STILL DON'T BELIEVE GROWTH IS SLOWING? WE DON'T KNOW WHAT TO SAY.

While the latest round of lackluster economic data continues to confound Old Wall expectations, we're not surprised. Our Macro team continues to reiterate its #GrowthSlowing and #SuperLateCycle calls even while many on Wall Street cherry-pick last month's "Where's Waldo" jobs report number as the latest "evidence" to remain ebullient.

Oh well. The data continues to be on our side.

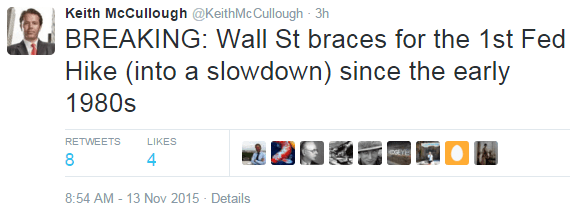

Look no further than today's retail sales and producer price numbers. Hedgeye CEO Keith McCullough had this to say:

"Both US Retail Sales and PPI slowed (again) this month. If you missed the Macy’s and Nordstrom blowups this week, just wait until US Retailers comp the toughest comp in 5 yrs (in November). Oh, and the Fed is going to hike into this slowdown. That should be fantastic for the [producer prices] which is crashing to new lows like Copper did this week. USD #Deflation Risk = On."

Today's PPI reading confirmed our concerns about #Deflation (one of our calls for over a year now). Here's a five year look at PPI including the latest number. To be sure, the slope of the line is unambiguously negative:

We nailed retail sales too. This past July, Hedgeye Macro analyst Darius Dale warned subscribers about #ConsumerSlowing...

Again, here are the latest numbers and the increasingly tough comps for retail sales in November.

And this beauty...

Need more proof? Anecdotal evidence of the consumer spending crash is sprinkled all over equity markets.

Here's Macy's (M) CEO Terry Lundgren earlier this week:

"We believe that the retail industry is going through a tough period that we seem to experience something like this every five to seven years or so, and this one feels familiar in that regard."

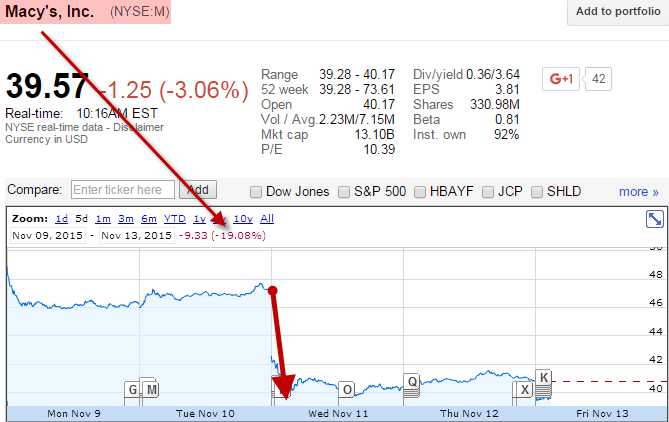

... And a look at Macy's stock chart:

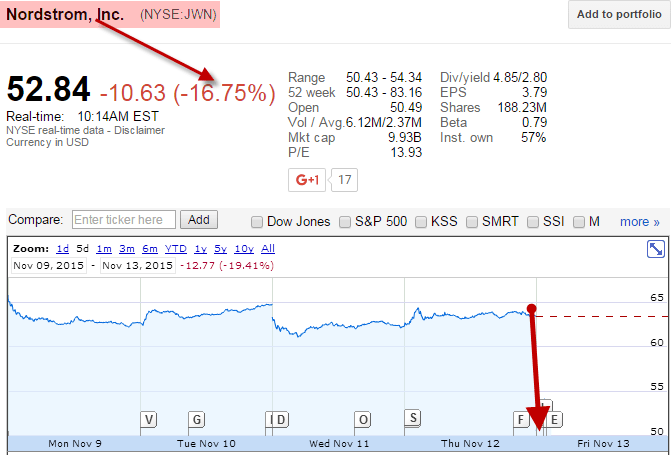

Then there's Nordstrom (JWN) CFO Mike Koppel:

“It appears that there has been a slowdown in the overall demand for the customer that is purchasing what we sell.”

... And the resulting stock plunge:

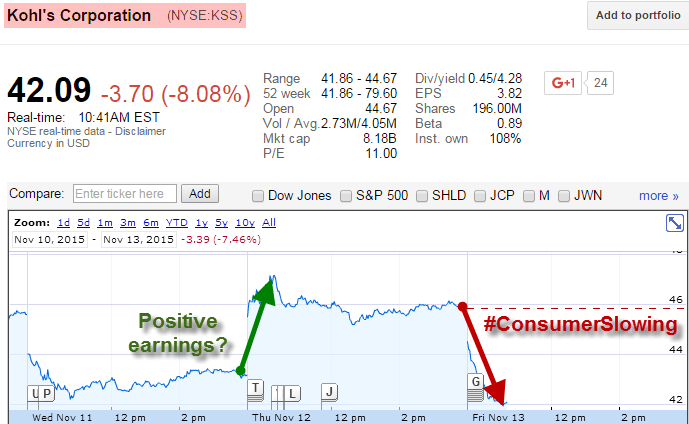

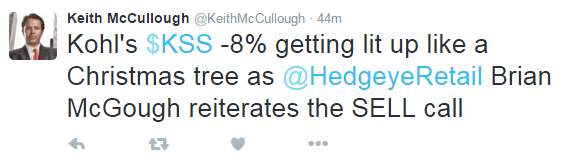

Not to alarm you further... but even after Kohl's (KSS) posted seemingly positive earnings, its shares are getting shellacked too on #ConsumerSlowing woes. (Note: our Retail analyst Brian McGough reiterated his short call yesterday.)

Bottom Line: None of this is reassuring. Economic Pollyannas be advised.