Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to learn more.

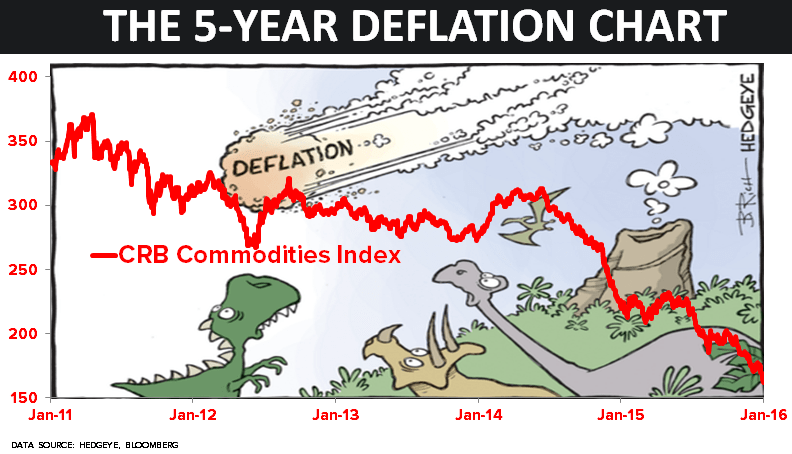

"... After this 1-day bounce off the Russell 2000’s crash (20% decline from July) intraday low yesterday, and commodities “bouncing” off 5-13 year lows (CRB Commodities Index down -20% in the last 3 months alone – see 5-year non-“transitory” deflation chart for details), I’m looking forward to swimming with both Potomac and the non-peddled-rate-of-change data. I won’t drown our clients that way."