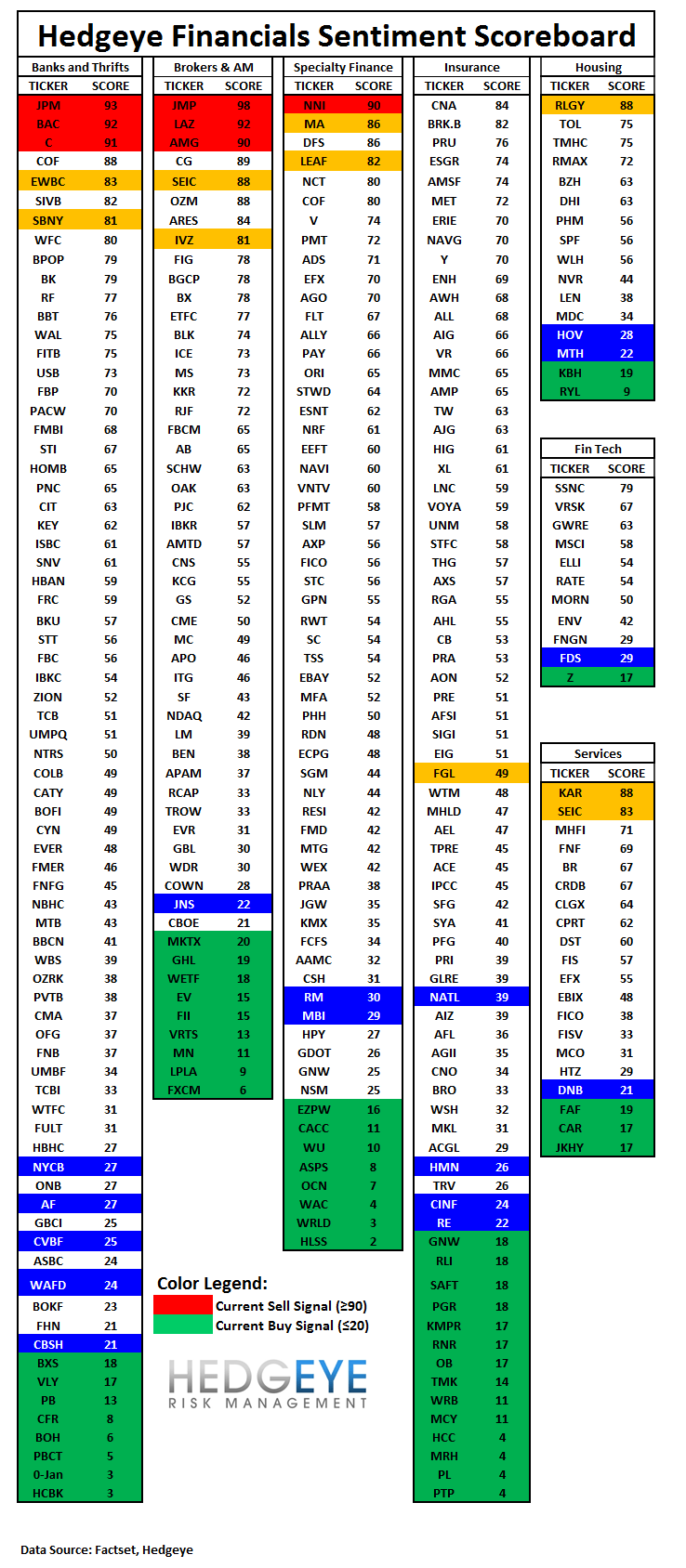

This morning we are publishing our updated Hedgeye Financials Sentiment Scoreboard in conjunction with the release of the latest short interest data last night. Our Scoreboard now evaluates over 300 companies across the Financials complex.

The Scoreboard combines buyside and sell-side sentiment measures. It standardizes those measures to an index of 0-100, where 100 is the best possible sentiment ranking and 0 is the worst. Our analysis shows that a contrarian strategy can be employed successfully by taking the other side of stocks with extreme readings in sentiment, either bullish or bearish. Once sentiment reaches these extreme levels, it becomes a very asymmetric setup wherein expectations become too high or too low.

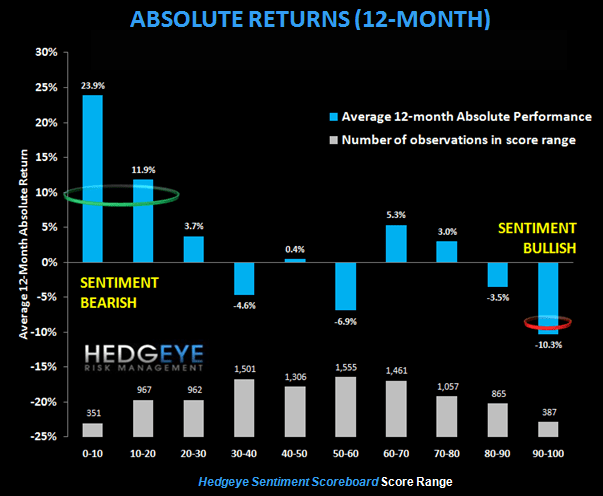

We’ve quantified the tipping points for high and low sentiment. Specifically, we've found that scores of 20 or lower have a positive, average expected return while scores of 90 or greater are more likely to underperform.

Specifically, our backtest of 10,400 observations over a 10-year period found that stocks with scores of 0-10 went on to produce an average absolute return of +23.9% over the following 12-month period. Scores of 10-20 produced an average absolute return of +11.9%. At the other end of the spectrum, stocks with sentiment scores of 90-100 produced average negative absolute returns of -10.3% over the following 12-months.

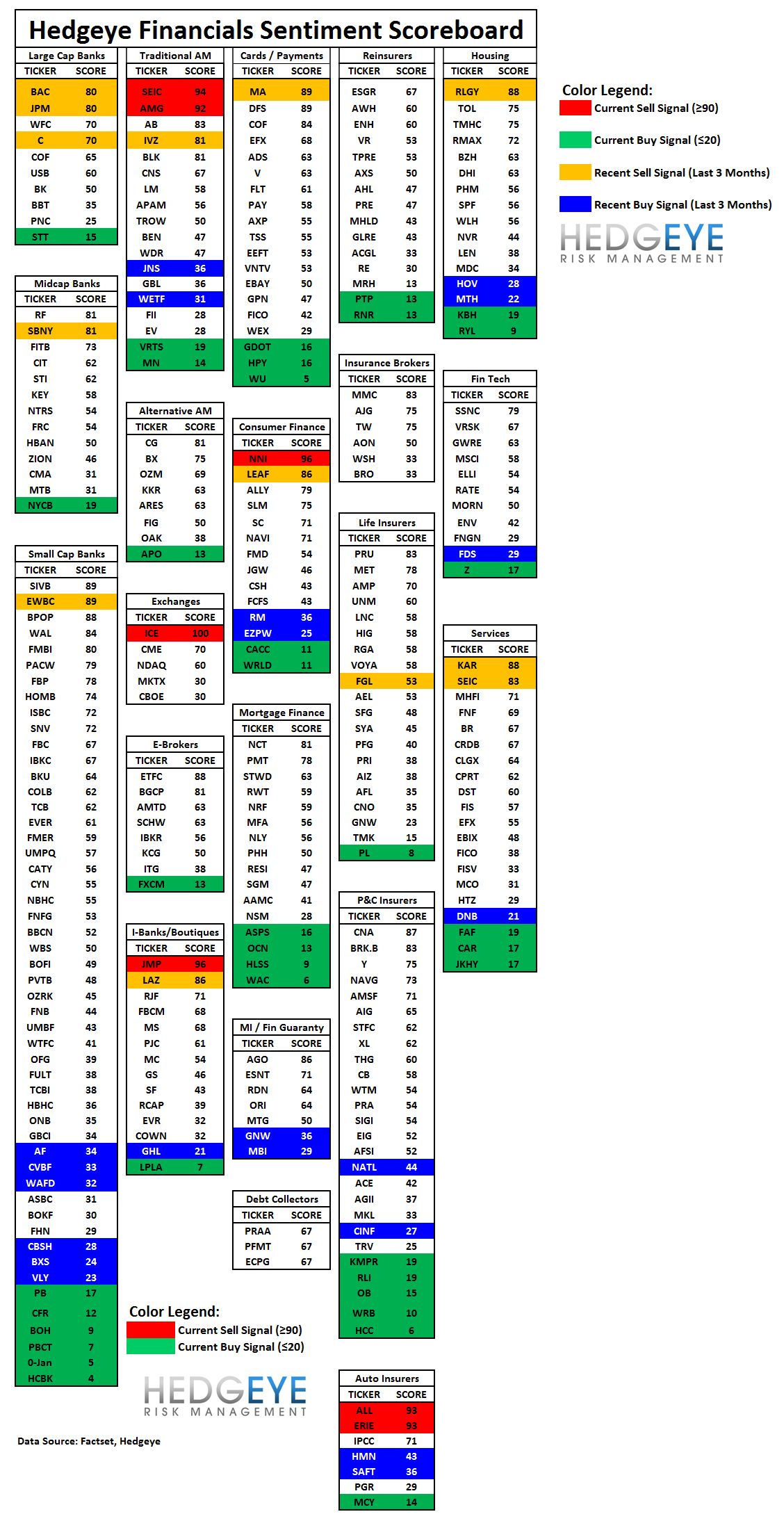

The first table below breaks the 300 companies into a few major categories and ranks all the components on a relative basis. The second table breaks the group into smaller subsectors and again gives them relative rankings within those subsectors.

The following is an excerpt from our 90 page black book entitled “Betting Against the Herd: Generating Alpha From Sentiment Extremes Across Financials.”

Let us know if you would like to receive a copy of our black book, which explains this system and its applications.

BUYS / LONGS: Financials with extremely low sentiment readings of 20 and below on our index (0-100) show strong average outperformance in absolute and relative terms across 3, 6 and 12 month subsequent durations. Stocks with sentiment ratings of 20 or lower rise an average of +15.1% over the next 12 months in absolute terms.

SELLS / SHORTS: Financials with extremely high sentiment readings of 90 and above on our proprietary sentiment index (0-100) demonstrate a marked tendency to underperform in absolute and relative terms across 3, 6 and 12 month subsequent durations. Stocks with sentiment ratings of 90 or greater fall in value an average of -10.3% over the next 12 months in absolute terms.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT