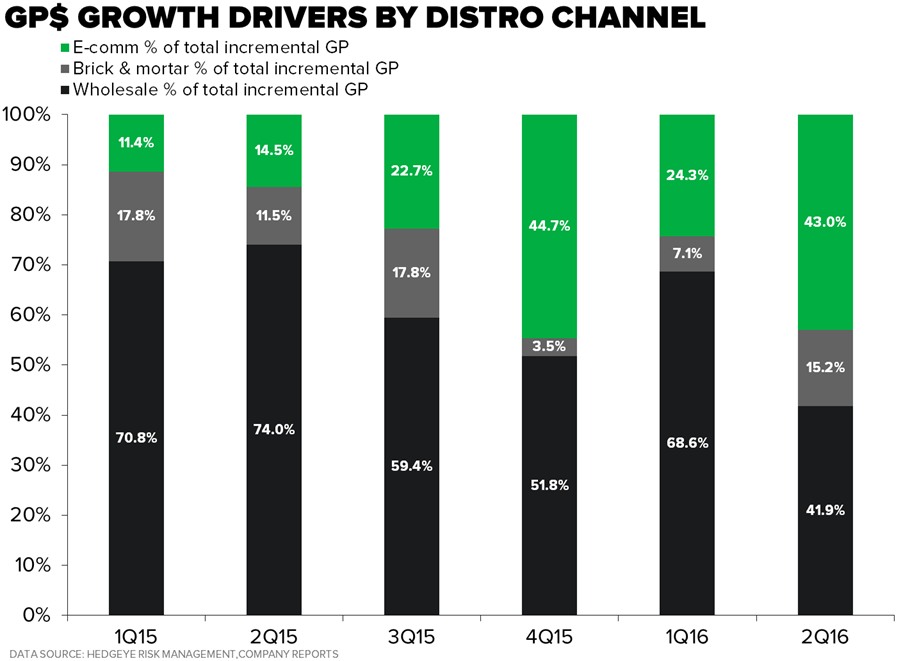

We find it amusing that in the entire 60 minutes of prepped remarks and Q&A, not once did Nike management comment (nor did anyone ask) about the most significant financial milestone we’ve seen out of Nike in the Mark Parker era. Specifically, this marked the first quarter in history where Nike DTC accounted for a greater percentage of growth than its wholesale business. Calculate it any way you want…the results are the same.

- E-commerce grew 50% in the quarter and accelerated on a 2yr basis by 200bps. It now stands at (just) 5.0% of sales, compared to 3.5% last year. Those might sound like small numbers, and they are. That’s why this trend has so much room to grow. Nike states a $7bn goal (e-commerce) by 2020. We think it will be closer to $11bn. That’s an incremental $10bn from the $1.2bn it registered last year. This is where the consensus will prove not bullish enough on Nike, and not bearish enough on its wholesalers (FL, et all…)

- As a percentage of growth, e-commerce accounted for 35% of the incremental dollars in the quarter and DTC (inclusive of Brick and Mortar and e-commerce) made up over $150 of the incremental $300mm in revenue in the quarter. This is the first time we’ve seen that from NKE, ever. And it won’t be the last. *calculation note: we assumed that DTC growth numbers were exposed to the same FX headwind as the 8% company average.

- More importantly, DTC accounted for 60% of the incremental gross profit dollars in the quarter based on our math.

This is the first time EVER that wholesale accounted for less than 50% of incremental profit. This means that Nike itself is now a more important profit driver than all of its traditional customers combined.

Ultimately, this is what should push Nike’s gross margins past 50% (from 46%), which is where $8-$9 in earnings power becomes part of the discussion. That’s what we think you need to believe to own this stock today.

The Quarter – Golf Clap. But 3Q Should Be Big

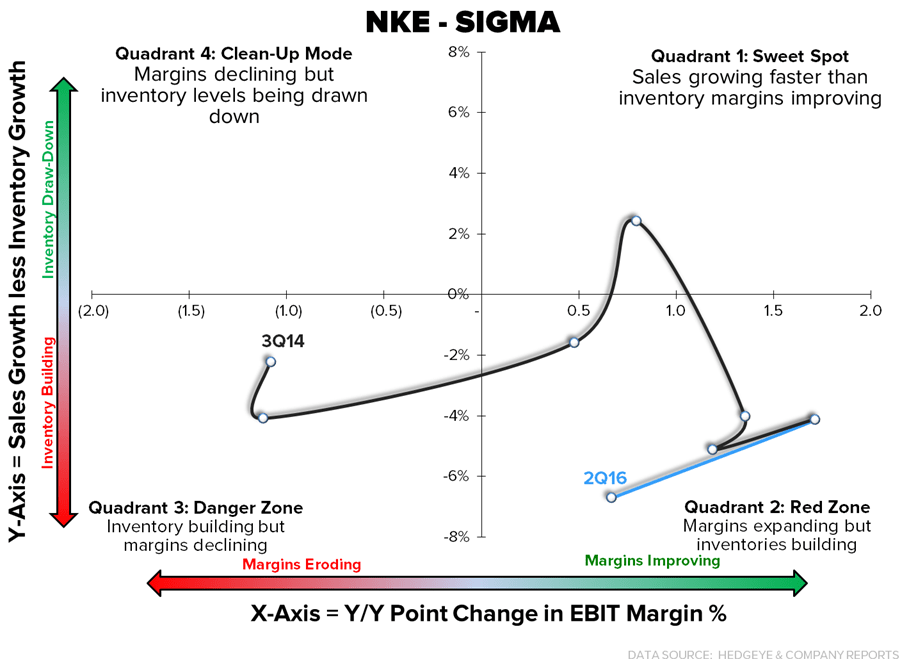

For your average company, this was a great quarter. For an industry-leader like Nike that trades at 27x earnings, it was average – at best. Yes, the futures numbers remain explosive (15% global growth, and 14% North America), and the growth in China is mind-numbing (China is 33% of EBIT, and is growing at 30%+). But keep in mind that the key profit driver – Nike DTC – is not included in the futures numbers. The company actually missed revenue (growing only 4%), despite having put up a healthy 9% futures growth number in 1Q. Gross Margins looked great, thanks to e-comm, but the company would have missed the Street’s EPS expectation by $0.02 if tax rate did not help EPS by $0.06ps. Inventories are still high, as Nike put up the worst sales/inventory spread in 14 quarters – that’s a long time (see SIGMA chart below). Call it West Coast port delay overhang, call it an expeditious move on NKE’s part to reinforce the pull model in the US, but the fact remains that NKE is sitting on bloated inventory levels in its core market for the first time in a decade, and that’s not a positive event for the rest of the athletic supply chain web. The way we see it, Nike was overly conservative in setting 3Q EPS expectations. Nike basically guided top flat EBIT in 3Q, or about $0.90 per share. We think it will do over a buck.

Here’s our comments leading into the Quarter.

12/22/15

NKE | Key Issues

Here’s a quick overview as to what we’re looking for from Nike tonight.

- A Big EPS Beat: We’re at $0.93 vs the Street at $0.86. This company has not missed a 2Q in well over 10 years. It’s not gonna start now.

- Futures. We all know that 9 out of 10 times, the consensus futures estimate is +1/-1 the prior quarter’s 2-year trend. But that only proves to be correct 4 times out of 10. So the question is…are we plus, or minus. Let’s keep in mind that this is an unaudited number that management does not even know until 1-2 weeks before the print. That said, we’re looking for 15% Global C$ growth in Futures, including 10% growth in North America. The latter would represent a 400bp sequential slowdown from 1Q results.

- Bifurcation in Futures and Results. One of the key factors behind our long term call on Nike (and our short on FL) is that Nike is likely to build its e-commerce business from $1.2bn last year to $11bn by 2020. That’s nearly 60% ABOVE the e-comm target Nike gave the Street at its analyst meeting earlier this year. This means two things…

- Futures: At some point, futures will become extremely less relevant, as futures only applies to Nike’s wholesale business. Naturally, we’ll likely hear the company talk about this when there is the inevitable downturn in futures.

- Gross Margins: Gross margins are likely headed well over 50% vs the 46% it reported last year, as e-commerce margins are about 20 points above wholesale.

- E-commerce: We need to see growth this quarter of at least 40%. We’re modeling 50%. It’s going up against a tough comp vs last year (65%), but lets face it…when we’re making a case that e-comm will grow from $1bn to $11bn, going up against a ‘tough comp’ is absolutely irrelevant. Every quarter should be a tough comp, otherwise we’re simply wrong in our thesis.

- US Commentary: Here are a few points that matter a lot, both for Nike and for retailers like FL, FINL, DKS, HIBB, etc..

- Saturation: If we were to ask only one question on the call (we generally don’t ask our questions publicly on conf calls) it would sound something like this, “Over the past six years, Nike has increased its penetration in key wholesale accounts from 40-50%, to 60-80%. At the same time it used the resulting cash flow to invest in the plant, people and systems needed to aggressively grow the leg of distribution – Nike DTC (e-comm) -- that will propel Nike from $30bn in sales to $50bn. With zero square footage growth opportunities for the traditional retailers in the US, and Nike incrementally taking higher ASP product for its proprietary distribution network, how can the traditional retailers actually grow? We understand the ‘innovation agenda’, and the ‘category offense’, but unless Nike convinces the consumer to break out of a 35-year paradigm of per capita purchasing patterns – it seems like we’re at a point where it’s all about price for the legacy retail models. No?”

- Basketball: Not hugely relevant to Nike, but relevant to retailers like FL where about 40% of sales are basketball. FL recently said bball sales slowed, despite a 4% increase in the number of Nike launches during its reporting period, and a 7.4% boost in average price point?

- Inventory Levels: US inventories were elevated at Nike last quarter, and the company noted that it should be cleaned up by the end of Q3 (Feb). We need to see meaningful progress towards this goal, or at least increased confidence that it is being fixed. Reminder, Nike’s confidence in clearing out inventory might be bullish for Nike, but not necessarily the wholesale channel.

On-site Manufacturing: Nike has kept this out of the forefront of the discussion for two years now. But it’s going to be a very relevant, very soon. Aside from driving the DTC model, it will gain even more leverage over retailers who will pay top dollar (in raw cash, working capital, or in margins) to have this technology in stores. We don’t think Nike will talk about this specifically, but we think it becomes a part of the discussion in the next calendar year.