In a note to subscribers this morning, Hedgeye CEO Keith McCullough highlighted a few recent market developments that he's watching today:

"It was another strong bounce-back morning for the greenback +0.4% vs. the Euro is taking the commodity crash right back to the woodshed – Oil -1.5% post yesterday’s +2.8% bounce (which helped Energy stocks lead the US equity rally off the lows intraday) - #Deflation Risk = On."

This evolving story has everything to do with monetary policy as the Yellen Fed looks to tighten in December while the ECB and Draghi ease. It's no surprise that the dollar is strengthening.

In other central planning news, the gap between 10yr and 2yr U.S. Treasuries is closing on speculation of a December rate hike. More analysis from McCullough:

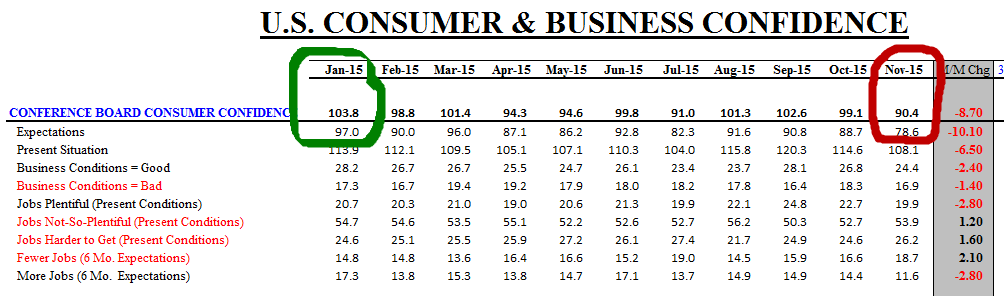

"The yield curve continues to compress as the US economic data slows (Corporate profits -3.2% Q3 and Consumer Confidence tanked to 90.4) – this week the 10s/2s spread has compressed another 6bps to +129bps as credit trades like 1,000 pounds of stale pumpkin in a 100lb bag."

That further compression of the yield curve came after last week's -9bps.

Then again, the Fed apparently doesn't seem too concerned about raising rates into a slowdown. Here's the most recent spate of #GrowthSlowing data. Note the January peaks.

Consumer Confidence

Consumer Spending

Do you see any economic green shoots? We don't.