W - Wayfair Cyber Five Sales Results

Our Take: These Holiday sales numbers for Wayfair are big with direct sales up 130% this year and up 103% on a 2yr basis. Management called out the fact that it would up the ante during this holiday season in areas like seasonal décor, housewares, etc. as it realized last year that could play the Black Friday game in areas less tied to furniture and more directly competitive with retailers like Bed Bath, Target, Walmart, Kohl’s, etc. While the press release came 6 weeks ahead of last year's, there was no comment this year on the number or percent of orders that were placed by repeat customers which is an interesting omission in its own right.

Also, let’s not forget two things 1) most people did not know what Wayfair was last Black Friday, and 2) people don’t use Black Friday as an excuse to buy higher-ticket/margin furniture.

The bottom line on Wayfair is that this company is spending – and it’s spending big – around penetrating what management believes to be the company’s TAM. Unfortunately, we think they are overestimating it by a country mile, and are building an infrastructure for growth that will not materialize – at least profitably.

Recession Watch - Macro Comments from Hedgeye CEO Keith McCullough

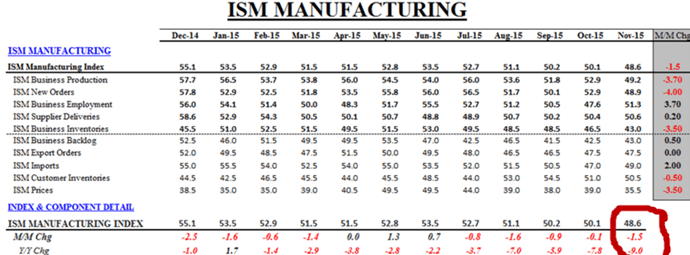

ISM bomb of 48.6, but no worries – if you back out company selling prices alongside strong dollar/weak demand deflation, and don’t look at US Retail Sales and/or consumption growth slowing from Q1 cycle peak – all good.

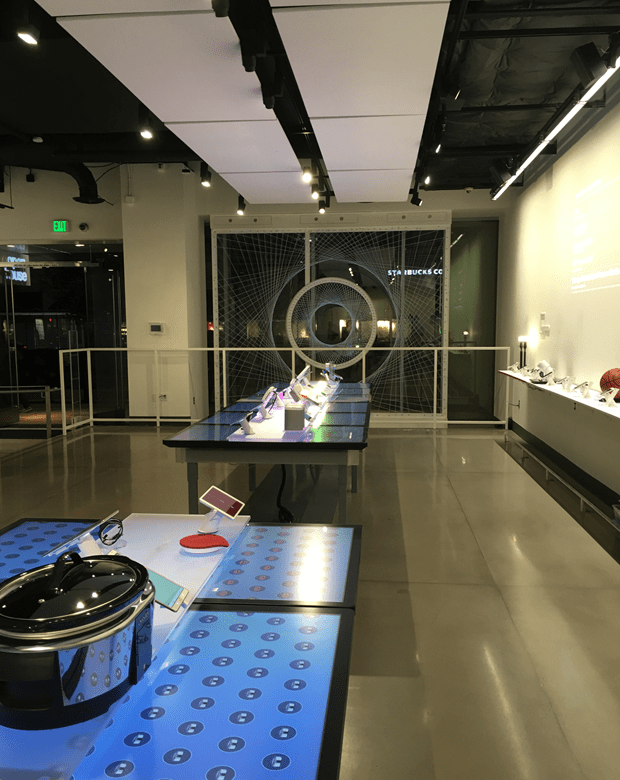

TGT - Target's Connected Open House

(https://corporate.target.com/article/2015/07/open-house-connected-home)

Our Take: This might be the coolest thing that Target has done since exiting Canada. This is a store in San Francisco we visited last night that is basically a prototype for TGT to embrace IoT. They’re selling the ‘connected home’ experience with everything from smart thermostats, door locks, baby scales, light bulbs (for $199 3-pack) to dog collars (think doggie Fitbit).

This is in no way scalable, bc you could buy half of this stuff in Home Depot. But the reality is that we give Target an A for effort on this one.

AdiBok - Adidas looking to sell-off hockey brand CCM, along with Taylormade

(http://nypost.com/2015/12/01/adidas-looking-to-sell-off-hockey-brand-ccm/)

WMT, AMZN - Amazon Received 12 Times as many Twitter mentions than Walmart on Cyber Monday

(http://fortune.com/2015/12/01/amazon-walmart-cyber-monday/?xid=yahoo_fortune)

GIII - 3Q16 Earnings

OXM - Michelle McQuality Kelly to Succeed Scott A. Beaumont and James B. Bradbeer, Jr. as Group CEO of Lilly Pulitzer

(http://investor.oxfordinc.com/releasedetail.cfm?ReleaseID=945052)

CAB - Cabela’s Inc. to Explore Strategic Alternatives

(http://phx.corporate-ir.net/phoenix.zhtml?c=177739&p=irol-newsArticle&ID=2119452)

SVU - SUPERVALU Names Eric Claus New Chief Executive Officer of Save-A-Lot

(http://www.supervaluinvestors.com/phoenix.zhtml?c=93272&p=irol-newsArticle&ID=2119548)