Our FHQ (Friday Housing Quant) tables present the state of the publicly traded homebuilders in a visually-friendly, quantitative format that takes about 60 seconds to consume.

Takeaways:

- Performance Roundup: Housing has become a bit of a bifucated beast in the last week or two. Interestingly, ITB is +5.3% QTD, trailing only slightly the S&P 500 at +6.9%, but this is a bit of cherry pick as ITB contains only 10 stocks and its largest 3 holdings: DHI, LEN and NVR happen to be the three best performing builders. XHB is +2.3% for the QTD and the average builder we track is -1.6% with the median builder down -2.9% QTD. We think the weakness is a confluence of rate-driven concerns ahead of the Fed meeting next week, ongoing jitters around the Houston market and residual profitability angst following TOL's 4Q. Our preferred four horsemen of 4Q among builders are NVR, LEN, BZH & KBH, which are +8.9%, +3.4%, -6.9%, and -4.1%, respectively. The three best performing builders thus far this quarter are DHI (+10.2%), NVR (+8.9%) and LEN (+3.4%), while the three worst performing builders are TMHC (-13.8%), BZH (-6.9%), and MTH (-5.8%).

- Insider Buying: Other than the Director at Hovnanian (HOV) who purchased 20k shares (~$45k) in late October, there's been no recent insider buying in the sector.

- Beta: The highest beta names (1YR) remain HOV (1.55), KBH and BZH which are at 1.32 and 1.35, respectively. At the other end of the spectrum, the lowest beta plays are NVR (0.65), MDC (0.97) and TOL (1.00).

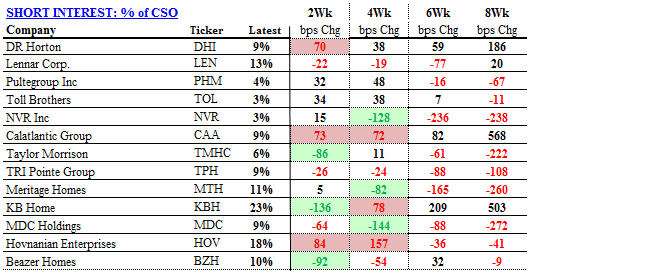

- Short Interest: CAA, HOVand DHI have seen SI creep higher, rising by the most in the group in the last 2 wks. TMHC, KBH & BZH have seen SI fall by the most.

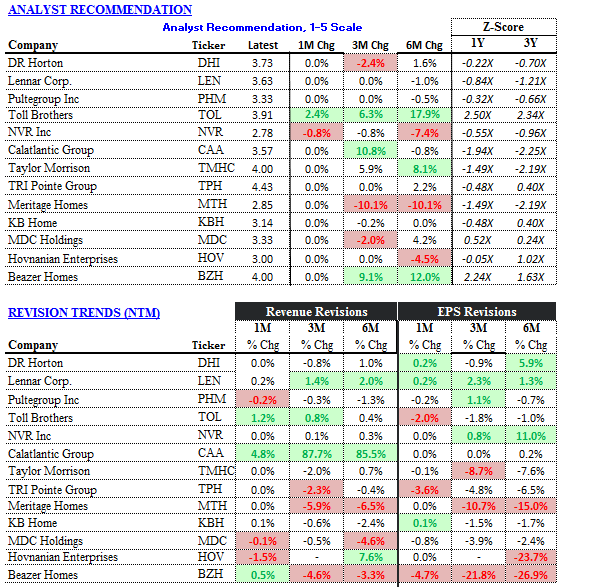

- Sell Side Sentiment: Brokers have become marginally more bullish on TOL (+2.4%) and less bullish on NVR (-0.8%) in the latest month.

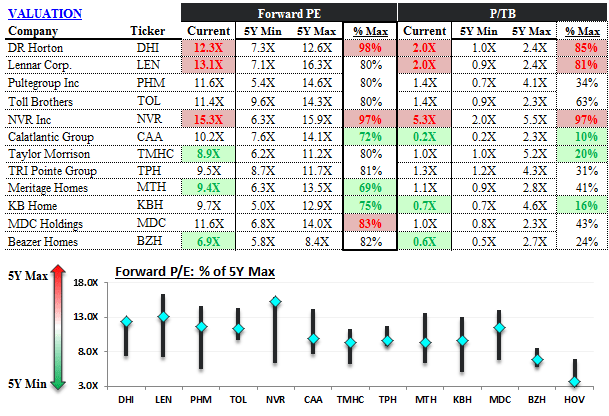

- Valuation: The cheapest names in the group currently are BZH (6.9x), MTH (9.4x) and TMHC (8.9x), while the most expensive are NVR (15.3x), LEN (13.1x), and DHI (12.3x). Incidentally, NVR, at 5.3x TBV, is currently at 97% of its peak 5-year valuation. DHI and LEN, both at 2.0x P/TB are at 85% and 81% of their 5-year peak multiples.

Joshua Steiner, CFA

Christian B. Drake