Editor's Note: Below is a chart and brief excerpt from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to subscribe.

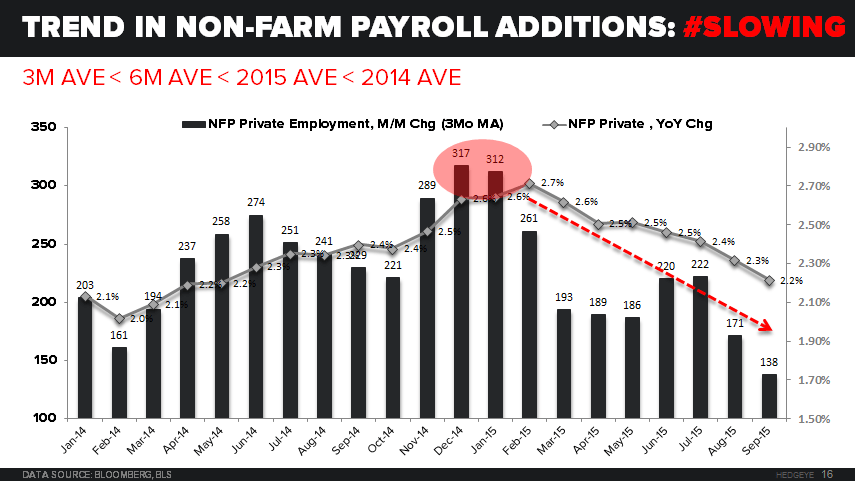

"... While the probability of another #GrowthSlowing Non-Farm Payroll (NFP) print remains as high as it’s been since we started making the call that the US Labor Cycle peaked in Q1 of this year (see Chart of the Day with the DEC 2015 NFP top circled in red), what if the perma bulls paint it as “good”? This is where the fiction of “good” can become very bad for macro markets."