“The economic mechanisms of an efficiently inefficient market are fundamentally different from those of neo-classical economics.”

-Lasse Heje Pedersen

That’s a mouthful, but it makes a lot more sense than the bill of linear-economics goods I was sold in college. I’m looking forward to debating real-world market practitioners at our inaugural Global Macro conference tomorrow in Stamford, CT – it’s called Macrocosm.

The principles of neo-classical economics are fun to consider, mainly because they’re so easy to disprove. Pedersen’s book, Efficiently Inefficient, is a great primer on the fundamental differences between econ PhD dogmas and real world markets.

Does capital structure matter? How about funding frictions and liquidity constraints? When do you need to be aware of phase transitions in economic, profit, and credit cycles? These are all questions we non-linear people will be considering at Macrocosm.

Back to the Global Macro Grind…

Darius Dale and I were doing the rounds, seeing sharp Institutional Investors in Boston yesterday, when what was looking like another flat to down day for US stocks turned into some rip roaring fun to the upside.

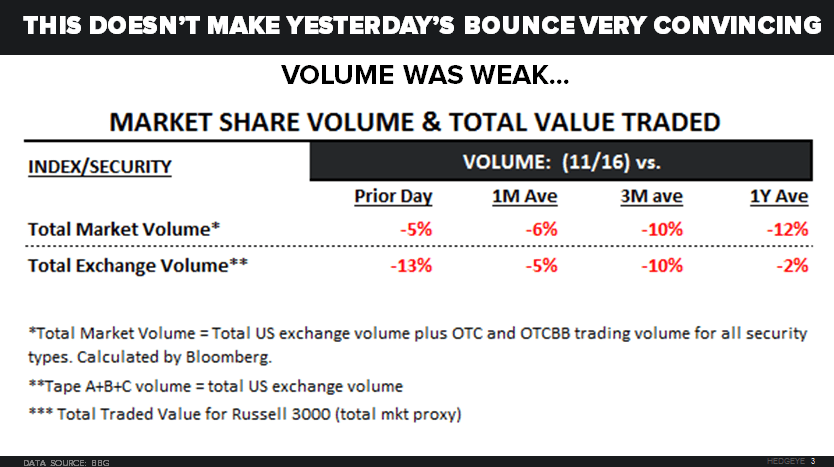

It’s a good thing they bounced them. That was the 1st real up day (albeit on slowing volume – see Chart of The Day for details on Total US Equity Market Volume being -12% vs. its 1yr average) for the US stock market in the last 9.

With the SP500 +1.5% on the day, the real pin-action (beta chasing) was in that good ole “reflation” trade:

- Oil (WTI) popped +3.1% on the day after collapsing another -7.9% last week

- Energy Stocks (XLE) proceeded to ramp +3.3% > 2x the SPY move in turn

- Utilities (XLU), the only major S&P Sector to close up last week, closed +1.7% too

What was it that drove this ramp? Was it NY Fed Head Bill Dudley turning tail saying the Fed doesn’t really have to raise rates in DEC due to “well below target inflation.”

Click here to join Hedgeye CEO Keith McCullough live on The Macro Show at 9am.

Was it a bird or a plane? Was it simply that US and European Equity markets signaled immediate-term TRADE oversold into Friday’s close? Or some combination of all of the above?

I’m pretty sure it wasn’t another set of US Retailers (XRT) missing numbers yesterday (Dillard’s (DDS) down -15% on the Friday/Monday “low gas prices” combo – and Urban Outfitters (URBN) seeing US demand being so bad that they’re buying a pizza chain).

No, I couldn’t make up that pizza-pivot if I tried. That stock is going to keep crashing today.

Copper is still crashing this morning too, down another -0.4% to $2.10, taking its YTD and 6-month #Deflations to -26% and -28%, respectively. But we really shouldn’t talk about that when we can be debating how Qe4 is going to drive the next bull market in Energy.

Seriously, that’s on the table.

That was the main contention in our client debates yesterday – the line of questioning went something like this:

- “So, let’s just say you’re right and the probability is rising of a US recession by mid-2016…

- And let’s assume that the Fed isn’t dumb enough to keep raising into a slow-down…

- Wouldn’t you guys being right on the economy mean the Fed needs to start easing again?”

Yep. Why not?

Oh, right. There’s that thing called the US Presidential election where:

- If the US is dropping below 1.5% GDP growth (towards 0.4% - Hedgeye’s low-end scenario for Q4 to be reported in Q1)

- The probability rises that a Republican could win…

- And if that Republican contender is anti-Federal Reserve, how does Janet (a Democrat) go to Qe4 during the debates?

Well. Since she’s un-elected, I hope everyone realizes that she can have the “courage to act” however she damn well pleases. That said, this whole central-planning catalyst calendar is going to get really gnarly if she tries going there.

Remember that if/when the Fed pivots back to dovish from pretend-hawkish, they have to tell the American People why they are doing that. Say it with me now – Super #LateCycle Growth Slowing…

In other news, neo-classical linear economists still have +3-4% US GDP growth forecasts for 2016.

Our immediate-term Global Macro Risk Ranges are now (with intermediate-term TREND research views in brackets):

UST 10yr Yield 2.17-2.36% (bearish)

SPX 2020-2073 (bearish)

RUT 1139--1167 (bearish)

NASDAQ 4 (bullish)

Nikkei 181 (bullish)

DAX 101 (neutral)

VIX 16.59-20.25 (bullish)

USD 97.99-100.08 (bullish)

EUR/USD 1.05-1.07 (bearish)

YEN 121.53-123.99 (bearish)

Oil (WTI) 39.79-43.55 (bearish)

Nat Gas 2.23-2.40 (bearish)

Gold 1070-1101 (bearish)

Copper 2.08-2.20 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer