Below are our analysts’ new updates on our thirteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this.

Please note that we added the Utilities Select Sector ETF (XLU) to Investing Ideas on Friday. We will send a full research report to subscribers early next week. Hedgeye CEO Keith McCullough’s updated levels for each ticker are below.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

TLT | XLU | JNK

To view our analyst's original report on Junk Bonds click here. Since we added short Junk Bonds to Investing Ideas in October, JNK is down -7.8%, versus -4.5% for the S&P 500. Our long TLT position is up 7.7% since adding the position in August 2014, versus -0.2% for the S&P 500.

After the worst start to a year literally EVER for U.S. equity markets, TLT caught a bid in the first week of trading as the centrally-planned Chinese stock markets traded limit down earlier in the week. It was the largest central bank liquidity injection from Beijing since Chinese markets crashed in September.

TLT remains one of our strongest long idea calls heading into 2016 as junk bond markets begin to crack.

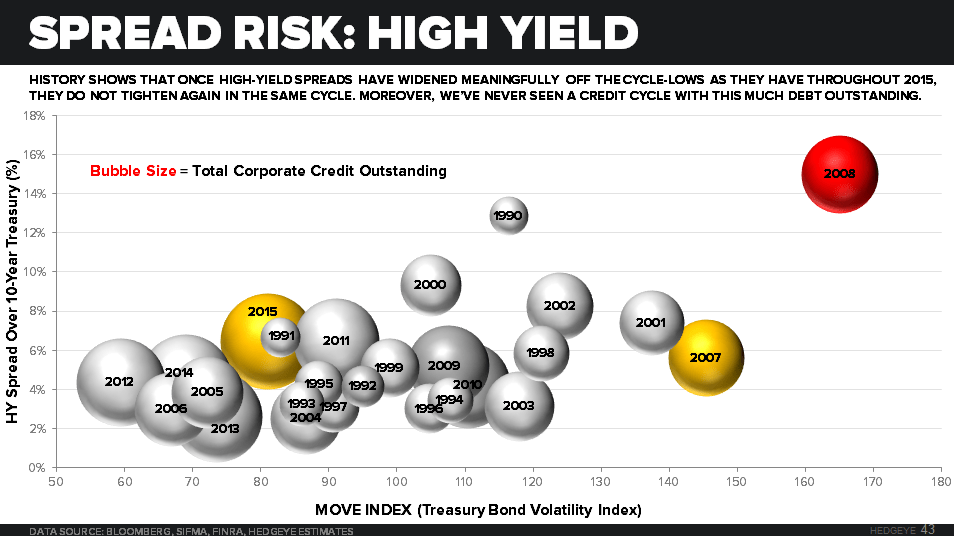

With the introduction of our Q1 2016 themes presentation this week we outlined the epic corporate credit risk in our #CreditCycle theme. The chart below presents a good picture on how epic this risk really is:

- The size of the bubble corresponds with the total amount of corporate credit outstanding;

- SIFMA reports that total corporate credit outstanding has increased 2.5x in 15 years;

The excessive amount of corporate credit outstanding today is concerning, as credit spreads have started to move off of their 2014 lows in yields and volatility. Once spreads break out above their long-term averages a recession typically follows. The table below shows both investment grade and high yield credit spreads:

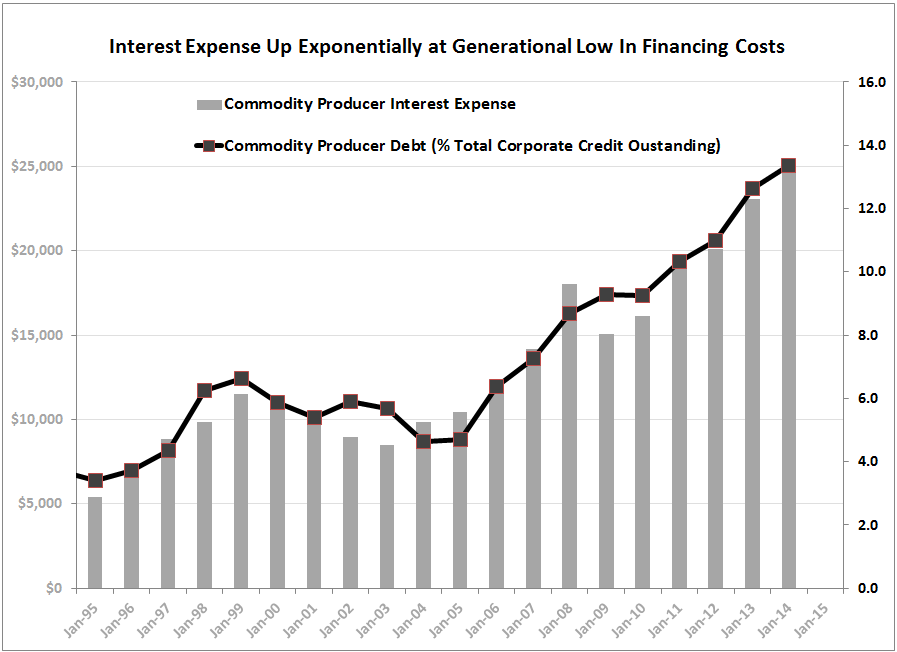

The third chart below may be most alarming of the bunch, as it relates to the excess financing that has taken place over the last 10 years, much of it in the commodity sector. Below we are showing interest expense over time for a sample of large commodity producers. The most important thing to consider when viewing this chart is that every interest rate cycle since the early 1980s has led to lower lows in interest rates. With cheaper financing, interest expense should be declining and not increasing rapidly. The leverage has been piled on, so stay out of the way as it unravels. Stay short of JNK and long of safety (TLT).

NUS

To view our analyst's original report on Nu Skin click here.

Nu Skin (NUS) is under investigation in Taiwan for illegal importation and sale of ageLOC Spa machines into the country. It is currently unclear which way the investigation will swing, but NUS has stated that potential penalties could include fines up to $3,000 USD and if applicable jail time for employees involved.

That's a small sum but this is just the latest in potential wrongdoing by Nu Skin globally. NUS remains on our best idea SHORT list, both on the fundamental business deterioration as well as the results stemming from certain government investigations.

FII

To view our analyst's original report on Federated Investors click here.

The slight $26 billion inflow into money funds for calendar 2015 masks the trend that money was moving to the sidelines for the bulk of last year. Outside of a 1Q15 drawdown of over $140 billion for cash products that sourced seasonal demand for stocks and bonds, investment capital then furiously moved to the sidelines from 2Q15 onwards.

This move to cash is just beginning in our view, as the past 7 years have seen over $1 trillion redeemed in cash products which has chased returns in the stock and bond markets.

The annual inflow into money funds for 2015 looks a lot like the growing conservatism that marked 2005 and 2006 which lead into the Financial Crisis of ‘07/’08 (and banner years for the money fund industry with inflows of $654 and $637 billion respectively). As risk assets start to deflate, money will accelerate its move to the sidelines and leading cash managers including Federated Investors (FII), Legg Mason (LM), and BlackRock (BLK) will benefit. FII has the most leveraged to this trend which is the rationale for its long Investing Ideas placement.

WAB

To view our analyst's original note on Wabtec click here. Since Wabtec was added to the short side of Investing Ideas, the stock is down -33.1% versus -1.6% for the S&P 500.

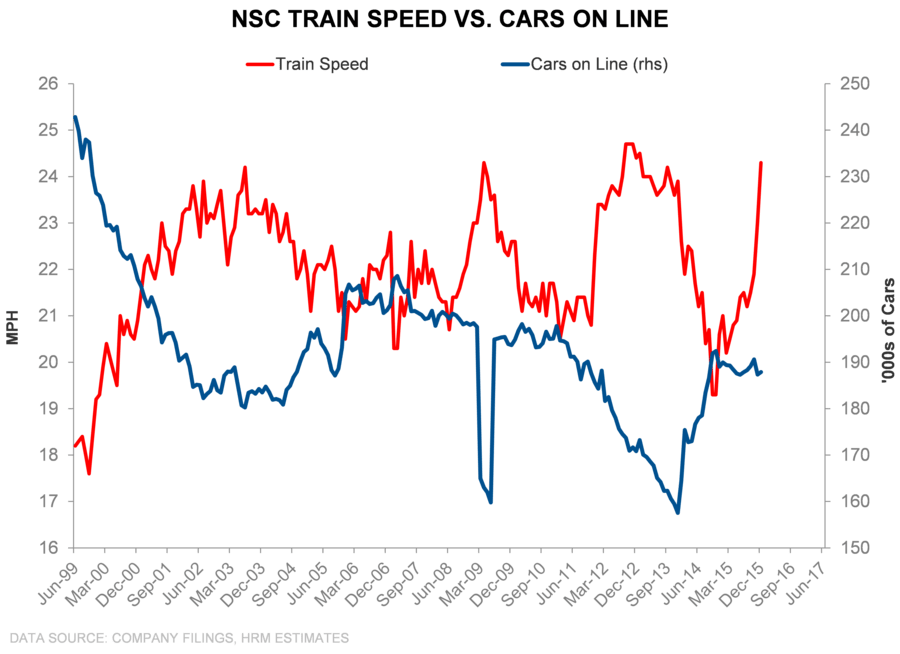

The data from Norfolk Southern (NSC) below illustrates the key relationship to consider for our short Wabtec (WAB) thesis. Slower speeds tend to pull equipment on to the track. Now that speeds are picking back up, we expect that equipment to be pushed back out. One can think of it as turning existing assets more quickly.

More speed results in less equipment in service. If speeds continue higher, freight railroads may find themselves with ample excess equipment and reduced aftermarket needs amid slow volume growth – a negative combination for WAB.

TIF

To view our analyst's original report on Tiffany click here. Since Tiffany was added to the short side of Investing Ideas, the stock is down -12.4% versus -1.5% for the S&P 500.

Macy's gave its holiday sales update this week, reporting comp sales down -4.9%. Of the major department stores Macy's has the most similarities to Tiffany (TIF). They have a relatively similar customer, they both have exposure to international tourist traffic, and they both have a notable NYC presence.

We think the Macy's report is a negative for TIF's underlying sales trends. However we don’t think we will see as large of a slowdown from TIF, since warm weather likely impacted Macy's and the company attributed about 80% of the comp decline to the unseasonably mild November and December. We continue to think that 2016 expectations are too high and the market seems to agree. TIF hit new 52-week lows on Friday.

W

To view our analyst's original report on Wayfair click here.

This week Wayfair (W) announced the launch of Wayfair.ca, along with business and trade programs in Canada as well. This announcement does not have a material impact on the company for two main reasons.

- The company already serves the Canadian market and about 2% of web visitors come from Canada so the most interest parties are likely already customers;

- The market opportunity is much smaller as Furniture and Home Furnishings retail in Canada is about 14% of that of the US.

Wayfair will continue to invest in an infrastructure that is built for a market much larger than it's true addressable market. Either the sales will not be there in the future or gaining those sales will be too costly for W to make an real profits.

RH

To view our analyst's original report on Restoration Hardware click here.

More than any other company/issue we've had questions on since 2016 kicked into high gear, Restoration Hardware (RH) takes the cake – and more specifically, its near-term earnings trajectory. We’re not surprised, and we agree 100% with the impetus for the concern.

The cold hard fact remains that the tactical game changed in December due to promotional activity, perceived economic sensitivity, and timing issues around concept and new store launches. However, we believe fully in the long-term call, and believe now as much as ever that there’s $11 in earnings power, and that people will actually start to believe it within a year.

MCD

To view our original note on McDonald's click here. Since adding McDonald's to the long side of Investing Ideas, in August, the stock is up +16.2% versus -8.7% for the S&P 500.

McDonald's (MCD) boasts style factors that are best in class for turbulent times in the market, big cap and low beta and it has handily been outperforming the market and its competitors as of late. One of the biggest aspects of competing in their space is value offering.

Wendy’s, Burger King, and McDonald’s, are the three big players duking it out. Each company offers a different value proposition, Wendy’s 4 for $4, Burger King’s newly introduced 5 for $4, $1.49 10 piece chicken nuggets, 2 for $4 croissan’wich, and McDonald’s recently launched a 2 for $2 menu called ‘McPick’, that will offer four items ― the McDouble, the McChicken, Small Fries and Mozzarella Sticks.

Everyone has their favorite fast food joint to get a burger, but the company that provides the best value will entice the most crucial customer in the space, the value customer, or the person looking for a cheap good meal that will satisfy their stomach and their wallet.

Consumers have a choice when they eat, they can go out, or they can eat at home, and when a concept can bring the price point near or even below what it would cost to cook in, that’s when you win.

McDonald’s has ceded share in the value category primarily to Burger King over the last two years. Now that they are launching a national value platform with a full slate of media support, MCD will recover the value customer.

ZBH

To view our analyst's original report on Zimmer Biomet click here.

The JPM Healthcare Conference commences next week and Zimmer Biomet's (ZBH) and many hundreds of companies including their customers and peers will be sharing their initial views of 4Q15 just past. They will typically comment on their long term opportunity and the “aspirational” EPS growth target of 8% to 12%, which they have made at the last two JPM presentations. We’ll follow up next week with some comments on their presentation and the JOLTS update for November reported next Tuesday.

We were fortunate to attend a dinner in Boston last night with executives from Partners Health. Partners is clearly preparing for population health and more bundled payment arrangements like the one going into place for knee replacement this year (CCJR) over the coming years. Their $1.2 billion IT system investments in Epic software is one major way they are adapting to a more challenging healthcare market. And while they don’t expect to see a big change to knee device prices in 2016, big changes are afoot that seem very likely to permanently alter the market.

GIS

General Mills' (GIS) business seems to be starting to pick up steam, as the company is working to improve merchandising and advertising on core business.

In addition they have executed a few small, but meaningful M&A deals showcasing the change in managements thinking. The divestiture of Green Giant to B&G Foods, for instance, although a profitable business, was a good move for them given their lack of focus/investment in the brand (they have more opportunities like this throughout their portfolio, in addition to SKU rationalization).

Most recently, they acquired a yogurt maker in Brazil named Carolina and a meat snack producer in the US called EPIC Provisions. Carolina represents their entry into the yogurt category within Brazil which is a $3 billion market which is growing double digits.

Secondly, the acquisition of EPIC Provisions (WEBSITE HERE), a roughly $25 million in net sales company, proves that management is changing the way they think. With the backing of John Foraker (President at Annie’s, now a GIS company) leading the charge both externally and internally to get this deal done. This was the smallest acquisition that GIS has performed in recent memory.

GIS continues to look for more sizeable acquisitions in emerging markets, but the string of pearls approach may remain most effective domestically.

ZOES

Zoës Kitchen (ZOES) stock price continues to struggle due to style factors being far out of favor. If you have a long-term position in the name, continue to hold strong because the fundamental business continues to perform very well.