“We gain the strength of the temptation we resist.”

-Ralph Waldo Emerson

In Greek mythology, the Sirens were deadly yet beautiful creatures, who lured nearby sailors with their beautiful music to sail towards their island. According to mythology, the result of sailing towards the enchanting music and voices was inevitably ship wreck, since the island was surrounded by hidden rocks which were perilous to sail through.

Odysseus, the Greek King of Ithaca and the hero of Homer’s poem the Odyssey, was determined to experience the songs of the Sirens without crashing into the nearby rocks. On the advice of Circe, he had all of his sailors plug their ears with beeswax and tie him to the mast. Thus his sailors could sail the ship, without temptation, and since he was tied to the mast he was unable to steer the ship ever closer to the dangerous sirens.

No surprise, as the ship sailed closer to the Sirens, Odysseus reversed his orders and tried to get his men to untie him from the mast. Instead, as originally instructed, they tied him tighter, so his temptations would not overcome him and lead to a bad decision. Finally, when the ship had passed out of earshot, Odysseus signaled with his frowns that he be untied and released.

Like most Greek myths, there is a moral to this story. Simply put, it’s that our greatest temptations have the potential to be our greatest downfalls. As stock market operators, we are tempted daily by the magical songs of the Wall Street brokers.

If we are to follow the lead of Odysseus, it would be that we make sure our analysts have “bees wax” in their ears so that they remain are focused on the task in front of them and not be distracted. Meanwhile, as portfolio managers our hands should be bound so we don’t make arbitrary buy and sell decision based on nicely packaged narratives from the Sirens of the Old Wall.

If only it were all that easy!

Back to the Global Macro Grind…

One familiar common siren that sounds right about this time of year is the list of prognostications for the upcoming year. We don’t do these lists for two obvious reasons. First, markets and economies are never linear, so taking what we know today and predicting out over a year rarely makes sense. Second, the end or start of the year is simply an arbitrary time frame.

That said, we did do an update of our key themes and ideas headed into next year. There is nothing significant about the timing of these ideas as it relates to year-end, but on some level there is increased downtime headed into the end of the year, which gives us all a chance to review our investment perspectives.

Firstly, from our Macro team, the primary view, as it was for much for 2015, remains that growth will be slower than consensus is projecting for the U.S. There are a number of economic indicators which signal to us that the economy has, at best, peaked. The most notably of these are employment, consumer confidence, and corporate earnings.

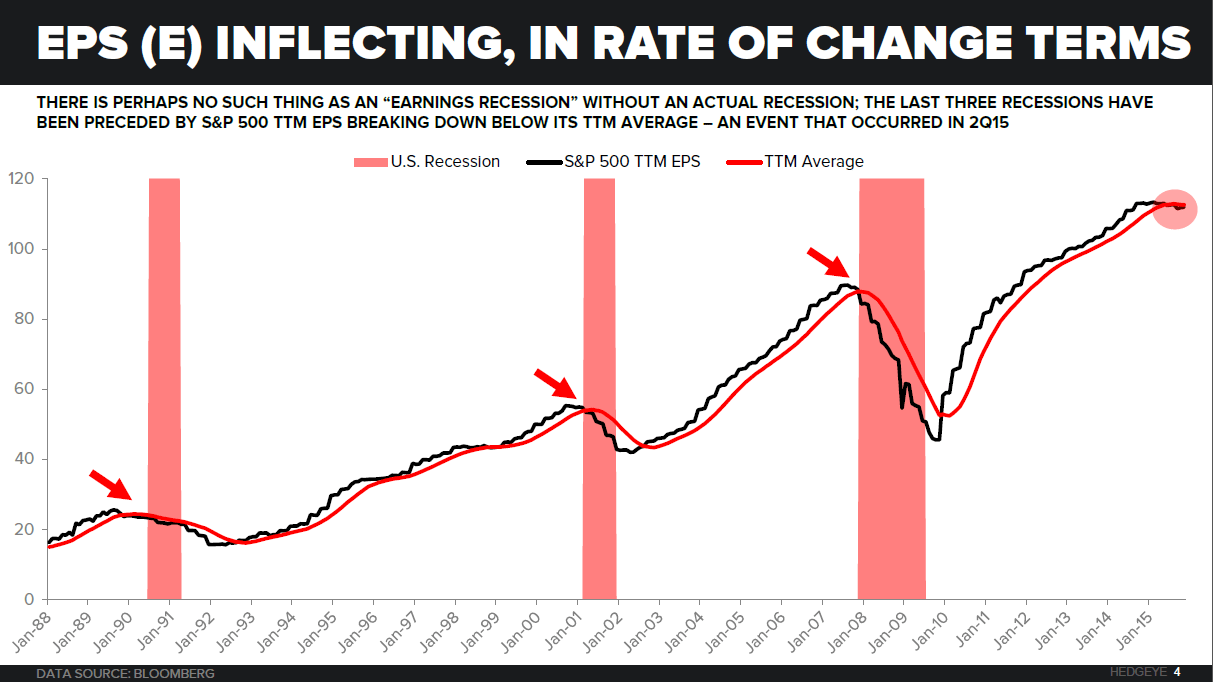

We’ve highlighted the last point on corporate earnings in the Chart of the Day. As the chart shows, all recent recessions in the U.S. have been preceded by a flat lining, or declining, of corporate earnings. This has already occurred in the U.S. with earnings breaking down below its trailing twelve month average in Q2 2015.

Secondly, our healthcare team is focused on the dramatic outperformance of healthcare company sales growth versus the broader SP500. Currently, healthcare sector sales growth is outperforming the rest of the field by almost 2.6x standard deviations. The obvious question is whether this is sustainable. According to our healthcare team this is unlikely.

Sales growth was pushed higher primarily because of the Affordable Care Act which produced more than 20 million healthcare users in a compressed period of time. This increase in healthcare users has been corroborated by an increase in job opening and hiring in the sector. Consistent with our #ACATaper theme, though, we think healthcare growth rates will be very challenged heading into the coming quarters, with one catalyst for this being lower than expected enrollees into the exchanges. (Click here to read Healthcare analyst Tom Tobin's summation of the #ACATaper on Investopedia.)

Finally, our financials team has been and continues to be very focused on the debt collectors. These companies historically have been the worst performing late cycle stocks in the financial sector, so they are poised to underperform cyclically. As well, the accounting for many of these companies is “challenging” at best, especially with the use of goodwill which tends to overstate the IRR of collection streams and the underlying flow through of net income.

The other key theme that the financials team is focused on currently is shorting the Canadian banks. From a macro perspective, the drivers of this short call were related to two Canadian bubbles: energy and housing. As it relates to energy, the bubble has basically all but burst with oil trading in the $30s and no surprise the Canadian banks, just like the Canadian economy, is over-indexed to energy.

On housing, simply put, the Canadian housing market on almost any metric remains wildly overvalued. While much of this over-pricing is centered in key markets, such as Vancouver, Toronto, and Alberta, in aggregate these markets also comprise the vast majority of the mortgage exposure of the banks. Perhaps the most telling for the Canadian housing market is the long term view versus the United States. Since 1970, the home price index in the U.S. has gone from 100 to about 900. While in Canada, home price appreciation is more than double the U.S. over that period.

Not sure we supplied you with any great buy ideas today, but hopefully we sounded the siren on a few to avoid. For our full update of ideas and themes, please take a look at the video below:

https://www.youtube.com/watch?v=4i-e-JktOpM&feature=youtu.be

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.15-2.30%

SPX 2005-2085

RUT 1107--1163

VIX 14.35-22.74

USD 97.42-99.35

Oil (WTI) 34.83-38.29

Copper 2.02-2.14

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research