The EUR/USD is currently trading down -0.50% to $1.0838 following this morning’s interest rate decision from the ECB in which rates were left unchanged (as expected), and any action to increase the size of the Bank’s quantitative easing program or issue any other “unconventional” programs were kicked to its next meeting on March 10th. The March meeting will also include the Bank’s staff forecasts for growth and inflation, the results of which could be a catalyst for the Bank to act.

Call Outs: Draghi reiterated the old Song and Dance. Today’s presser showed once again Draghi’s mentality to Extend&Pretend economic gravity. He continually cited the prospect of sustained low energy prices and the economic slowdown in China as contributing factors to the Eurozone's low levels of inflation. As we show in the first chart below on inflation, we expect CPI to remain low in 2016 (sideways at best), and far from the Bank’s pipedream of 2.0%.

What does today’s market action mean? Investors remain holding a massive short position in the EUR/USD. [See second CFTC chart below]. Within a strong dollar and weak commodity market, alongside mute growth prospects for the Eurozone, we continue to think this short position has legs in 2016, as investors become increasing aware of the inability of QE to move the needle on inflation.

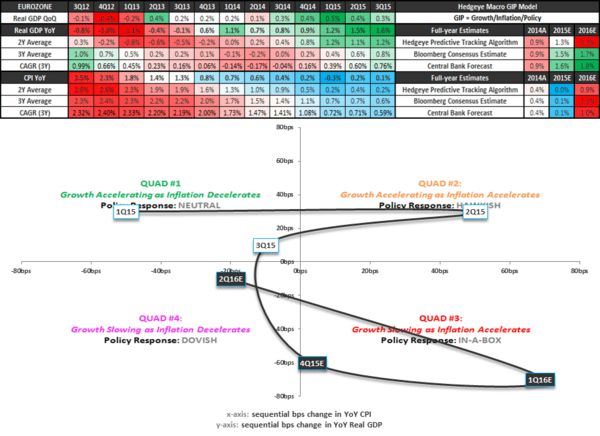

Our mantra remains the same. We maintain our macro theme of #EuropeSlowing, with our proprietary GIP (growth, inflation, policy) model signaling the Eurozone in #Quad3 (growth slowing as inflation accelerates) and #Quad4 (growth slowing as inflation decelerates) in Q1 and Q2 of this year [third chart below]. We expect the Bank’s staff revisions to its GDP and CPI projections to head lower in its March meeting.

What’s our policy outlook? We expect there will be increased pressure that the ECB has to act by expanding the size of its QE program (to €75-95B/month), which could come as soon as the March meeting. We expect the ECB to continue to place significant weight on oil prices, Chinese data, and its staff projections, all of which we expect to deteriorate into March.

EUR/USD Levels: The EUR/USD is in a bearish formation meaning it is broken across TRADE (3 weeks are less), TREND (3 weeks or more) and TAIL (3 years or less) durations.