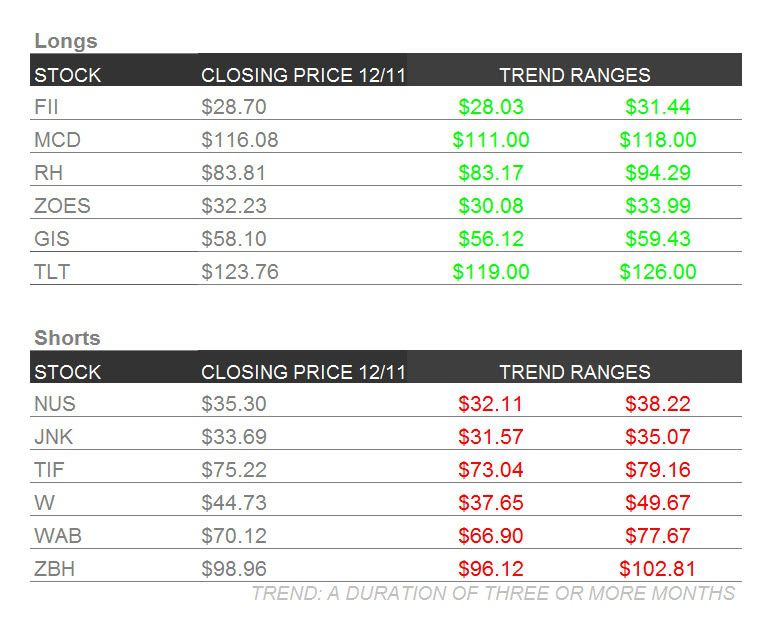

Below are our analysts’ updates on our twelve current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this. Hedgeye CEO Keith McCullough’s updated levels for each ticker are below. Please note that we removed LinkedIn (LNKD) this week.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

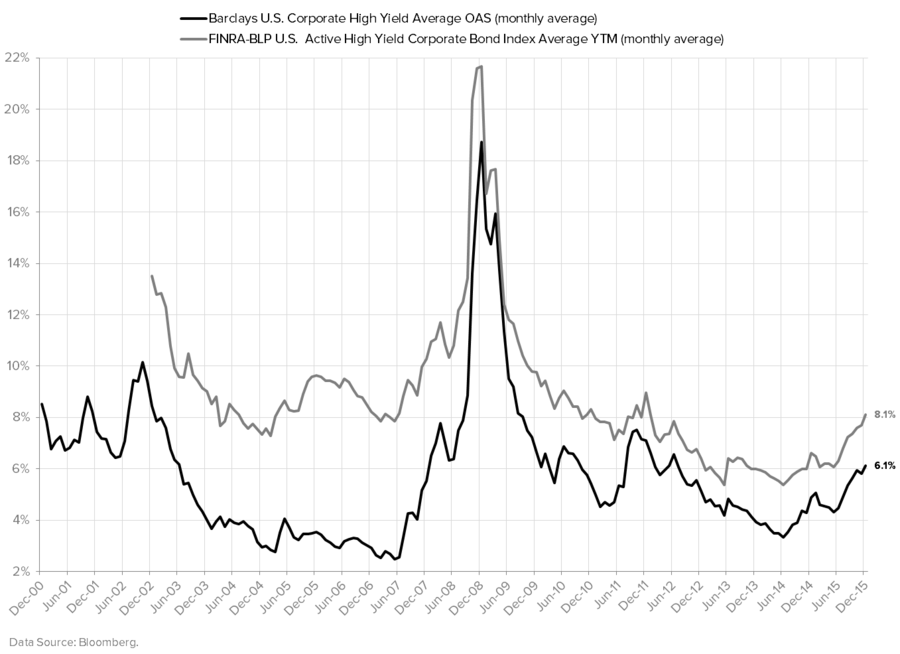

TLT | JNK

To view our analyst's original report on Junk Bonds click here. Below is an update on our Long TLT and Short Junk positioning written by Senior Macro analyst Darius Dale:

Is the Spread Widening Trade a Win-Win From Here?

Implicit in our long TLT/short JNK bias is an expectation for high-yield spreads to continue along their recent trend of widening throughout the YTD. As we penned in our 12/10 note titled, “Five Charts That May Make You Feel Uneasy About 2016”:

“All told, we continue to see exceptional risk in searching for an investable bottom in equities at this stage in the economic cycle. Perhaps the ongoing deterioration within the high-yield credit market is as much of a warning signal about the business cycle as it was back in 2007 – and this has occurred prior to any rate hikes out of the FOMC.”

Inclusive of Friday’s retails sales, PPI, consumer confidence and wholesale inventories data, we remain appropriately bearish (see charts and tables below) on the domestic (and global) economic cycle. Our dour intermediate-term outlook was most recently highlighted in the aforementioned note, as well as in our 12/9 Early Look titled, “Conviction Sells”:

“The U.S. economy is #LateCycle and the probability of a recession commencing by mid-2016 is extremely elevated – both in absolute terms and relative to the belief held by the overwhelming majority of investors and policymakers. Moreover, the risk of a global recession is also great in this scenario.”

Click the images below to enlarge.

The economic cycle doing what it always does (i.e. decelerate into a recession before bottoming and then reaccelerating) is reason enough to be bullish on the long bond and bearish on junk bonds, which are accelerating into full-blown crisis mode (the JNK ETF declined another -2% on Friday and is down -4.1% WoW, -5.8% MoM and -12.7% YTD).

Is the Third Avenue Credit Fund blow-up a canary in the coal mine for a substantial deepening of the junk bond illiquidity crisis? While we can’t know for sure, our research would suggest there are quite a few more cockroaches to be uncovered by the time it’s all said and done. Thus, developments such as these are definitely worth keeping on your screens:

(WSJ article HERE)

Enjoy the rest of your weekend, risk managers – you deserve it.

DD

NUS

To view our analyst's original report on Nu Skin click here.

The success of the Nu Skin (NUS) short, in large part, is dependent on government action. As we have stated, the SEC is currently investigating NUS for charitable contributions in China, which could easily expand once they are under the hood.

In the 2015 Investor Day press release, NUS added additional language to their risks and uncertainties disclaimer. It reads, “risk that litigation, investigations or other legal matters could result in settlements, assessments or damages that significantly affect financial results.”

Conveniently tucked away about three-quarters of the way into the paragraph this language signals to us that the SEC investigation is very real and could pose a threat to them. Although it would be pure speculation to think what the meaning of this is, we believe that the SEC investigation is coming to a head, and could have grown larger than its original scope.

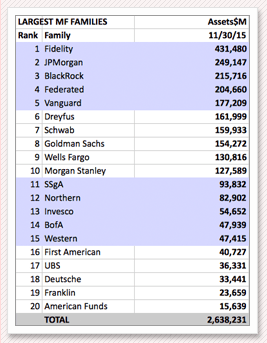

click the image below to enlarge.

FII

To view our analyst's original report on Federated Investors click here.

During the week, leading money fund manager Federated Investors (FII) closed on the small lift out of the money market assets of Huntington Asset Advisors, rolling in an additional $930 million in assets-under-management.

While the deal adds just +0.5% to FII’s existing money fund AUM of over $200 billion, lift out deals are immediately accretive as they come with little incremental operating infrastructure and represent a sub-scale manager ceding assets to a bigger more capable player.

Exiting the Financial Crisis in 2008, there were over 125 money market fund managers. Now, that number has been whittled down to just 75 providers. We foresee less than 30 providers over the next several years giving FII plenty of other accretive roll up deal opportunities.

This reduction in industry capacity is another way that Federated can increase its AUM along with late cycle flows out of risk assets and back into cash on the sidelines.

FII is a top 5 money fund manager behind Fidelity, JP Morgan, and BlackRock.

WAB

To view our analyst's original note on Wabtec click here.

Following the congestion driven surge in demand / Tier 4 pre-buy, locomotives are being stored even while the total equipment fleet is young. Equipment heading to storage hurts Wabtec (W) in two ways:

- As equipment heads to storage, why would new equipment demand increase?

- Second, WAB’s aftermarket business is hit as their customers choose to either delay maintenance and/or scavenge for parts off of stored equipment.

As we see it, equipment coming out of storage helped boost aftermarket activity, while equipment returning to storage may depress it. This is particularly problematic with slowing freight rail capital spending on equipment likely to decline for 2016.

TIF

To view our analyst's original report on Tiffany click here.

In regards to our Tiffany (TIF) short thesis, the key question we ask is why do earnings NEED to grow next year. If TIF is going to have a flat year in FY15 in an otherwise decent US and Global economy, what kind of consumer climate do we need to assume in 2016 to get earnings higher?

That’s an especially interesting question given the following…

- Sales productivity is at a historical peak of ≈$3,450

- A Brand that might be "Great" to the person typing this note, but one that is simply ‘Very Good’ to Millennials.

- Minimal square footage opportunity (2% long term)

- A business that structurally does not lend itself to online (only 6% of sales)

- Gross Margins currently at peak levels of 60%

- EBIT margins still at 19% this year despite the company’s challenges – with 2-3 points of potential downside.

We'll stick with our short call.

W

To view our analyst's original report on Wayfair click here.

