The main takeaway on the labor front this week is that while the US more broadly muddles further along, the energy economy is hemmorhaging. The chart below shows the spread continuing to widen between our energy state basket and the rest of the US. For reference, we use 8 states: AK, LA, NM, ND, OK, TX, WV & WY to derive our energy state basket. The gap between our two indexed series widened another 4 points to 46 for the week ended November 28th. The most recent dip in energy prices has yet to be reflected in the numbers.

Company's with material exposures to energy hubs such as Houston and Calgary will see headwinds grow for some time. This is why we remain short the Canadian Banking complex. Western Canadian companies with outsized exposure to this phenomenon include Canadian Western Bank (CWB-TSE), Genworth MI Canada (MIC-TSE), CIBC (CM) and Royal Bank of Canada (RY). For reference, initial claims trends in Alberta are similar to those in our 8-State US energy basket.

The Data

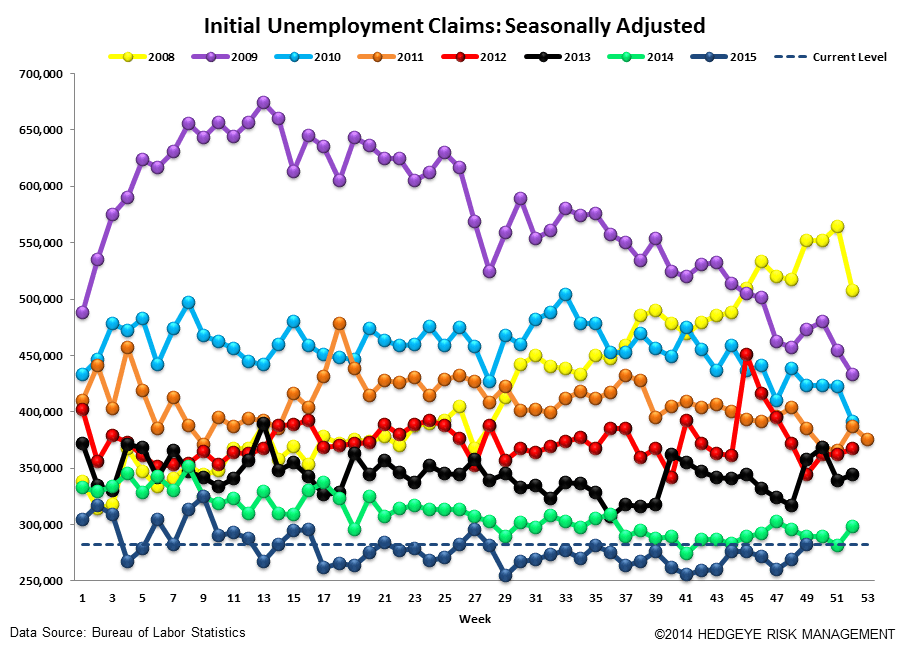

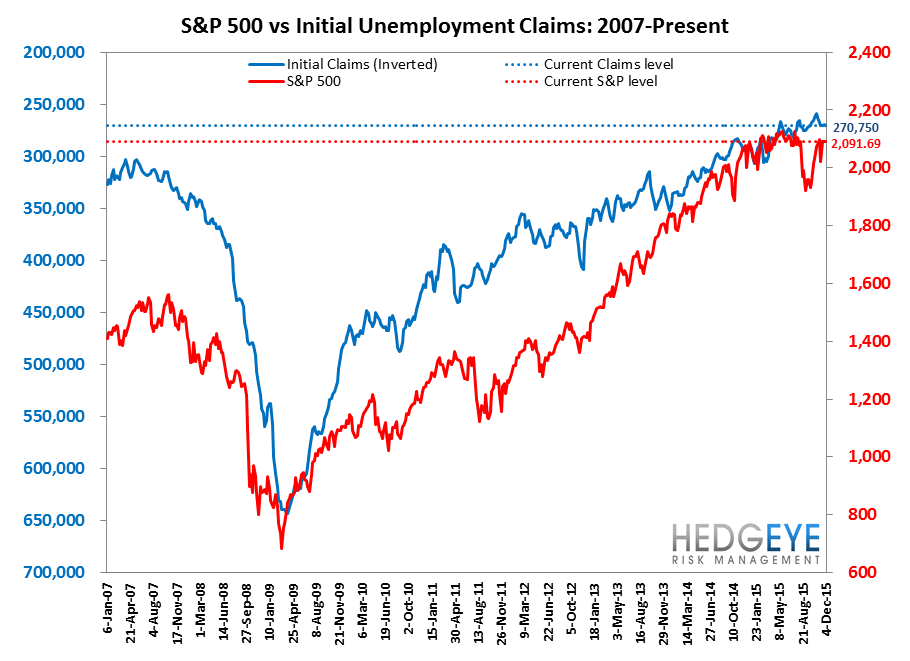

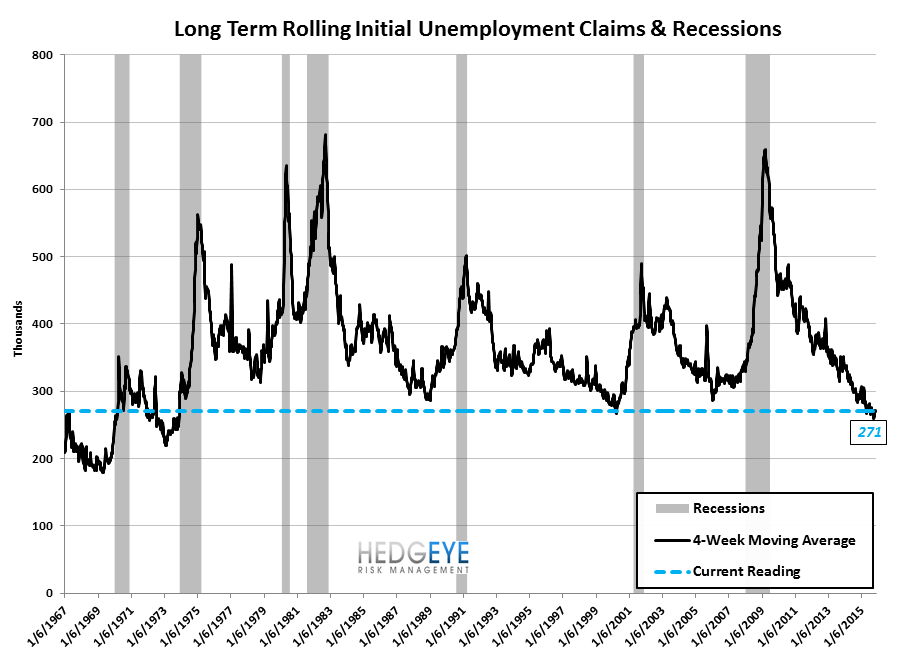

Initial jobless claims rose 13k to 282k from 269k WoW. The prior week's number was unrevised. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 1.5k WoW to 270.75k.

The 4-week rolling average of NSA claims, another way of evaluating the data, was -8.3% lower YoY, which is a sequential slow down versus the previous week's -9.9% rate of change.

<chart19>

Yield Spreads

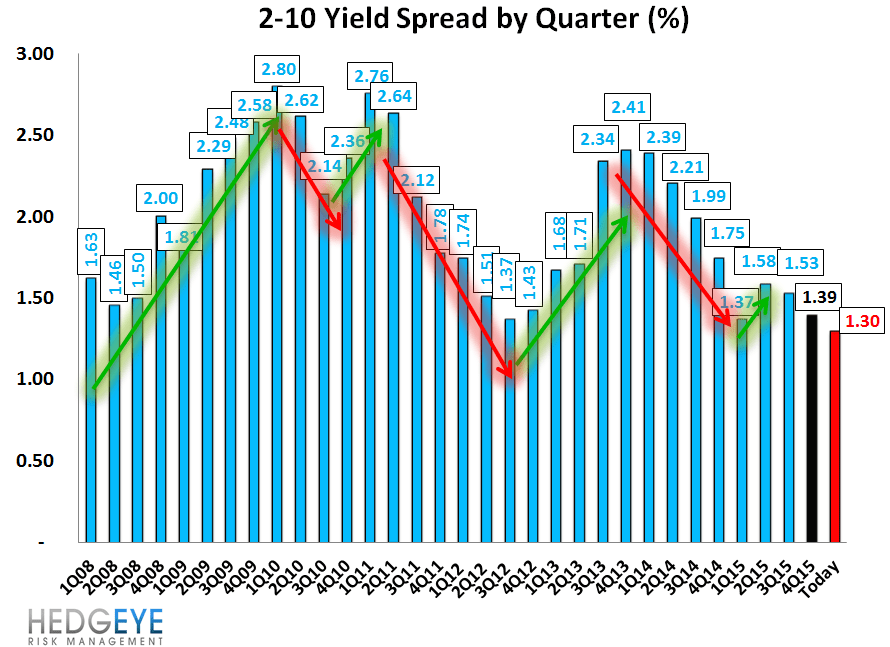

The 2-10 spread rose 6 basis points WoW to 130 bps. 4Q15TD, the 2-10 spread is averaging 139 bps, which is lower by -14 bps relative to 3Q15.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT