Below are our analysts’ new updates on our fourteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this.

Please note that we added the Allscripts Healthcare Solutions (MDRX) and Foot Locker (FL) to the short side of Investing Ideas last week. We will send a full research report to subscribers on Foot Locker early next week. Please note that we also removed Zoës Kitchen (ZOES). Hedgeye CEO Keith McCullough’s updated levels for each ticker are below.

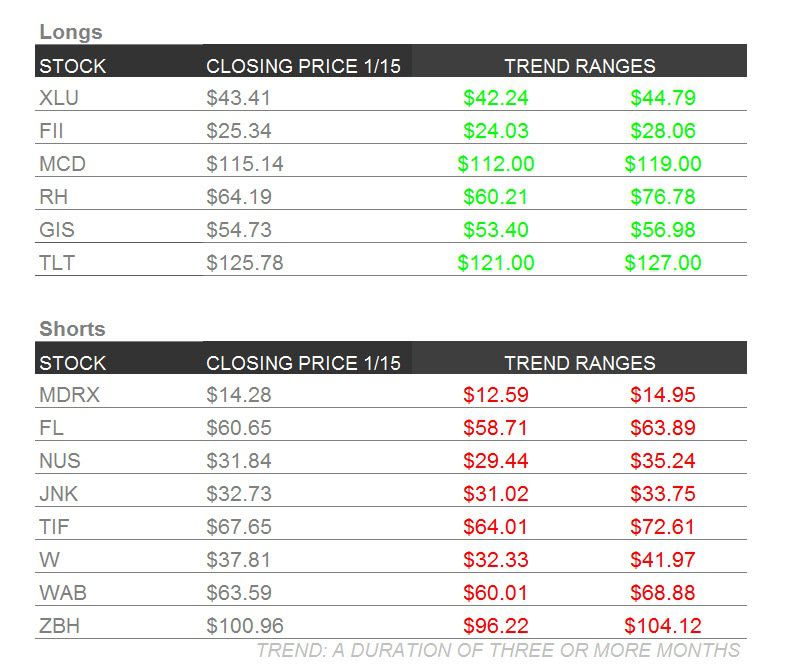

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

TLT | XLU | JNK

To view our analyst's original report on Junk Bonds click here and here for Utilities.

We added Utilities (XLU) on the long-side last Friday as the market continued to pummel everything we haven’t liked (high debt, high beta, and small-cap stocks leveraged to inflation expectations) – Utility stocks are low-beta, slow-growth bond proxies which is why they are by far the best relative performer YTD.

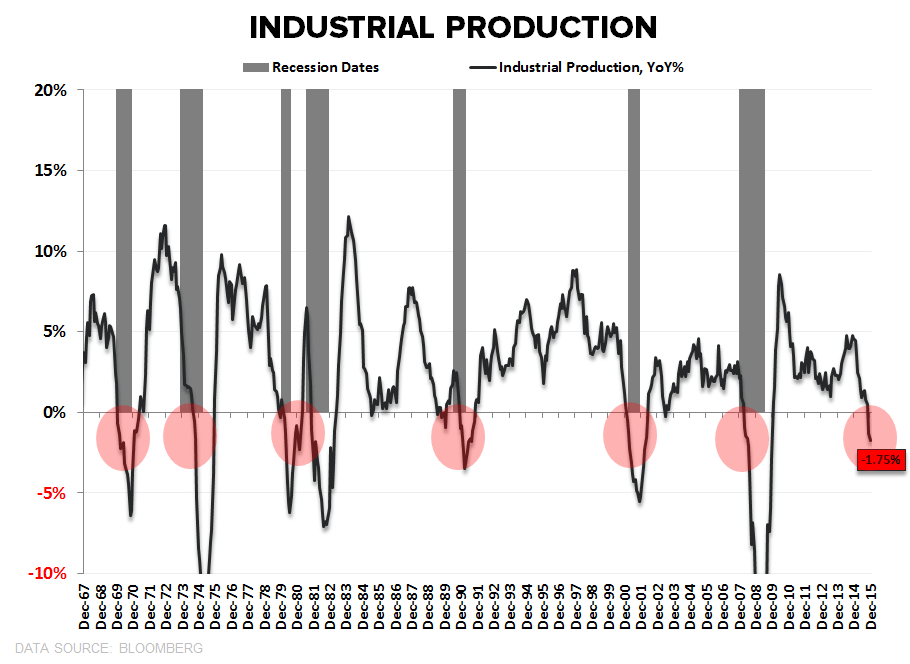

XLU is outperforming the S&P 500 by +7% and remains flat on the year. Friday’s large swath of data echoed what we have been saying for a while now on the deflationary risk of an industrial recession:

- Industrial Production for December printed down -1.8% Y/Y, accelerating to the downside (first negative Y/Y print of the current cycle)

To exemplify the depth of the current industrial recession, we quoted the CEO of Fastenal, Dan Florness in his introduction to the company’s earnings call on Friday. This quote comes from a guy who’s in the trenches:

“In the first quarter of this year, 72 of our top 100 customers grew. In the second quarter, that dropped to 63. In the third quarter, that dropped to 56. In the fourth quarter, that dropped to 49. So in the fourth quarter, half our top 100 customers grew and half contracted. In the month of December, to amplify that a little bit, 41 of our top 100 customers grew and 59 contracted.

We sell across the continent and around the planet; most of our business is in North America. And we sell to a lot of different industries. And when you start looking through the list, a lot of names that you would recognize stand out and you can see the pain they're feeling in their business.”

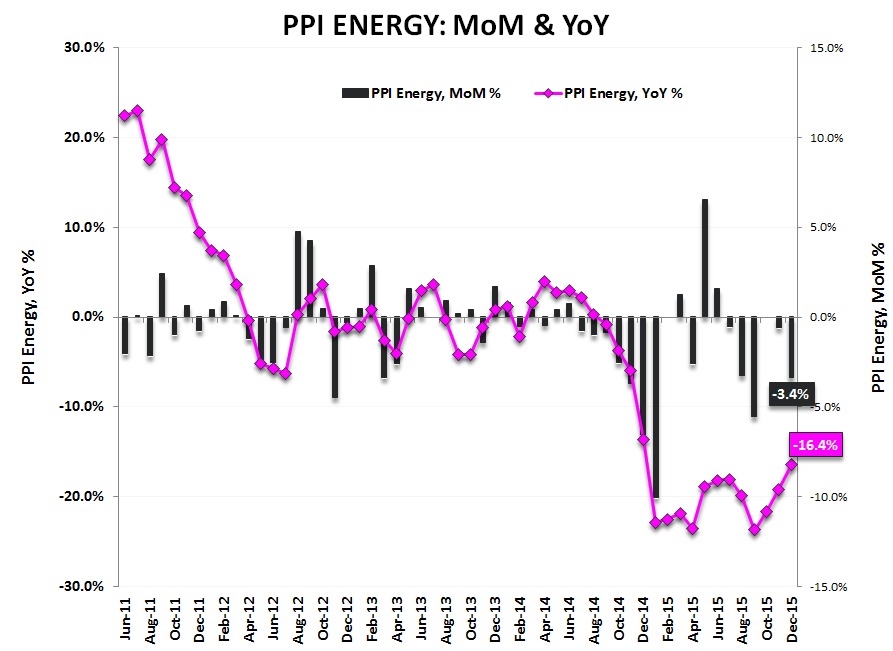

More on the depressed state of the producer. Deflationary PPI continued its march downhill with December reported numbers:

- Headline PPI declined -1.0% Y/Y

- PPI Final Demand declined -3.9% Y/Y

- PPI Final Demand Services increased +0.4% Y/Y

- PPI Energy declined -3.4% Y/Y

As mentioned in last week’s newsletter, with growth continuing to slow and volatility breaking out to the upside across asset classes, we expect the unwinding of a record amount of corporate credit leverage to continue. We’d put that deleveraging in the third or fourth inning currently. Credit spreads will continue to widen.

That's why you're long TLT and short JNK.

NUS

To view our analyst's original report on Nu Skin click here.

Nu Skin (NUS) continues to be a best idea SHORT for us in the consumer staples sector. They were down at the ICR conference in Florida, but did not provide a webcast to their presentation.

We found this to be odd and deceiving. Upon reaching out to IR, they said they didn’t feel the need to webcast because they were just showing slides from a previous presentation. We heard the room was pretty empty.

FII

To view our analyst's original report on Federated Investors click here.

What is the long-term thesis behind our Federated Investors (FII) long call?

Over the past 7 years, more than $1 trillion has been redeemed in money funds and reallocated to stock and bonds, sourcing the big bull market in risk assets. With the economic cycle eclipsing 72 months, we think it is time to get defensive.

In addition to improved profitability from even marginal rate hikes, this $1 trillion becomes a longer-term opportunity for all money fund markets as investors reallocate and back out of risk assets in the latter stages of this market/economic cycle.

With roughly 9% market share in industry money fund assets, FII will recapture these funds as they come back out of stock and bond markets. We have modeled +$200 billion in positive money flow for the money fund industry in 2016 and +$400 billion for 2017. This assumption reflects some conservatism allowing for some funds to remain outside the money fund channel.

WAB

To view our analyst's original note on Wabtec click here.

We believe freight rail equipment spending is just starting to enter a multi-year downturn. It’s a cyclical market, but Wabtec (WAB) shares remain priced for growth. WAB's peak margins also aren’t a great sign for longs. Here are two key charts:

TIF

To view our analyst's original report on Tiffany click here.

Tiffany (TIF) is scheduled to report holiday sales on Tuesday Jan 19th and at the same time should give preliminary guidance for FY 2016. We still think that earnings expectations for 2016 are 5-10% too high. The stock hit new 52-week lows mid-week then rallied slightly into the weekend.

We suspect the strength versus the down market may have been due to shorts covering into this sales announcement, booking some gains with the stock down 20% over the last month.

W

To view our analyst's original report on Wayfair click here.

Wayfair (W) presented at a retail conference this week, and as usual CEO Niraj Shah delivered a compelling message. However, we maintain our negative position on the company's business model as management is building the infrastructure for a total addressable market 5x larger than it really is.

Also, we firmly believe mono-channel does not work. Restricting sales to just the internet in this category is just as bad as a retailer who focuses 100% on physical stores.

Both are highly likely to fail over time.

RH

To view our analyst's original report on Restoration Hardware click here.

On Restoration Hardware (RH), we’re as confident as ever that NEAR-TERM earnings expectations are completely in check, and that long-term earnings are too low. And we’re as sure as we can be that we’re not about to be blindsided by any kind of press release from the company about management, business trends, or promotions.

We’re now looking at historically peak short interest (33% of float), and the multiple setting a new historical trough (16x). Put another way, we’re talking a 16x multiple for a 40% EPS grower.

Obviously, the market thinks we’re wrong in our earnings math. We’re absolutely not ignoring a material slowdown in the economy or Hedgeye’s bearish Macro view. We simply think that RH should still do better than the consensus in that environment, and that’s what we’re focused on given the massive 40% correction since November, and 20% month-to-date in January.

In the end, we think the risk is isolated to the multiple, not the consensus earnings, and that’s what matters most at a 16x p/e with 33% short interest.

MCD

To view our original note on McDonald's click here.

McDonald's (MCD) is down just -2.5% YTD. That is impressive considering what the market is doing around it. This stock continues to be Howard Penney’s top idea in the Restaurants sector. Looking out into 2016 we are looking forward to them having a full year of All-day Breakfast and their McPick 2 menu.

Long investors should be looking forward to that too.

ZBH

To view our analyst's original report on Zimmer Biomet click here. Here's an update from Hedgeye Healthcare analyst Tom Tobin.

"We listened to an upbeat CEO of Zimmer Biomet (ZBH) present at JPM this week. SYK also made some positive comments which resulted in a brief ortho rally this week. But it didn’t last.

I wasn’t surprised, or terribly concerned, about the short case unwinding here, and that turned out to be a good decision. ZBH’s CEO expressed a lot of optimism about the Biomet integration and the “cadence” of new products in 2016. I think what will be more impactful is the cadence of the US Economy which is already slowing into a rate cycle; not a good combo for employment and what is often a deferrable surgical case.

In terms of the narrative ZBH tells about the upside to their business longer term they used the chart below in their discussion. Up and to the right is good for the population of people over 65 years old, but pay attention to the scale.

The dates range from 2010 all the way out to 2050. If we take the next step and ask what the annual growth rate is in this chart, the answer is +1.9% per year. Since pricing is trending at -2.5%, adding 1.9% population growth yields 0% market growth.

With bundled payments emerging this year (CCJR) in knee surgery, and with more bundles coming next year from CMS, I don’t see that ZBH is in as enviable a position as they claim. Taken together, 1.9% volume, less -2% pricing, less bundled payment pressure, less US and global growth slowing, would mean they really have a difficult task in front of them to grow at all.

They’ll surely cut costs, and grow EPS, but that strategy does not typically yield an expanding multiple and good stock performance.

But we’ll see."

GIS

General Mills (GIS) led a $3 million funding round for kale chip maker Rhythm Superfoods. Although this is not a big deal and will most likely never make a strong impact to top or bottom line, it marks a changing in the tide for management thinking. They are making a distinct effort to delve deeper into the natural and organic category which will help them a lot in the long run.

Although the overall market has been atrocious year to date, down roughly -8%, GIS with its low beta, big cap, style factors has held in, down just -5%. We continue to like General Mills as a LONG, especially during the tumultuous times in the market.

MDRX

We added Allscripts Healthcare Solutions (MDRX) to Investing Ideas this past week. Click here to read our analyst's full stock report.