On Thursday's Q/A call, RH management had some clear comments about the promotional environment in the mid-tier furnishings channel. They indicated that this holiday season was the most promotional they had ever seen by a meaningful margin. Many of the players in the furnishings space are accelerating email campaigns and increasing discounts. This is not a positive sign for Wayfair's (W) fourth quarter margins, especially when you consider that its cost structure is not fixed and predicated on ad-spend and price to attract customers to its platform.

It is undeniable that Wayfair is taking share while growing revenue at an industry leading rate. However, the bottom line is that this company is spending – and spending big – around penetrating what management believes to be the company’s TAM. Unfortunately, we think they are overestimating it by a country mile, and are building an infrastructure for growth that will not materialize – at least not profitably.

RH

To view our analyst's original report on Restoration Hardware click here. Below is an excerpt from from our Retail team's note ("RH - Lost in Translation") sent to institutional clients earlier this week.

"This Restoration Hardware (RH) quarter is going to draw a Mason Dixon line between the Bulls and the Bears. On one hand, the key factors that the Bulls (including us) need to see were profoundly present – giving us confidence that revenue will double, that we’ll see a 16% operating margin, and $11 in earnings power. In addition, RH beat the quarter, delivered 33% EPS growth in what should be the slowest growth quarter of the year, and it took up 4Q revenue guidance based on what it’s seeing so far this quarter (to 20%+).

On the flip side, the Bears got a nice little gift in the form of weaker Gross Margins due to promotional activity, and renewed concerns about management. The reality is that this is a transformational growth story that will change on the margin more often than it doesn’t.

Even though the 30% short interest already captures a whole lot of bad news, this print won’t make people cover – and probably validates the pressure the stock came under earlier this week. We’ll respect it for what it is, but based on our confidence in the earnings power at play here, we’d use any weakness as an opportunity to buy.

The market combined with noise around the evolution of this story gives you a shot at buying it on the cheap every six months or so. We’re thinking that this is one of those times."

MCD

To view our original note on McDonald's click here.

McDonald's (MCD) remains one of our top LONG ideas in the restaurants space. All indications are that all day breakfast is working, bringing back old customers and driving growth of new customers. Customers are pairing both breakfast and lunch items together in the lunch and dinner day, part which is helping drive additional sales.

McDonald’s Canada opened its first standalone McCafe this month. The much simplified concept intends to appeal to customers by offering both speed of service and low cost. They intend to be faster than their main competitor Tim Hortons and cheaper than Starbucks, carving out their own niche in the market.

ZBH

To view our analyst's original report on Zimmer Biomet click here.

Healthcare analyst Tom Tobin has no material update on Zimmer Biomet's (ZBH) but his bearish thesis on the company is firmly in tact. Here are some key highlights from Tobin's original call on ZBH that are well worth a second look:

- "The demographic drivers of knee joint replacement are well past peak and in a secular decline."

- "Affordability of medical spending has peaked in the United States with deflationary pressures mounting and being expressed through policy changes alongside the broadening adoption of IT systems."

- "Medicare recently initiated an aggressive global payment policy (CCRJ) which we expect to create a strong incentive for providers to pressure device costs."

- "We believe the #ACATaper is emerging over the coming months as the newly insured revert to spending levels similar levels as seen with typical insured populations."

- "The Biomet merger (while accretive) is not the solution for ZBH shares. Cost synergies are rarely a positive when organic growth is slowing."

GIS

General Mills (GIS) reports 2Q16 earnings next Thursday, the 17th before the market opens. GIS remains one of our core LONG ideas in the consumer staples sector and in the market overall because of its strong brands and style factors that are in favor. GIS boasts high-cap, low-beta and high liquidity, all good things to have in a volatile market.

ZOES

Zoës Kitchen (ZOES) is a company with style factors that are out of favor currently, high beta and low-cap. But this is a long-term story and you must remember that during these volatile trading days. Furthermore, we suggest that you buy big on the dips, but don’t expect to get out of the position clean in the near-term.

Now that Chipotle (CMG) customers aren’t going within 100 ft. of one of their restaurants, we thought about who would benefit most. From the standpoint of stealing the most share from CMG, it’s probably not ZOES just due to their comparitively small size. But ZOES looks to have the best opportunity to draw in new customers that they hadn’t been able to attract before.

Their concepts although dissimilar in type of cuisine, are similar in that they both offer a premium, better for you option, at a fair price, and with fast service. ZOES’ restaurants are conveniently and strategically located to take advantage of the opportunity, 80.1% of ZOES restaurants are within five miles of a Chipotle. This only represents roughly 15.3% of Chipotle’s restaurants but that amount will be under significant threat from a very capable competitor.