As an oilman, I hope that you'll forgive just good old-fashioned plain speaking.

- Daniel Plainview, There Will Be Blood (I'm An Oil Man Speech)

Let's speak plainly. The trend in energy state claims (chart below) shows the spread between indexed claims in energy states and the country as a whole has steadily increased from a low of 3 in early July to 34 as of the most recent reading for the week ending November 14. Energy hedges are rolling off broadly as the end of 2015 approaches. We expect this emergent acceleration in the deterioration in labor conditions throughout the energy patch to continue into 2016.

The takeaway here is that company's with high relative exposures to energy hubs like Houston and Calgary will see headwinds continue for some time.

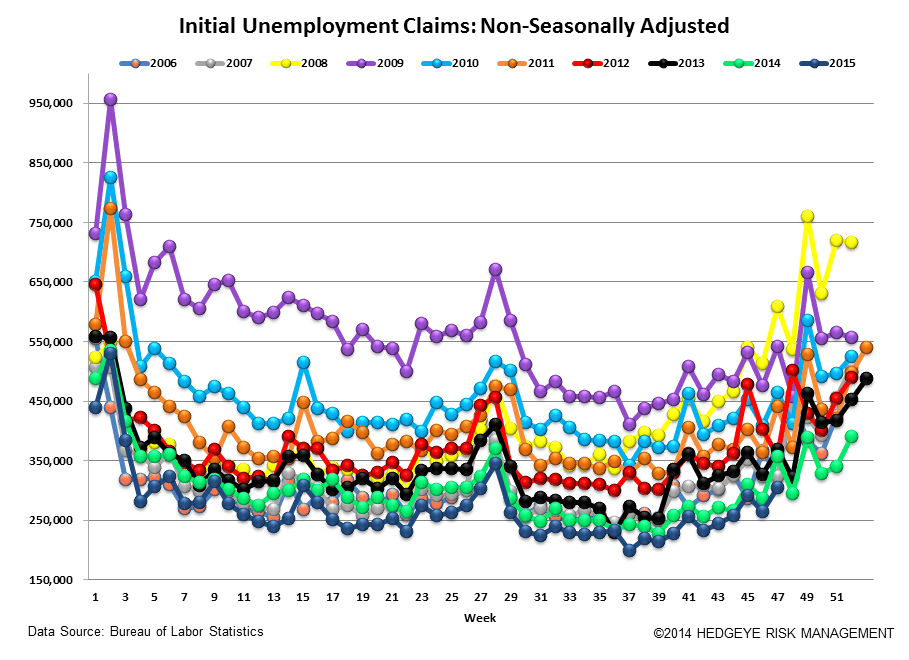

Meanwhile, the rest of the country continues, for now, to exhibit decent performance as evidenced by the fact that non-energy states are collectively more than offsetting the weakness in the energy footprint. Overall, initial jobless claims showed week-over-week improvement with the SA figure falling from 272k to 260k and the year-over-year rate of change in rolling NSA accelerating slightly from -6.5% to -8.2%.

The Data

Prior to revision, initial jobless claims fell 11k to 260k from 271k WoW, as the prior week's number was revised up by 1k to 272k.

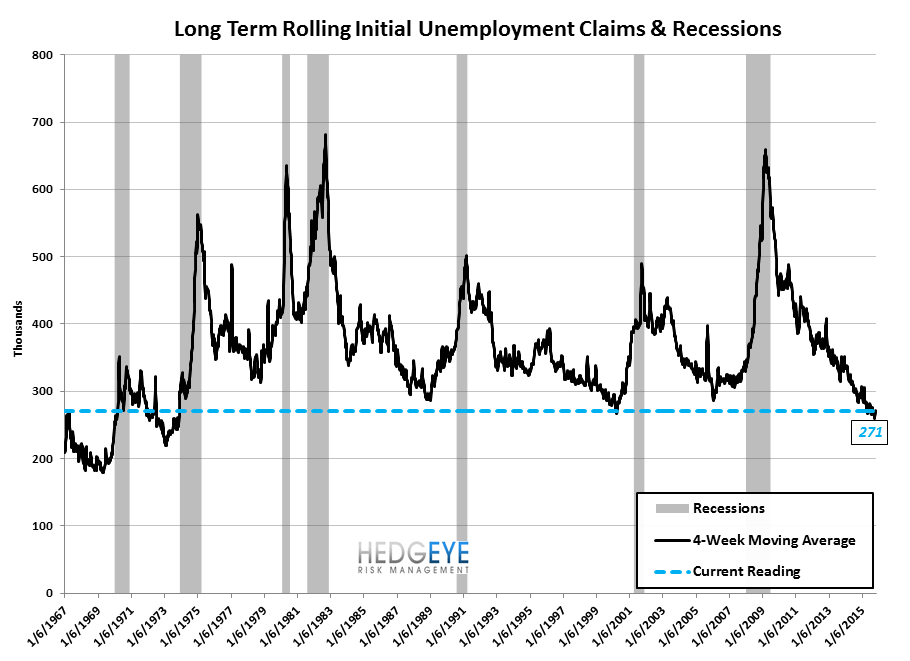

The headline (unrevised) number shows claims were lower by 12k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims was stable at 271k.

The 4-week rolling average of NSA claims, another way of evaluating the data, was -8.2% lower YoY, which is a sequential improvement versus the previous week's YoY change of -6.5%

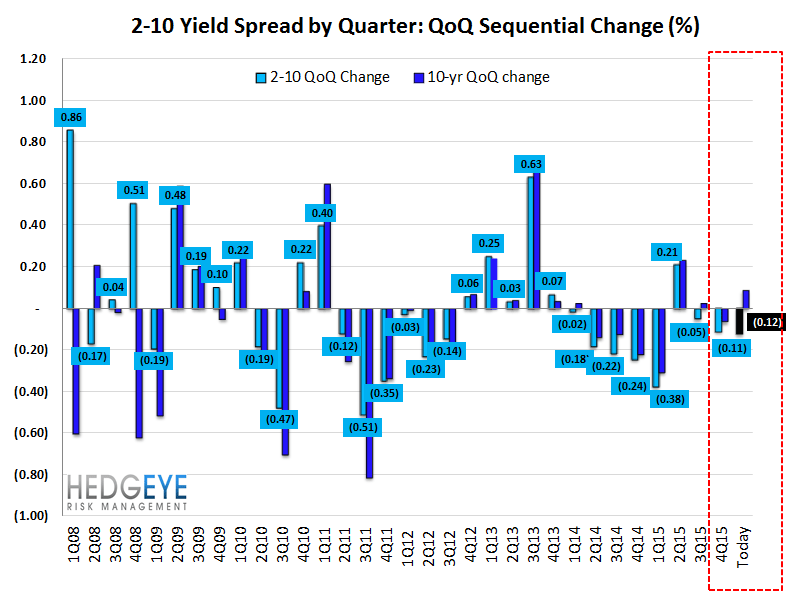

Yield Spreads

The 2-10 spread fell -10 basis points WoW to 130 bps. 4Q15TD, the 2-10 spread is averaging 142 bps, which is lower by -11 bps relative to 3Q15.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT