"Everybody talks about the weather, but nobody does anything about it."

-Mark Twain

I have been chirping about the #ACATaper for several months now with a small but growing audience of subscribers who are starting to ask more questions about our research as the evidence mounts and stock prices in the healthcare space get hammered.

I say chirping because a chirp is hard to hear, and to a lesser extent, the person chirping is usually beating you. If you have played sports, you know what I mean. If you have an older brother who beat you at whiffle ball absolutely every single time you played and called it “The Streak,” I understand your pain completely.

It is no fun to be chirped, and it’s not my style. Good research is usually quiet, and “getting loud” is anathema to a process, at least a good one, that generates more questions than answers. So far we’ve shared our research most comprehensively in our recent Healthcare Themes Presentation (ping for more info) if you care to take a look.

Back to the Macro Grind…

The #ACATaper theme suggests that after the U.S. Medical Economy experienced the largest inflow of new medical consumers (35 million) in the last 30 years, and who carried with them above normal per capita spending resulting in more than $120B of new money being pumped into the system in a mere 18 months, the what-comes-after will likely be equally epic on the downside.

To put the ACA enrollment expansion into context, the next best year for increases in the number of insured medical consumers occurred in 1996 when the United States added 3.2M people to the insured population. The United States just added 10 times that number in just 18 months! Nothing in recent history even comes close.

What will happen next, in our view, is the enrollment gains of 2014-2015 are now convincingly behind us, and heading for declines in 2016. Those 35 million new medical consumers, who had been chronically uninsured prior to the ACA and had a lot of things to take care of medically, will be spending much less per person in 2016 and beyond. What the ACA has created is a comparison so big that it will likely be violent as it unwinds and might make “taper” look like too gentle a term in retrospect. The #ACATaper may mutate into #REFORMAGGEDON.

If we’re right, we’re not just leaving it up to management teams for the heads up when they speak at a conference or report earnings, like HCA did when they preannounced negative for 3Q15 (down -31%) , or like UNH did yesterday when they also pre-announced negative(down -12%). In HCA’s case, they overstaffed their hospitals for volume that didn’t show up. That agrees with the #ACATaper, which anticipates pent-up demand to roll off in the coming quarters and the ACA consumption contribution to turn negative.

UNH said the same thing but on a lag and in reverse. They announced that their ACA Exchange enrollment was going to cost +$425M more than expected for their 540,000 exchange enrollees. That is $773 per enrollee more than expected, with the true expense likely higher since presumably these losses came after the ameliorating forces of risk adjustment, reinsurance, and risk corridors which the ACA put into place to smooth this new market’s emergence. These two stalwarts of the S&P 500 did not see this coming.

The #ACATaper appears to be happening fast as well. Just compare what UNH said on their 3Q15 earnings call on October 15, 2015 to what they said yesterday on November 18, 2015 when they pre-announced and guided down.

“We will expand to 11 new markets in 2016 and we continue to expect exchanges to develop and mature over time into a strong, viable growth market for us. -David Scott Wichmann President & Chief Financial Officer, UNH 3Q15 Earnings Call

Compare that rosy picture to what UNH communicated in their press release yesterday…

“UnitedHealthcare has pulled back on its marketing efforts for individual exchange products in 2016. The Company is evaluating the viability of the insurance exchange product segment and will determine during the first half of 2016 to what extent it can continue to serve the public exchange markets in 2017” (UNH 2015 earnings update)

We have our high frequency data sets that will keep us alert to the #ACATaper trend. We prefer predictive, high frequency data check-ups with a few anecdotes mixed in, as oppose to waiting for management to tell us what happened.

The Great Healthcare Deflation

After the #ACATaper, the prospects for the US Medical Economy do not appear any brighter in 2017 or 2018, at least not for the vast majority of publicly traded market capitalization available to investors today. Consider the following demographic trends:

- The U.S. workforce and their commercial insurance, the most profitable part of the US Medical Economy, will enter a long period of population growth stagnation, remaining at 190M for the next decade.

- The workforce will get younger too on average, and consume less per capita, as the bolus of Millennials displace the Gen-X generation.

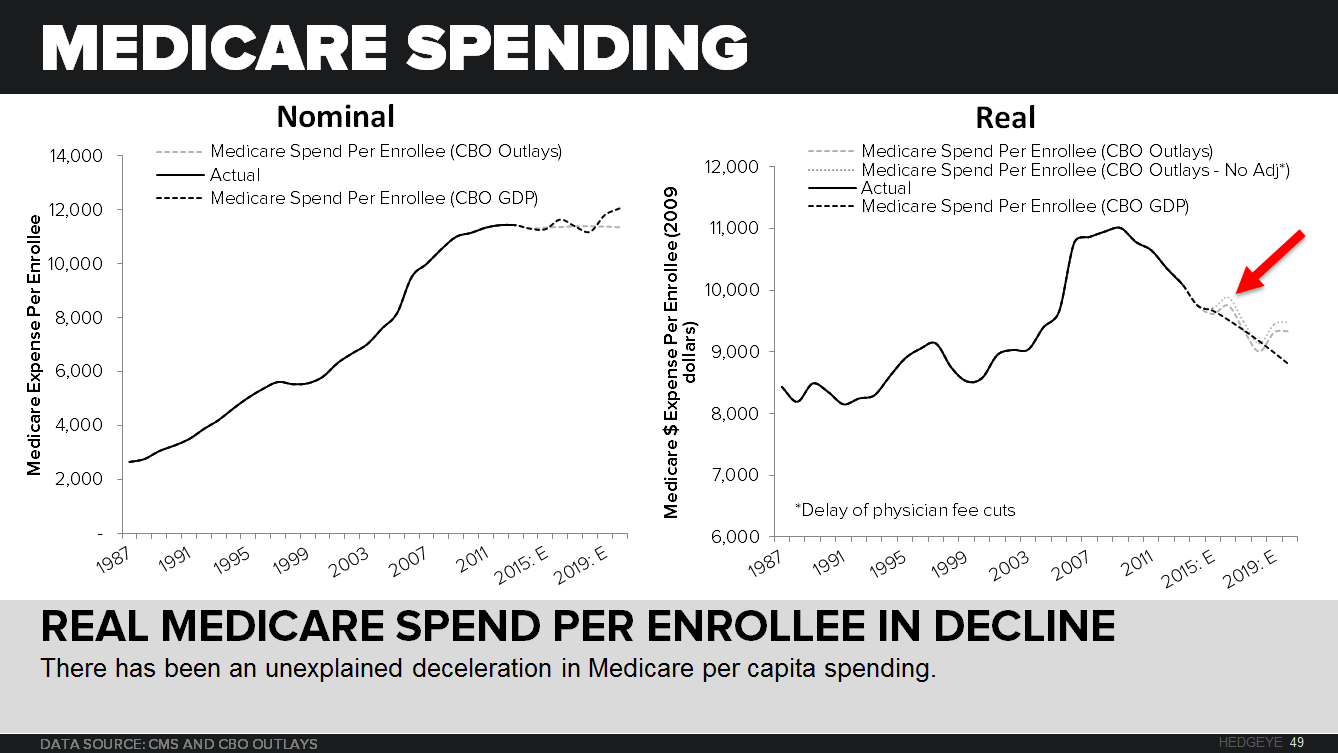

- Meanwhile, the Baby Boomers will graduate into Medicare at a faster rate than Medicare spending is forecast to grow, and push growth of real spending per Medicare beneficiary negative.

These demographic trends will occur with affordability nearing its natural limits. Premiums are nearing the peak for individual out of pocket expense, employer premium contribution, and state and federal budgets for Medicaid and Medicare.

But people will get sick in the future and the population will consume more medical care; they will show up to the doctor office, pharmacy, and hospital regardless of the fiscal backdrop. However, when they do make that appointment, the price paid and profit available for those units of care will almost certainly be lower than today, resulting in a secular decline.

The great hope I have for the U.S. Medical Economy is that I will see a massive turnover in the healthcare market capitalization now included in the S&P 500 Index, and witness the emergence of new delivery models, new products, new technology, that makes the system more price transparent and more efficient. The problem for now is much of this innovation is sequestered out of sight in the world of private investment and venture capital, or yet to be developed at all.

We’ve had 50 years of excess inflation in healthcare, a trend so long in the making that it seems like it can never end, but it will end because there simply isn’t another alternative. There was a time when a knee implant with $70 of material costs could be sold for $7000, but those days are over.

Of course, the transition will be painful, and has only just begun, but it does hold the promise of renewal. My hope is if the policy and capital stewards of the U.S. Medical Economy can manage it, we will have deflating prices, less waste, better care, and the perpetual Healthcare Crisis we’ve come to expect will turn into the Healthcare Opportunity.

If it happens, it will be a great source of strength for individuals and their medical security, their employers who will have more to reinvest, and for our country if we can stick the landing.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.17-2.29%

SPX 2038-2104

RUT 1135--1195

VIX 14.72-20.51

USD 98.49-100.18

Copper 2.05-2.20

If you have any questions please call or send us e-mail.

Thomas Tobin

Managing Director

@HedgeyeHC