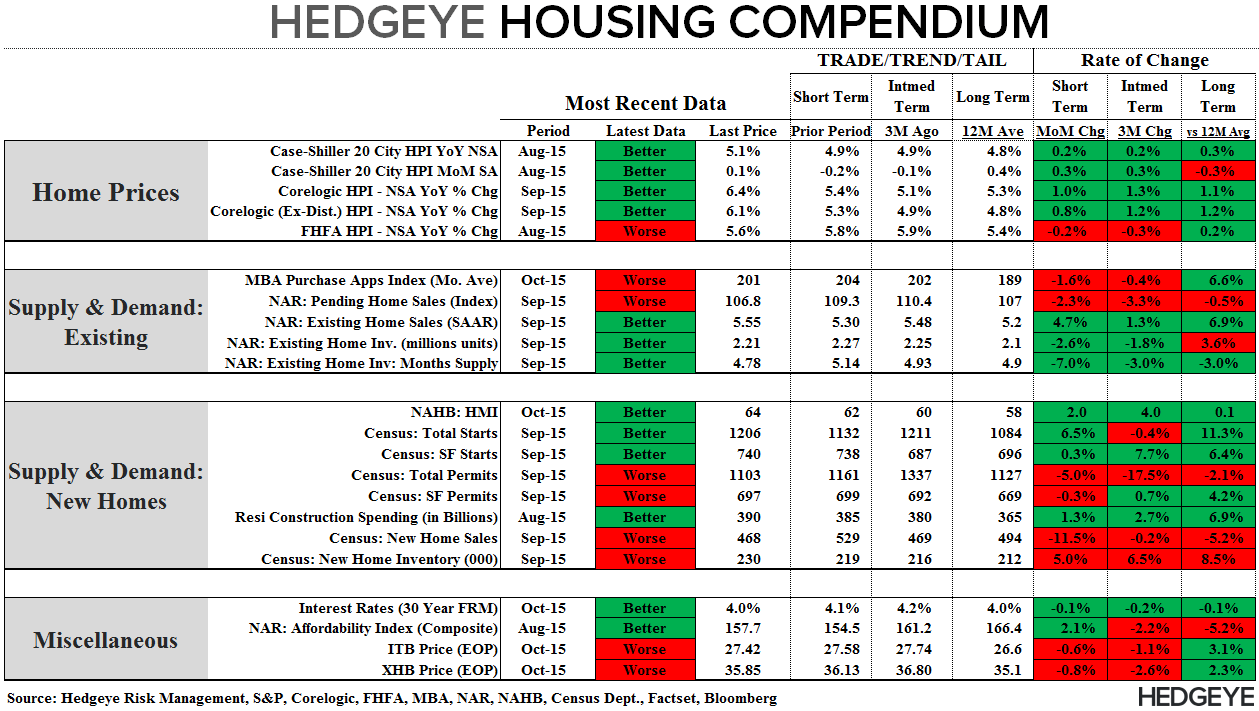

Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

Today's Focus: MBA Mortgage Applications

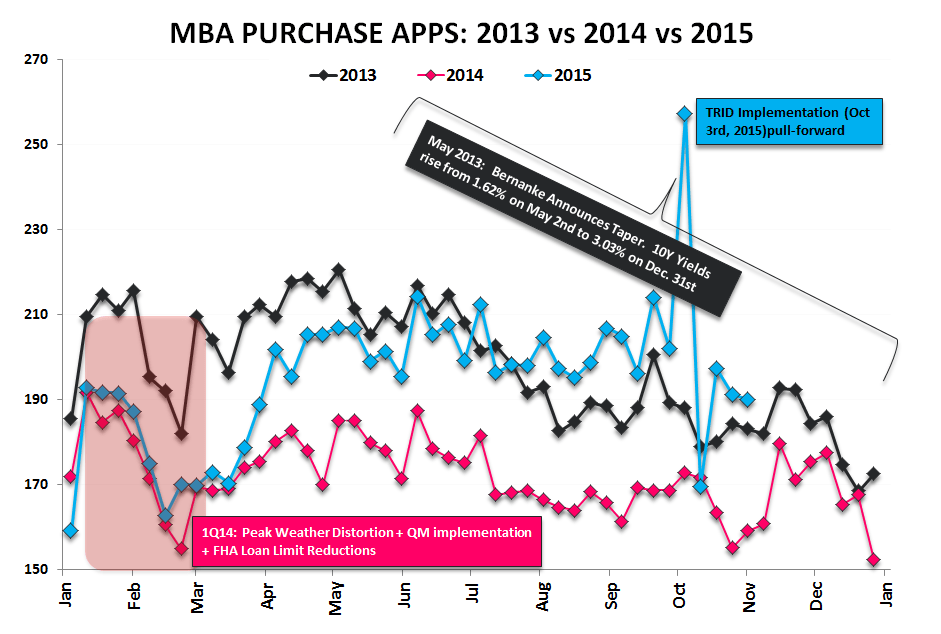

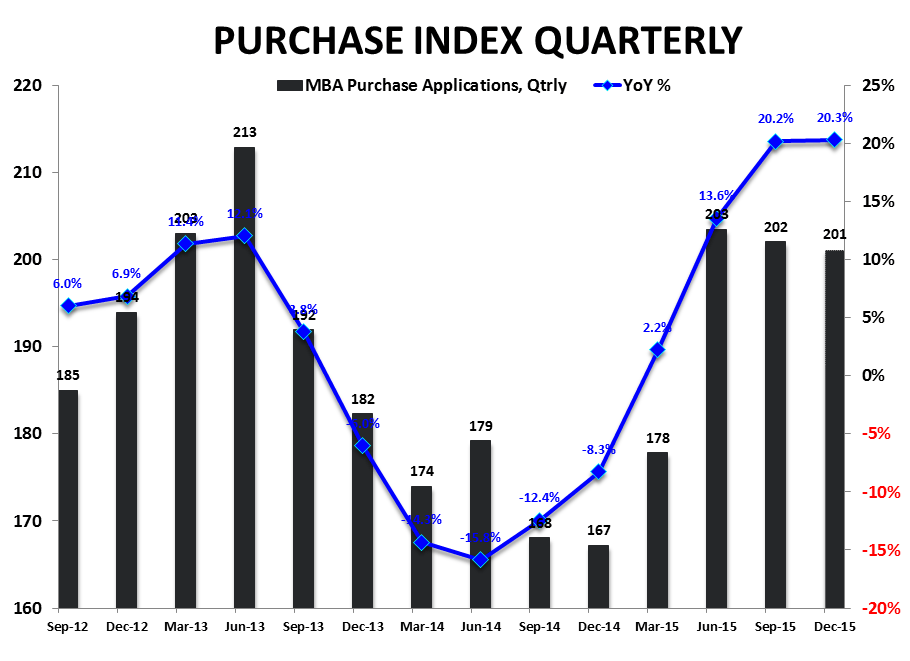

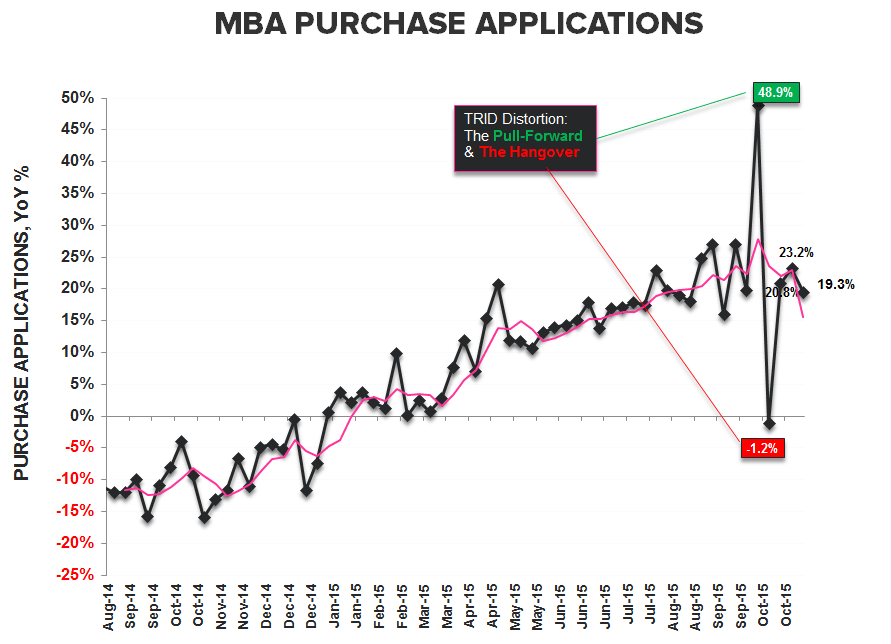

Purchase Demand declined -0.6% week-over-week while decelerating -300 bps to +19.3% year-over-year.

The latest weekly data is largely uneventful but, on the margin, the last three weeks of October have seen a modest pullback in activity relative to both September and recent quarter averages. Excluding the weeks immediately prior to and post TRID implementation, purchase demand in October is tracking -5.6% and -4.5% relative to August and the 3Q15 average (see 1st chart below). Given the progressively easier back half comps, growth has remained solid and steady on a year-over-year basis at ~+20% YoY.

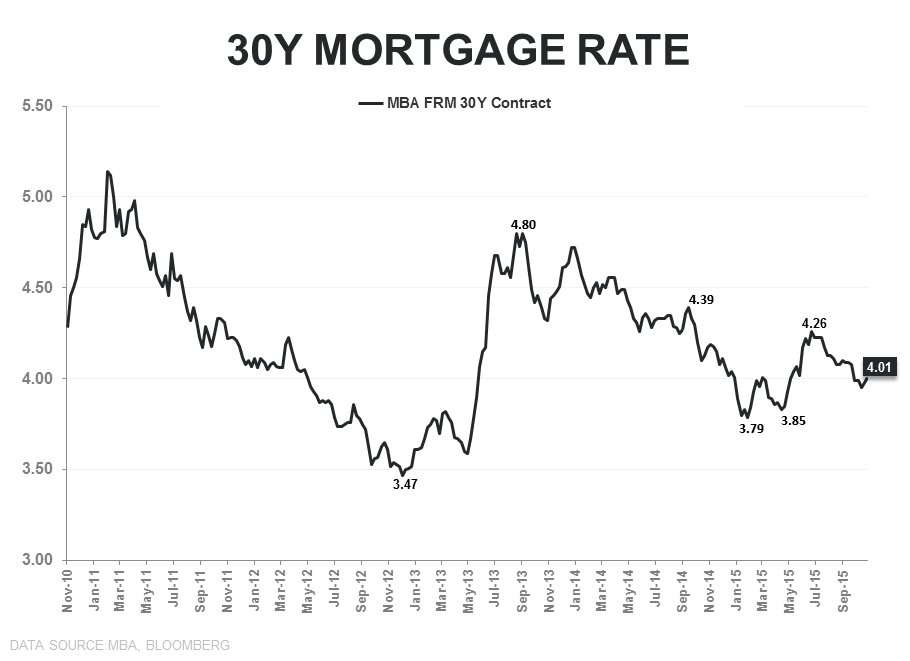

Meanwhile, rates on the 30Y FRM contract moved back above 4%, rising +3bps in the latest week as the bond market bid both the short and long end higher in response to the rhetorically hawkish commentary out of the FOMC October meeting. At current levels, rates are in-line with the 2015 average of 4.02% and below the 4.35% average for 2014.

About MBA Mortgage Applications:

The Mortgage Bankers’ Association’s mortgage applications index covers more than 75% of mortgage applications originated through retail and consumer direct channels. It does not include loans delivered through wholesale broker and correspondent channels. The MBA mortgage purchase applications index is considered a leading indicator of single-family home sales and construction. Moreover, it is the only housing index that is released on a weekly basis.

Frequency:

The MBA Purchase Apps index is released every Wednesday morning at 7 am EST.

Joshua Steiner, CFA

Christian B. Drake