HAPPY NEW YEAR INVESTING IDEAS SUBSCRIBERS!

It's been a particularly strong year for our research team, with prescient calls on both the long and short side. As such, Investing Ideas subscribers have had a commensurately good year. Congratulations and thank you for sticking with our process. We're happy to ring in the new year with you and look forward to another big year in 2016.

Below are our analysts’ updates on our twelve current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this. We will send CEO Keith McCullough’s updated levels for each ticker in a separate email.

IDEAS UPDATES

TLT | JNK

To view our analyst's original report on Junk Bonds click here.

The yield spread (10Y’s -2Y’s) compressed to a 52-week low of 120 bps this week. AGAIN, that’s a 52-week low in growth expectations right after “lift-off”. Into year-end, the bond market continues to price in what it has all year long: #Slower-and-lower-for-longer.

We continue to believe deflation will pressure the policy-fueled leverage embedded in junk and high yield bond markets. The cheap money, corporate credit boom inflated asset prices and it has more room to deflate. This deflationary run started in the second half of 2014, with the introduction of our #Deflation theme. Back then, was also the low in cross-asset volatility and the high in outstanding corporate credit (commodity producers chasing inflation expectations were the largest contributor).

As the current cycle gets longer in the tooth, the question bulls have to ask themselves is can the market see a sustained period of asset price reflation without entering a technical recession? We think not and are taking the other side of this trade.

The cycle always cycles. With last Tuesday’s final revision of Q3 GDP, the visual below is yet another cycle peaking chart. Stick with what’s worked into 2016. Bottoms are processes. And we're nowhere near a bottom in this credit cycle.

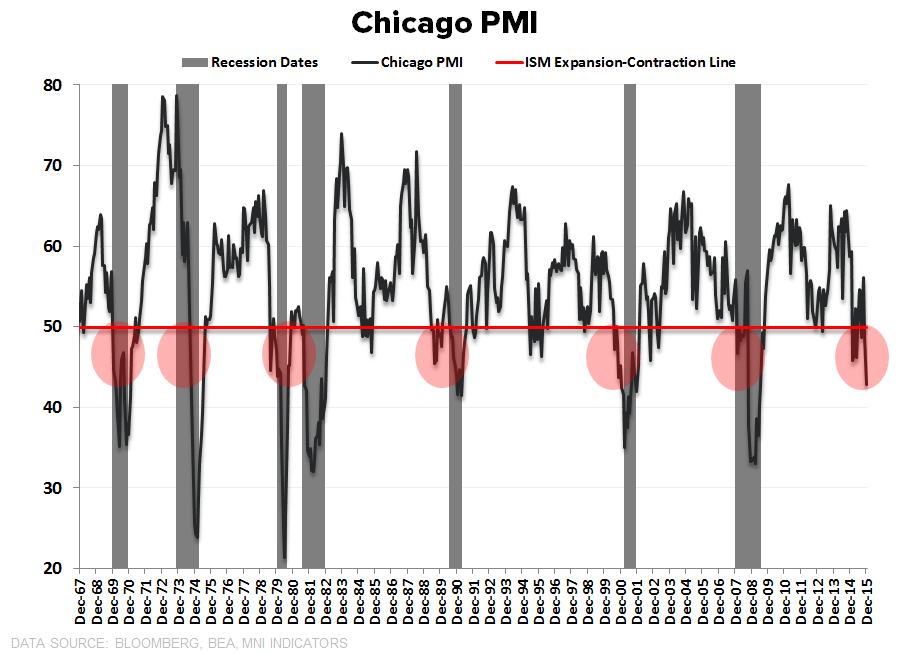

On a related note, Thursday's Chicago PMI number absolutely bombed. Here's a brief note Hedgeye CEO Keith McCullough sent to institutional subscribers last week:

"If only they’d stop reporting the cycle data! Today’s PMI reading of 42.9 for DEC (vs. 48.7 NOV) was a certified train wreck. I’m sure they’ll say it’s different this time (or something like that) but for those of you data dependent fans, I’ve attached the historical data series on this index reading. Some false positive readings vis-à-vis recession signaling but pretty strong track record."

TIF

To view our analyst's original report on Tiffany click here.

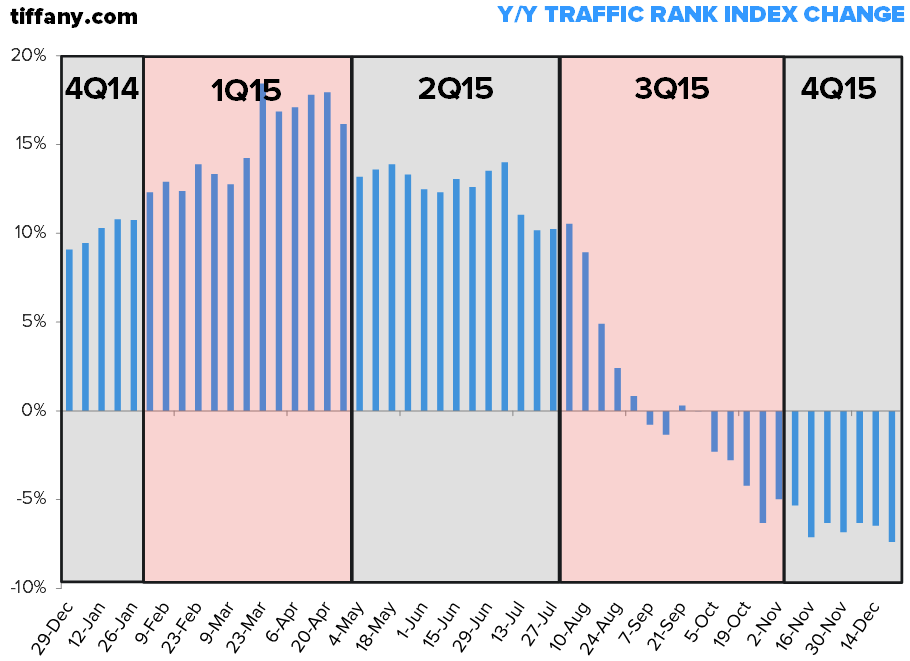

The weak traffic trends we saw in 3Q have persisted in 4Q for tiffany.com. Now, E-commerce only accounts for 6% of sales at TIF, but it’s a good barometer for brand relevance, since the average ticket for TIF sits at $750 there is a lot less impulse and more planning before a consumer slaps down a credit card and walks away with a blue box. Remember: 2016 EPS estimates have fallen to $4.32 from $5.63 at this time last year, and we think there is still downside to go.

W

To view our analyst's original report on Wayfair click here.

Wayfair (W) has considerably higher penetration in its total adressable market than people believe. People – including Management, are using numbers like $90bn as an addressable market. That’s just flat-out wrong. We’ve done extensive research on this one, and when all is said and done, we think that the end market is no more than $30bn.

To put that into context, it suggests that Wayfair has about 10% share of its market. That’s 2-3x the share of players like RH and IKEA. The primary reason is that Wayfair sells furniture and home goods. The purchasing process for a consumer durable like a set of bunk beds, for example, almost always includes in-store visits as well as online research.

You get that at Williams-Sonoma, Restoration Hardware, and even Pier 1. But you can’t touch and feel the seven million items sold by Wayfair before you buy. In fact, our research suggests that W’s target consumer has a ‘blind buy’ threshold of around $750. That’s well below the prices listed for furniture sold on its websites.

RH

To view our analyst's original report on Restoration Hardware click here.

Restoration Hardware (RH) is our top long idea in all of retail, and we view the recent weakness in the stock as a buying opportunity. All in we think the company will build to $5bn in sales at mid-teens operating margin which equates to $11 in earnings power. This growth and profitability comes from...

- ~30% Square footage growth with new full line design galleries.

- New businesses, like Modern and Teen, that can be easily layered over its low cost infrastructure.

- Leveraging occupancy from the "sweet heart" real estate deals the company is getting as a high end traffic driving tenant willing to take anchor size leases.

WAB

To view our analyst's original note on Wabtec click here.

Wabtec (W) has been a good short call for Industrials analyst Jay Van Sciver all this year. But since we added it to Investing Ideas September 11th, WAB shares are down -25%, versus the S&P 500 which is up 5% since then. Van Sciver thinks there is more downside ahead.

The crux of Van Sciver's original short thesis is still intact:

- "We believe Wabtec was a beneficiary of both resources-related capital spending (international freight railroads) and the congestion of the U.S. rail system in 2014."

- "With rail speeds increasing and mining capex falling through the floor, those supports should gradually be removed from this richly-valued stock."

- "The end markets do not look promising for Wabtec. Freight car orders are coming off their all-time highs as backlog does the same per Railway Supply Institute data. Class 1 Railroads are curbing capex spending in the face of slowing freight volumes. U.S. railroads are now putting equipment into storage."

- "Investors should increasingly note a disconnect between weaker order rates versus expectations for continued robust earnings growth in 2016. That would be a big problem for a 'growth' name with a high valuation."

FII

To view our analyst's original report on Federated Investors click here.

It should be a Happy New Year for Federated Investors (FII). With the Fed's 25 basis point hike in interest rates, in the financial sector, FII stands to benefit most from even this marginal change.

In essence, Federated Investors (FII) has a stable business for what we think will be a volatile 2016. 2015 finished with slight positive inflows into the firm's main business line, money market or cash products. This is reminiscent of the start of cash builds in 1999 and 2006 ahead of the negative returns in risk assets in 2000 and 2007.

The first rate hike in 9 years improves the profitability of the money fund business by 65% and leading money fund managers have a $1 trillion opportunity to claw funds back from stock and bond markets. In a beta centric sector we like the conservative business lines at FII which make it a relative outperformer for the upcoming year.

ZBH

To view our analyst's original report on Zimmer Biomet click here.

As a negative headwind, the #ACATaper had been slow to accelerate to the downside. As we close out 2015, the rate of change has most certainly gone negative over the last 6 months, but the next leg down appears to be holding out for 2016.

To begin the new year most healthcare companies and institutional investors will be gathering in San Francisco at the JPM Healthcare Conference. Managements, including Zimmer Biomet's (ZBH), will be sharing their initial views of 4Q15 just past and signaling with "body language" across the one on one table about 2016.

While we are interested in what transpires, we are even more interested in the December employment report on the first Friday of January and the subsequent JOLTS report for November the following week. Tops are processes not points and while we are past peak on the ACA tailwind for ZBH, the full brunt of the headwind remains ahead of us.

Editor's Note: To read Healthcare analyst Tom Tobin's more granular explanation of his #ACATaper theme and what it means for Healthcare stocks like ZBH, read his insightful Investopedia piece "Why a Perfect Storm Is Brewing In Healthcare."

MCD

To view our original note on McDonald's click here.

Since we added McDonald's (MCD) to Investing Ideas on August 11th, when Restuarants analyst Howard Penney argued that 2015 would be "the last time the stock is below $100", the fast-food giant is up 19%, versus a -3% loss for the S&P 500.

Part of the thesis was that MCD's All Day Breakfast would "lead to increased sales and customer satisfaction." Now, we have some data to formally back that claim up from a note Penney sent to institutional subscribers last week.

"Our most recent survey regarding All Day Breakfast at McDonald’s asked consumers, have you started to go to McDonald’s more often because they now offer breakfast all day? Out of the 2,000 people we polled 15.6% said they are going more often. This number seems small, but if you think about it as incremental traffic, this is a significant number. All Day Breakfast truly seems to be a traffic driver for MCD, and it’s driving the check too, as people often combo breakfast items with lunch and dinner items."

We continue to love McDonald’s heading into the new year and maintain our price target of $150.

NUS

To view our analyst's original report on Nu Skin click here.

Consumer Staples analyst Howard Penney has no incremental update on Nu Skin (NUS). We reiterate our short call on NUS arguing that it operates a "broken business model," VitaMeal is the smoking gun "hiding in plain sight," and the existing SEC Investigation and the lack of disclosures represents a material threat to the company's shares.

GIS

Why should investors own General Mills (GIS)? For one, the past year was volatile but GIS held up nicely. In fact, year-to-date, GIS is up 6% while the S&P 500 put up a loss of -2%. In essence, GIS has all the style factors we love from a Macro perspective; large cap, low beta and liquidity.

Here's a video of Hedgeye Senior Macro analyst Darius Dale on Fox Business laying out our economic outlook and hence why we prefer large-cap stocks:

(If you're having trouble loading the video, click here to watch.)

Since we added the company to Investing Ideas in May, shares are up 2%, versus tough tape for the broader market; the S&P 500 was down -4% over that period.

That said, GIS's fundamental business struggled in its fiscal 1Q 2016 two weeks ago. GIS is anchored in the slowing center aisles, and it has struggled in large part to meet analyst expectations. We believe this is due, in part, to management’s overly bullish outlook on their own business during the 1Q16 earnings conference call, which they toned down a bit during the 2Q16 call.

However, we're sticking with GIS heading into 2016 as the second half of its 2016 fiscal year is chock full of innovation, merchandising and strong advertising that should help lead General Mills get back to the leadership position in their categories.

ZOES

Shares of Zoës Kitchen (ZOES) have struggled of late in direct opposition to the trends supporting General Mills' outperformance. Due to the macro-driven market, high beta, low-cap names such as ZOES have fallen out of favor.

For "buy and hold" type investors, recent weakness is an opportunity to pick up ZOES on the cheap. We still love the management team and the concept of the restaurant. This company has a long runway of growth which we believe is only just in the beginning stages.

Furthermore, in a note sent to institutional clients earlier this month, Restaurants analyst Howard Penney asked this simple question: "Who Will Benefit Most From Chipotle's Struggles?" Interestingly, Penney makes a compelling argument in favor of ZOES:

"We want to single out ZOES as a company that will likely benefit from the demise of CMG. Their concepts although dissimilar in type of cuisine, are similar in that they both offer a premium, better for you option at a fair price with fast service. ZOES’ restaurants are conveniently and strategically located to take advantage of the opportunity, 80.1% of their restaurants are within five miles of a Chipotle. This only represents roughly 15.3% of Chipotle’s restaurants but that is a meaningful amount that will be under significant threat from such a capable competitor."