RECENT OUTFLOWS

WisdomTree assets-under-management (AUM) finished last year in fluid fashion with -$3.0 billion flowing out of the asset manager in December alone. This was the worst month in the history of the firm and January 2016 hasn't started in any better fashion. In the first five business days of the New Year, WisdomTree has shed another $686 million, essentially on par with the -$3 billion monthly run rate exiting '15. We can't exactly chalk up year end loses to seasonality, as December 2014 put up a +$1.0 billion inflow for WETF. Monthly inflows are now a pittance of their highs of over $6.0 billion from March '15. Over 90% of the losses in both December and January occurred in the firm's international hedged equity products.

The Tale of Two Products

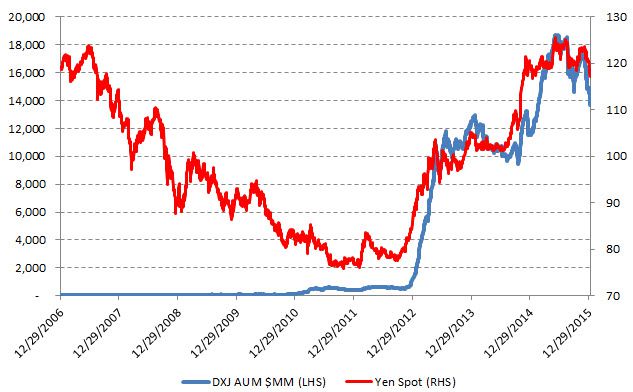

We are chalking the exodus in the international hedged products to separate catalysts as firstly the firm's Japanese hedged product has fallen victim to a substantial rally in the Yen which has taken demand for the hedged FX fund off of the boil. We warned of a slack in demand should the U.S. dollar not continue to strengthen which has proven accurate over the very near term.

The firm's European product can't be painted with the same brush however as the Euro has maintained its price range against the U.S. currency.

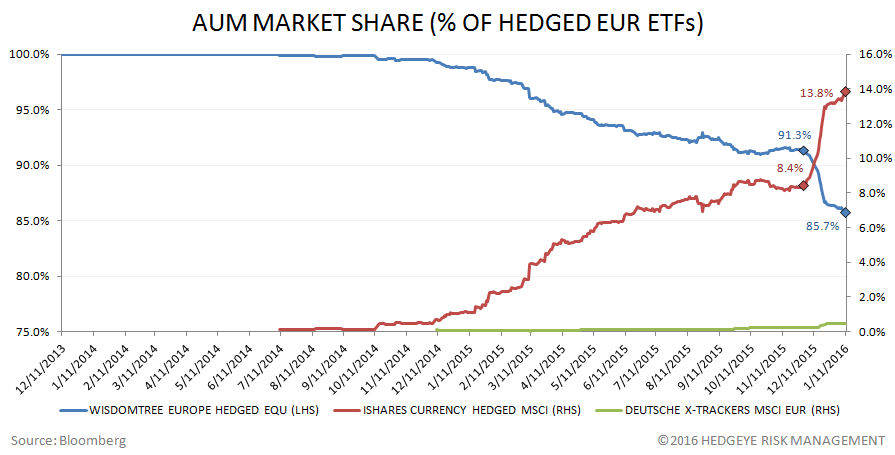

It looks however that European woes are the result of new demand for the copy cat iShares hedged product (which is 5 basis points cheaper). The following chart shows how the HEDJ moved from a 91% share of the market’s three major hedged Euro products (WisdomTree’s HEDJ, BlackRock’s HEZU, and Deutsche’s DBEZ) at the beginning of December to 86% share through yesterday. This has increased the HEZU iShares Currency Hedged MSCI Europe share from 8% to 14% over the same period on net positive inflows respectively.

Additionally, DXJ’s share of the market’s three major hedged Japan products (WisdomTree’s DXJ, BlackRock’s HEWJ, and Deutsche’s DBJP) ceded another point of market share over the past month. The Deutsche and BlackRock products both gained incrementally in December finishing at just over 9% and 4% share respectively.

PRICING NOW IN QUESTION and Forward outlook

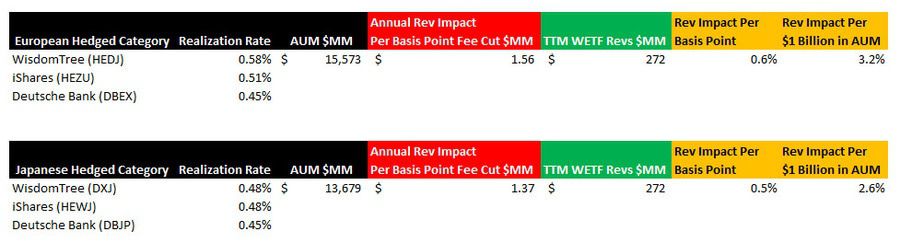

It looks like pricing is becoming a factor with the emergence of investor interest in the iShares hedged European product (or it was just a catch up trade to share that the Japanese product had already ceded to competitors). While the delta's of price decreases per basis point are quite small, we don't think Street estimates incorporate a lot, if any, pricing compression for WisdomTree. At a 1 basis point decline for HEDJ pricing on an annual basis, we calculate a -0.6% top line revenue impact, but with AUM in decline the impact could be worse. We calculate for every $1 billion in AUM lost for the hedged European fund that annual WisdomTree revenues decline by -3.2%. The impact on pricing and AUM are not as severe for the Japanese DXJ product.

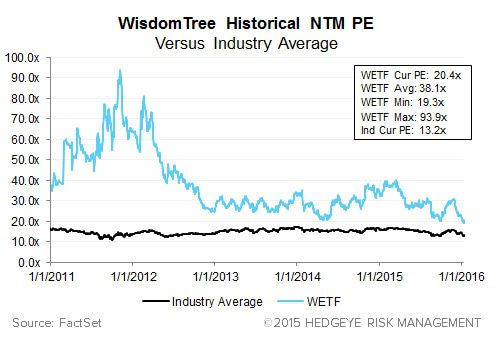

The ongoing fundamental issue from our vantage point is Street consensus is way too high (which is increasing by the month with the development of net outflows). We calculate that 2017 consensus estimates of $0.97 per share (the out year numbers this growth stock is valued on) to be based on over $80 billion in AUM. With assets-under-management at $47 billion currently, this is a stretch at best. Even our $0.79 estimate for '17 based on $70 billion in AUM looks ambitious at this point. WisdomTree continues to trade at a substantial premium to the asset management group at over 20.0x next 12 month estimates versus the group at just over 13.0x '16 numbers which make estimate cuts problematic. The stock remains on our Best Ideas list as a Short.

WisdomTree (WETF) - More Questions Than Answers - We Remain Short

WisdomTree (WETF) Black Book Presentation - Not So Smart Beta

Please let us know of questions,

Jonathan Casteleyn, CFA, CMT

Joshua Steiner, CFA