“The legend lives on from the Chippewa on down

Of the big lake they call Gitche Gumee

The lake, it is said, never gives up her dead

When the skies of November turn gloomy”

-Gordon Lightfoot

While I hope none of you are ever subject to listening to me sing, “The Wreck of the Edmund Fitzgerald” by Gordon Lightfoot is a tune I’ll often hum, especially when I’m getting bearish.

It’s a local (and mortal) hymn for those of us who grew up on the big lake they call Gitche Gumme (Lake Superior). The skies of US economic data haven’t turned this gloomy since early 2007. So I’m really humming this morning.

And, as a friendly reminder to those of you who didn’t know, I also got fired for being “too bearish” on November 2nd, 2007. By the end of that month, the almighty SP500 was down over 6%, on the way to an almost 60% peak-to-trough crash.

Back to the Global Macro Grind…

I’m not making the 2008 call we made. I’m reiterating the 2015 one we’ve been making. While time flies and Wall Street’s memory about cycles slowing are short, they always seem to miss that each cycle slow-down isn’t the last one they missed.

Never ever forget that it’s cycles (not central market planners) that make the world go-round. They are natural. They base (2009), recover (2010), stall (2011-12), accelerate (2013-14). They peak (2015). They get long in the tooth (Late Cycle 1H 2015). Then they slow (2H 2015).

That’s probably why the Atlanta Fed’s “GDP Now” cut its GDP forecast from 2.5% to 1.9% last night. Yesterday morning’s ISM reading for the US was a 50.1 for OCT. In rate of change terms, that’s -7.8% year-over-year (the slowest of the year) as we head into the gales of November.

But, but… the “jobs number could be good”, right?

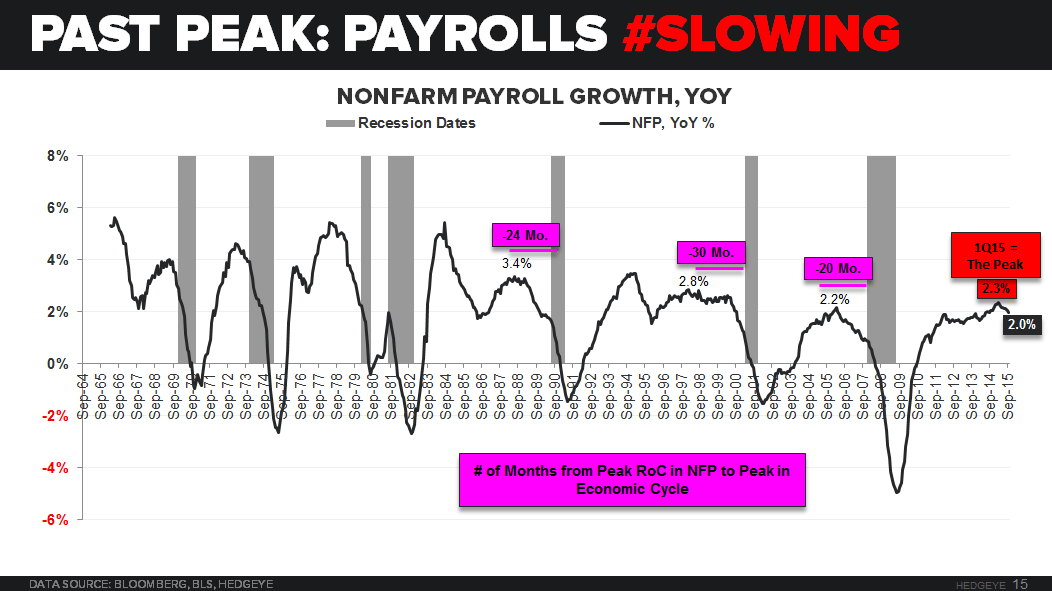

Right. Right. While the “mid-cycle” theory has been dead wrong, I’ve been hearing about wages and jobs “accelerating” for 6 months… but, as you can see in today’s Chart of The Day, we’re heading right into the eye of the storm (toughest compares) of this slowing US Labor Cycle.

“So”, if the non-farm payroll number is 194,000 or 206,000, the Fed should “hike” into a slow-down, right?

Wrong.

Forget for a second what happens on Friday if the more probable scenario at this stage of the cycle plays out (that we get another slowing labor report), if the Federal Reserve raises rates into this gale I think they could easily be the catalyst for the next US stock market wreck.

“The ship was the pride of the American side

Coming back from some mill in Wisconsin

As the big freighters go, it was bigger than most

With a crew and good captain well seasoned

Concluding some terms with a couple of steel firms

When they left fully loaded for Cleveland

Then later that night when the ship's bell rang

Could it be the north wind they'd been feelin'?”

Yes, I get it. US investors have great pride in the American side. But the wreck of expectations happens when everything you’ve been feelin’ since the US economic data really started to slow in July hasn’t gone away.

With both the Europeans (ECB) and Chinese “easing” at the end of October, there’s been plenty of monetary tightening on those positions levered to both A) inflation expectations (Commodities, Levered Energy Companies, Russia, etc.) and B) US Dollar denominated debt.

Raising rates “just because it feels like it’s time” into a slowdown could easily rip the US Dollar Index through 100.0. And if you’re mathematically aware of how that “flows” through to SP500 Earnings, you’ll note that’ll sink 1H 2016 revenues/earnings, big time.

On that score, as of last night’s close, 360 of 500 companies in the SP500 have reported the following:

- Revenues down -5.1%

- Earnings down -4.2%

It took me about 3 seconds to review what 2015 US stock market bull predicted that:

- GDP growth would get cut in half in 2015

- And Earnings would be down 4-5%

That’s because none of them did.

So have some patience with the bear case (like we did in July). Wall Street knows a #LateCycle slowdown morphing into a recession when it sees it. Give it time. And, in the meantime, I’ll keep humming:

The wind in the wires made a tattle-tale sound

When the wave broke over the railing

And every man knew, as the captain did too

Twas the witch of November come stealin’

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.98-2.21%

SPX 2025-2117

RUT 1135--1189

VIX 13.54-19.30

USD 95.99-98.41

EUR/USD 1.08-1.11

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer