RECENT NOTES

12/21/15 DRI | GREAT QUARTER, DON’T EXPECT ANOTHER ONE SOON

12/17/15 AN OPEN LETTER TO THE CEO OF CHIPOTLE FROM HIS PEER GROUP

12/16/15 DRI | ONE LAST GOOD QUARTER

12/11/15 YUM | INVESTOR DAY IN REVIEW

12/9/15 CMG | WHO WILL BENEFIT FROM THEIR STRUGGLES? (ZOES, PNRA, QDOBA, CHUY, MCD)

SECTOR PERFORMANCE

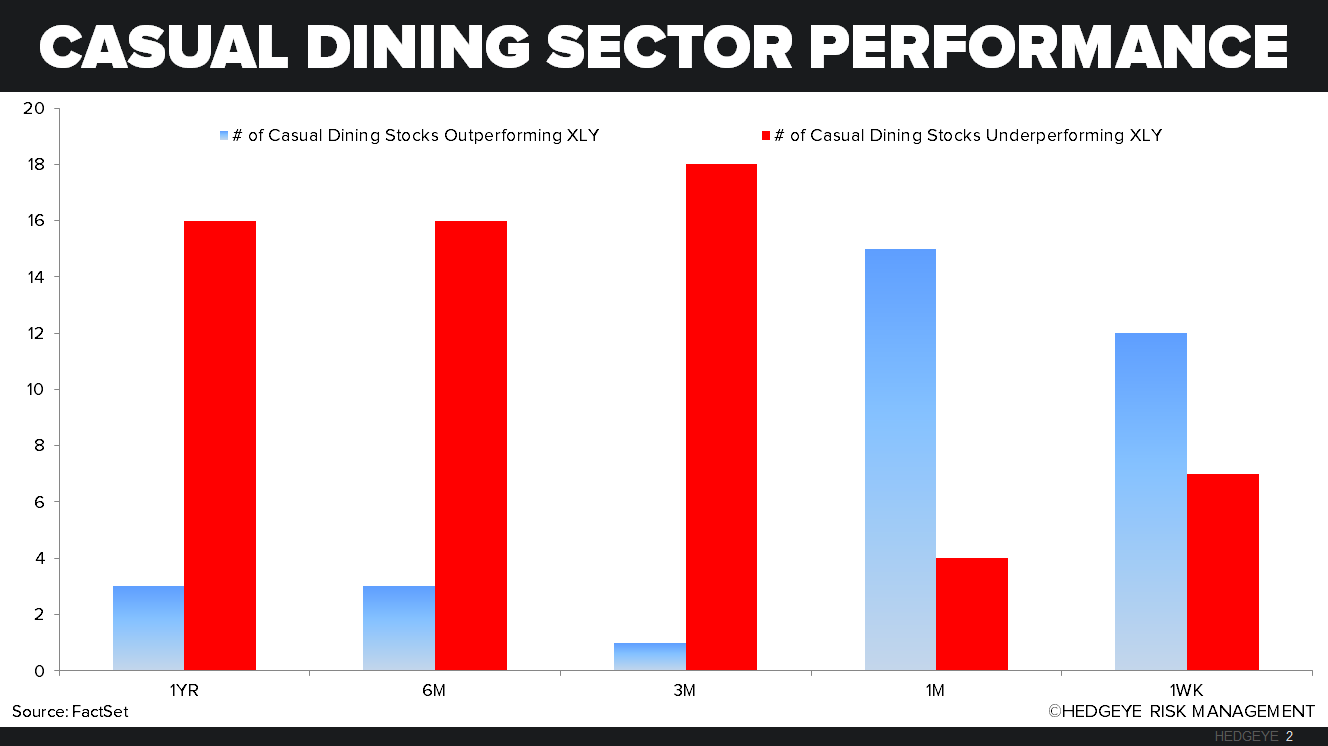

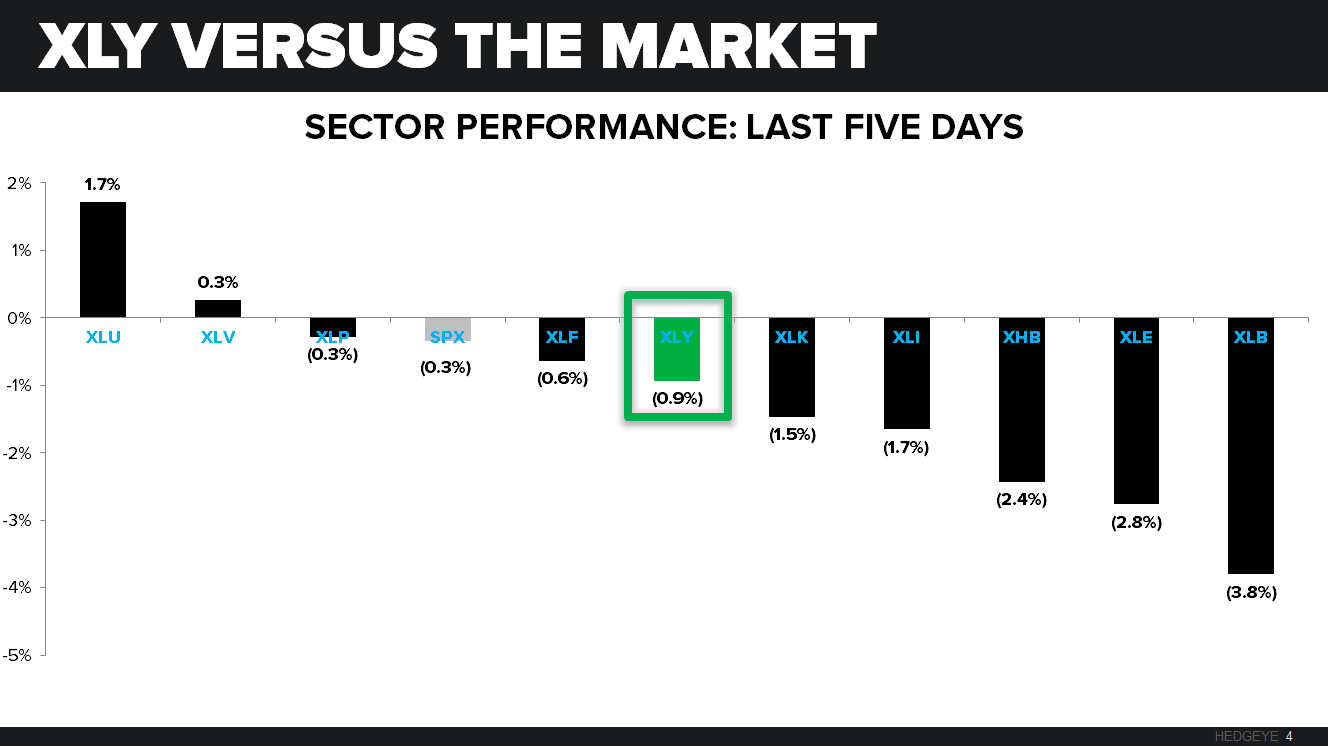

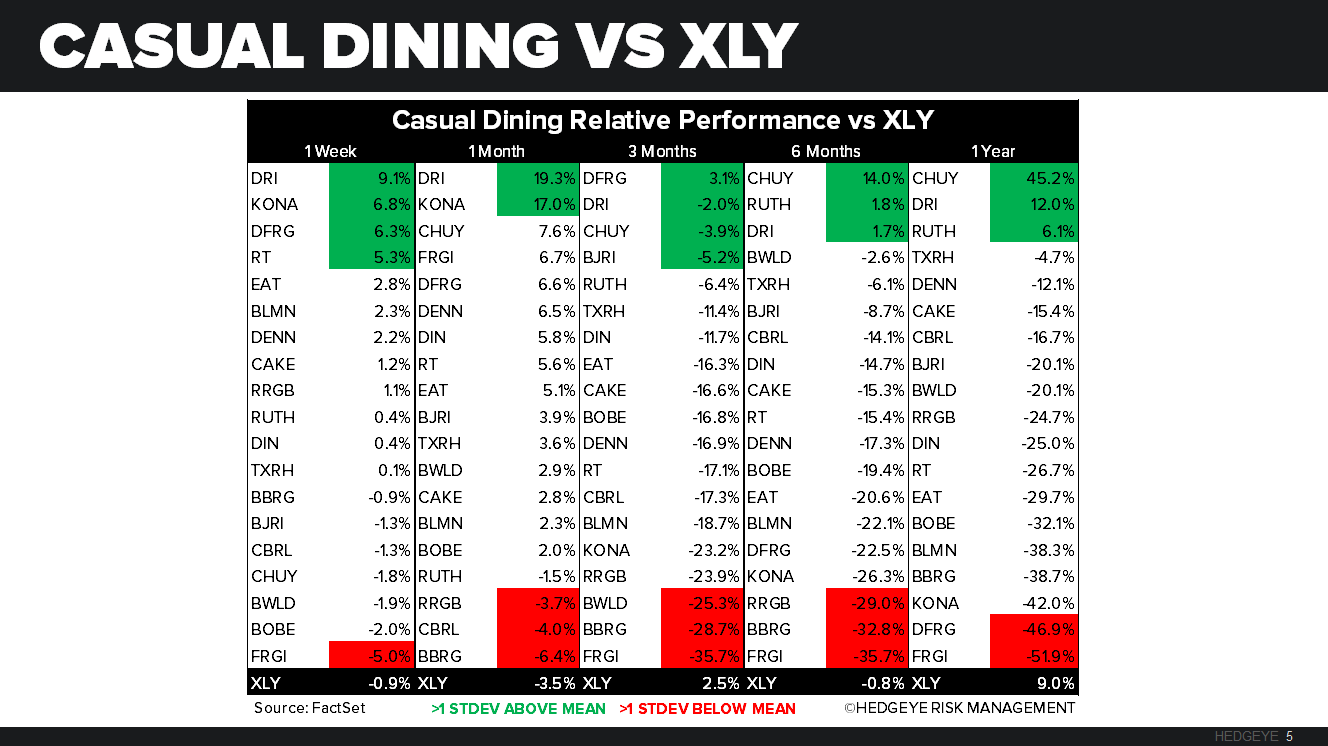

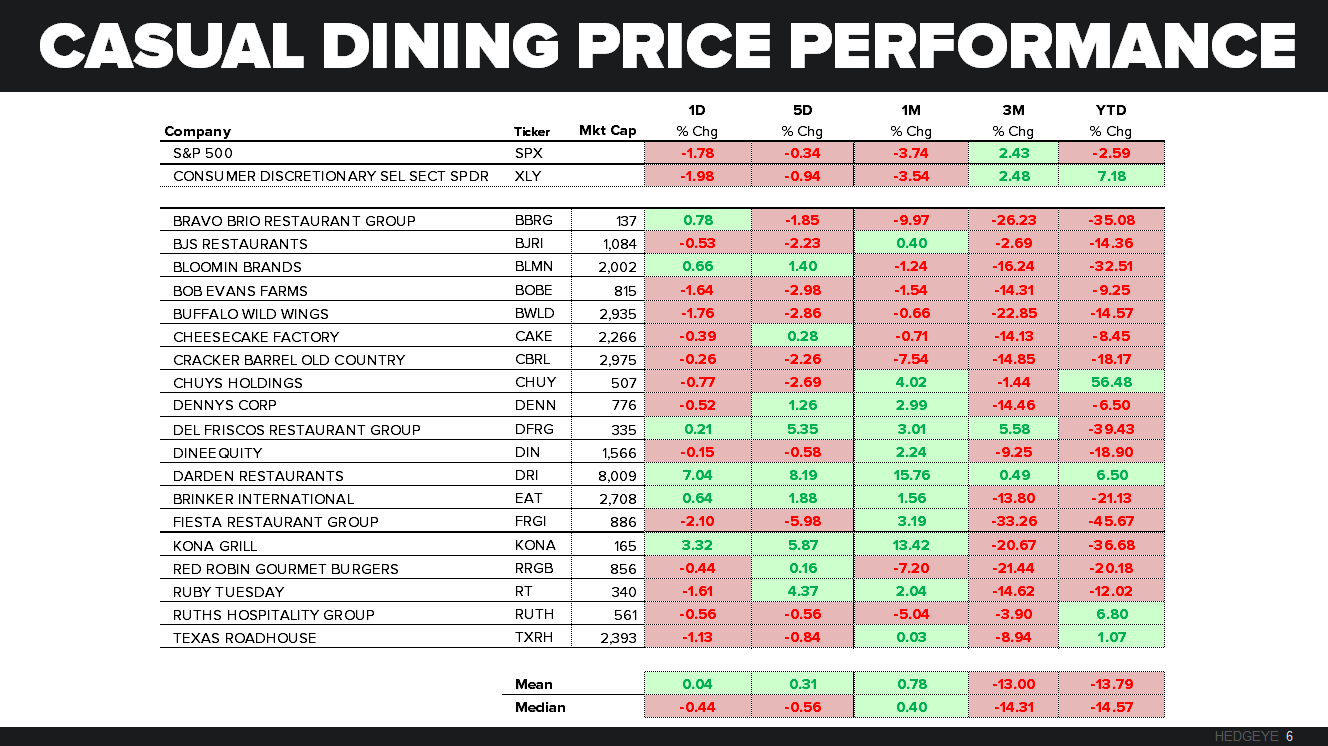

Casual Dining and Quick Service stocks that we follow outperformed the XLY, last week, which was down -0.9%. Top performers on a relative basis from casual dining were DRI and KONA posting increases of +9.1% and +6.8%, respectively, while NDLS and JMBA led the quick service group this week up +3.9% and +3.6%, respectively.

XLY VERSUS THE MARKET

CASUAL DINING RESTAURANTS

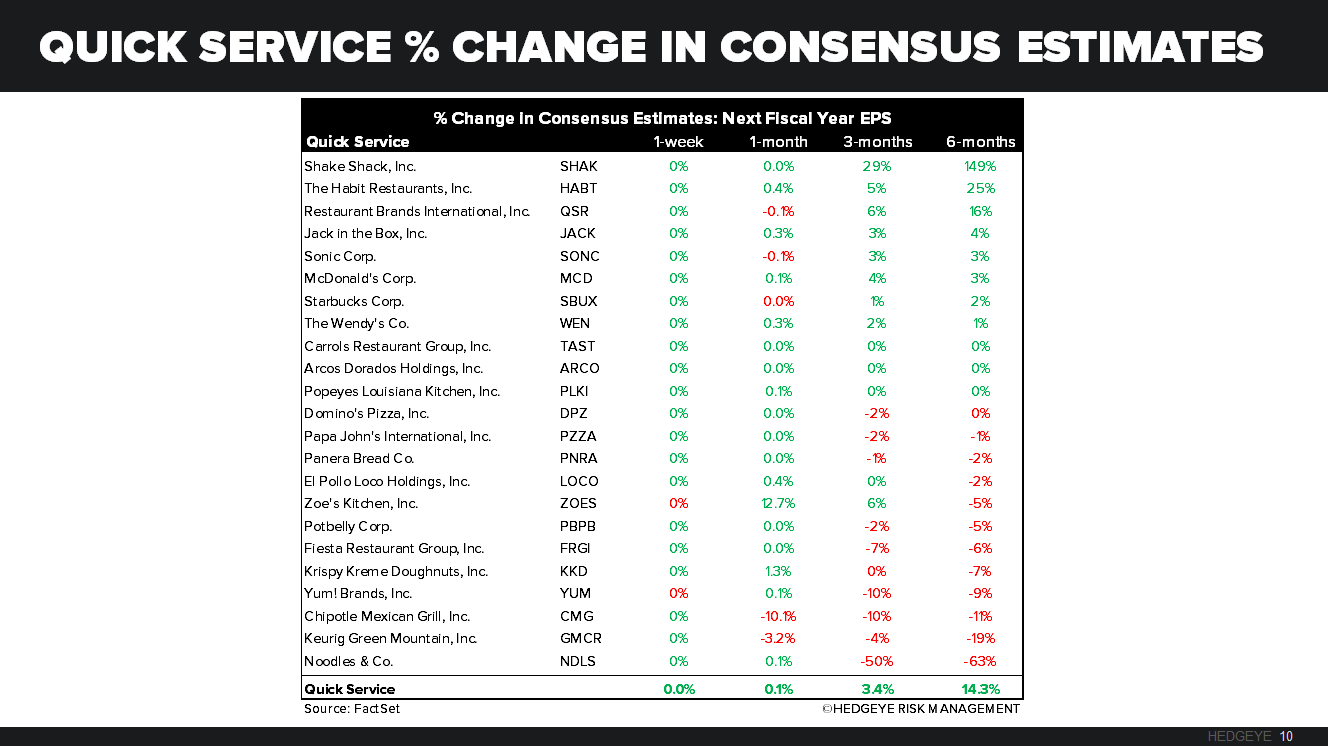

QUICK SERVICE RESTAURANTS

Keith’s Three Morning Bullets

The Fed tightened into a slow-down last week and perpetuated #deflation in doing so…

- VIX – with the SP500 -3.6% for DEC, front-month VIX is back up at 20.70 – more importantly, it’s risk range is now 17.84-24.83 and this breakout on our TREND duration has been brutal for High Beta as a Style Factor, which was down another -2% last wk

- SPAIN – down hard in a generally up tape for European Equities this morning – post the Spanish election the IBEX is -2% (-7.5% in the last month) while the 10yr Yield for Spain is +11bps to 1.80%; I still think Draghi wants to snap Euro $1.05 vs. USD

- OIL – down another -0.6% this morning to $34.49 after deflating another -3% last week - #Deflation is not “transitory”, it’s been pervasive and since the US is in an industrial recession right now, it’s finding its way into revs/earnings for 1H 2016

SPX immediate-term risk range = 1; UST 10yr Yield 2.12-2.32%

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst