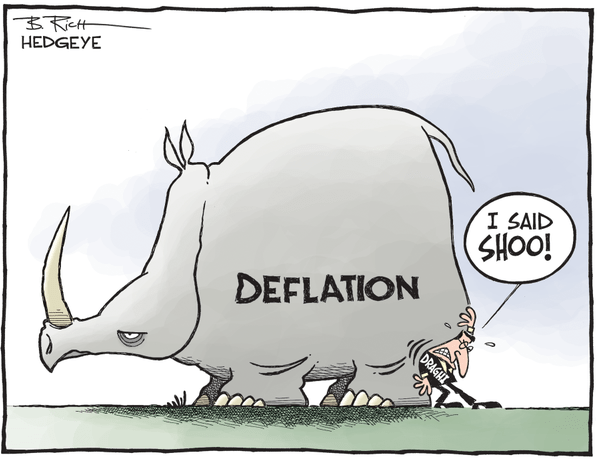

WORRIED ABOUT #DEFLATION? YOU SHOULD BE.

Earlier this morning, ECB President Mario "Whatever It Takes" Draghi warned as much in a speech delivered in Frankfurt. To be precise, Draghi said "We will do what we must to raise inflation as quickly as possible." He then added that "Low core inflation is not something we can be relaxed about."

What may not be appreciated, however, is that Draghi is actually perpetuating deflation, in currencies and commodities.

Here's Hedgeye CEO Keith McCullough's dissection of Draghi's comments, and the resulting effects on USD and oil, in a note to subscribers following the news:

"Draghi saying the ECB “cannot be relaxed” about fighting #Deflation – so, he’s devaluing the Euro again this morning, -0.5% to $1.06 vs. USD, reversing what was a Dollar Down day yesterday (in other words, he’s perpetuating commodity #deflation)

Oil, meanwhile, is looking to snap $40 WTI again as the Dollar ramps on “whatever it takes” to try to bend/smooth economic gravity - you can expect that most OCT “reflation” data is going to mean revert to bearish TREND here in NOV as commodities crash."