Wacky start to 2016, eh?

Jumping right into it in this morning's Early Look, Hedgeye U.S. Macro analyst Christian Drake sums up yesterday's wild market movements from Japan to Europe to U.S.

He sums it up in one sentence:

"The 2016 equity casino is officially open."

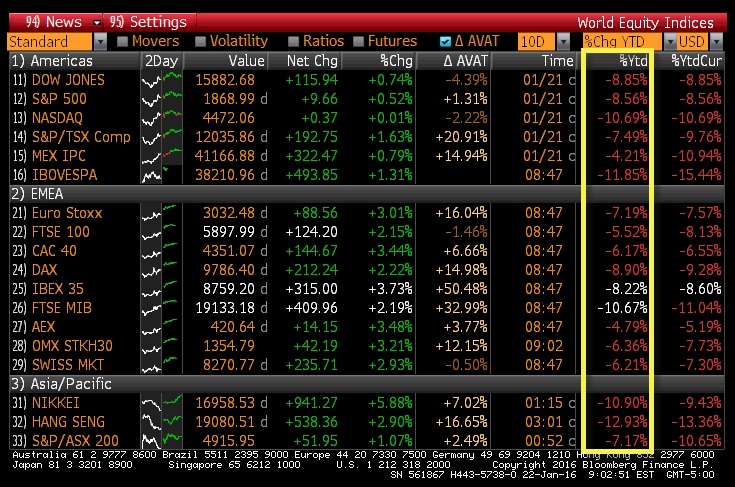

Agreed. So, before the perma-bulls get too excited about yesterday's bounce, take a look at year-to-date global equity performance...

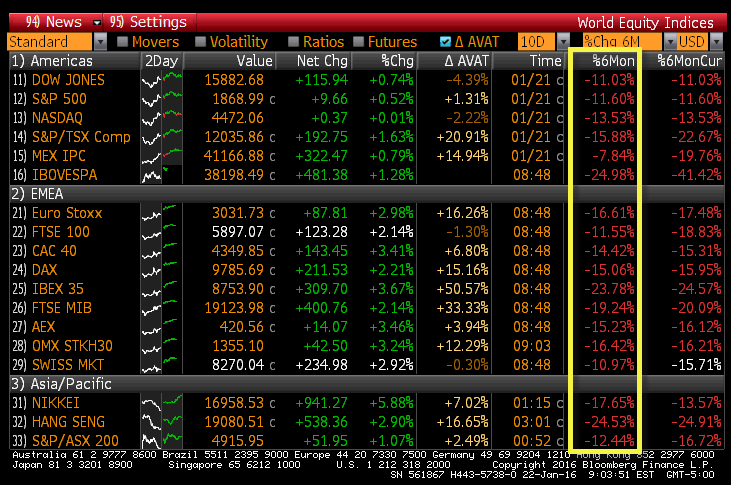

Even worse... how about the draw-down from those summer bubble highs?

The reality is that volatility is just starting to ramp. We reiterate: Sell on strength...

That in mind, here's a quick recap of yesterday's moves and an update on where we think we're going from a note sent to subscribers this morning.

"Yesterday the Nikkei rallied on a central bank rumor of more easing then sold off on a contradictory rumor, the SPX futures gapped higher on Draghi pointing to rising downside risks, oil rose on higher inventories and the U.S. equities finished higher alongside a 4th month of contraction in the Philly Fed Index and a rise in rolling jobless claims to their highest level since April of last year.

This morning’s catalyst is Chinese officials vowing to “look after” stock investors. Manic price action in markets and reactionary policy responses out of central banks are not outcroppings of improving fundamentals. GrowthSlowing remains the call and we remain sellers of strength."

... Meanwhile in Europe

"While European equities are bouncing today, nothing has changed with our fundamental outlook of #EuropeSlowing. We got our first touch of reality on the inflation outlook from the ECB in ECB governing council member Ewald Nowotny saying there are risks inflation could turn negative due to low oil prices in H1’16.

Also as no surprise, Eurozone GDP and CPI forecasts for the next three years were largely all guided down by a group of external analysts (we expect similar results from the ECB’s staff projections at the March meeting). Finally, preliminary January PMIs for the Eurozone all fell month-over-month. Manufacturing (52.3 vs 53.2 prior), Services (53.6 vs 54.2 prior), and Composite (53.5 vs 54.3 prior).

Got #GrowthSlowing?"

Keep you head up out there.