C&I and CRE Results Turn Negative

The Fed released its 4Q15 Senior Loan Officer Survey yesterday afternoon. The survey was conducted between September 29 and October 13 and covers lending standards and loan demand across business and consumer loan categories.

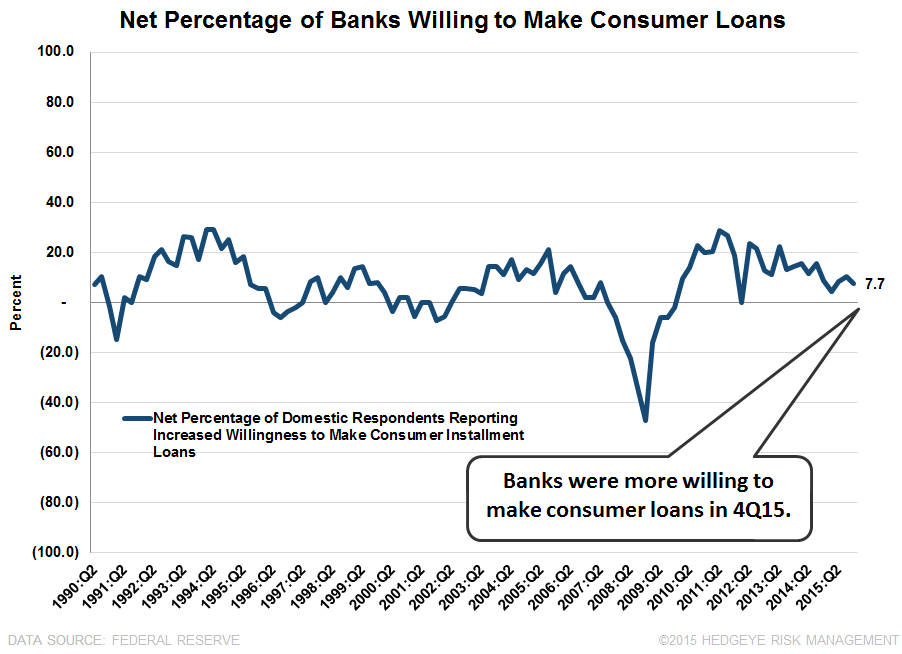

The survey results turned negative for both C&I and CRE lending. Residential mortgage lending standards were mixed. Consumer lending showed the most positive results; a net positive percentage of banks continued to report easing consumer lending standards, and demand for those loans increased.

Here are the two main takeaways this quarter:

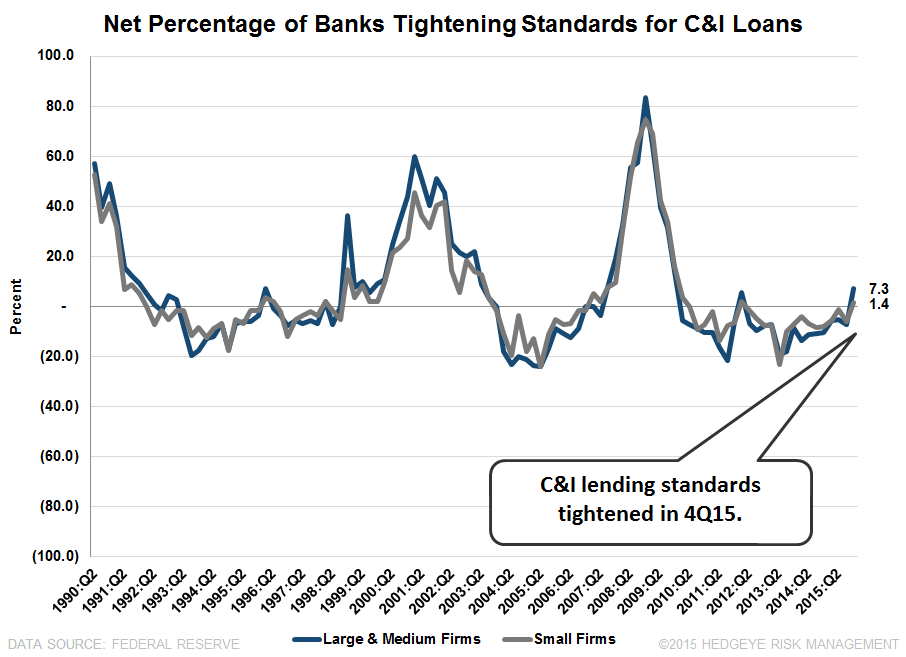

1. The net % of banks tightening C&I lending standards turned positive in 4Q15. Just to be clear, this is a bad thing. 7.3% of banks, net, tightened C&I credit standards for large and medium firms in 4Q15. This is only the second time since the last recession that a net positive percentage of banks tightened standards; the last time banks tightened was 1Q12, when 5.4% tightened C&I standards for large and medium sized firms. Moreover, 1.4% of banks, net, tightened C&I credit standards for small firms in 4Q15. As the chart below shows, tighening standards have preceeded and arguably been a proximate cause of the last two recessions. That being said, there have also been a few false positives, such as 1Q12, 1Q96 and it's debatable whether the surge in tightening that accompanied the late-1990s Asian Financial Crisis and LTCM was in fact a false positive or not.

At a minimum, the takeaway is fairly clear: lending standards tend to autocorrelate across the cycle and when they roll from net easing to net tightening it's something investors must take note of.

While somewhat obvious, it's nevertheless worth stating that this could be the inflection point signaling that Financial equity prices are at or near their peak. Unlike the prior positive tick in 1Q12, this time the economic cycle is showing many signs of being late stage.

The chart below looks at the historical C&I lending standards (LHS) juxtaposed against the S&P 500 Financials Index (RHS). C&I lending standards have historically begun tightening coincident with or ahead of peaks in Financial equity prices. We've highlighted in green the periods during which Financials stocks have risen. In the 1990s it was clear that lending standards were tightening by late 1999, suggesting the roll was near. In the 2003-2007 period standards began to tighten in 2007.

2. CRE Tightening. Commercial real estate lending also saw standards tighten in the quarter. The tightening was across all three categories: C&D, Nonfarm Nonresidential and Multifamily. Unfortunately, the survey format changed with the 4Q13 survey when they replaced the single category of CRE loans with the three aforementioned subcategories. As such, it's not possible to compare apples to apples historically. That said, in the 9 quarters since the new format began, this marks only the second (and second consecutive) quarter in which standards have tightened on C&D loans. It marks the first quarter in which Nonfarm Nonresidential loans have seen standards tighten. The Multifamly category has been bouncing between easing and tightening over the last two years so we take this quarter's net tightening with a grain of salt.

A Quick Review of the Senior Loan Officer Survey by Category:

C&I: The Canary In the Coal Mine

Two quarters ago, we called out C&I as a potential canary in the coal mine. That's because the net percentage of lenders tightening standards was almost back to the zero line. That percentage then eased back in 3Q15. However, 4Q15 appears to be the confirmation; the net percentage of banks tightening standards for loans to large firms moved past zero to +7.3%. Additionally, +1.4% of banks tightened standards for C&I loans to small firms. This could mark the end of the 6-year bull market for Financials equities.

CRE: Tightening Across the Board

After C&D lending saw a moderate 1.4% of lenders tightening standards in 3Q15, banks are now tightening standards for all three CRE categories in 4Q15. This inflection in CRE standards adds to our concern over the inflection in C&I standards.

Meanwhile, demand for all three categories of CRE loans increased in the fourth quarter.

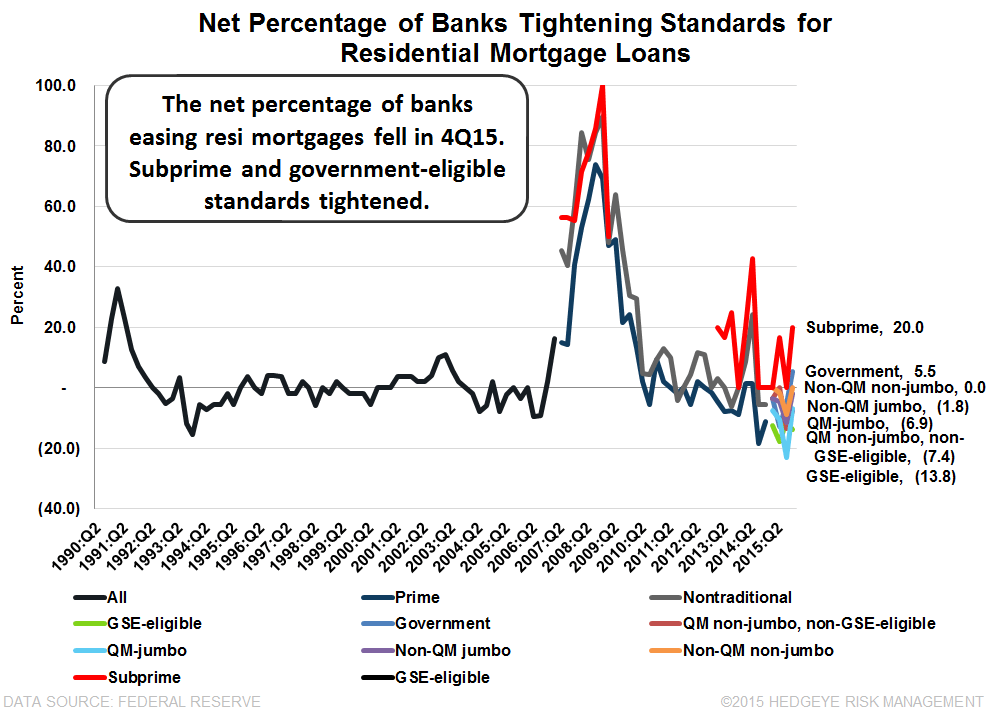

Residential Mortgage: Mixed

Starting in 1Q15, the Federal Reserve broke the survey's residential Prime and Nontraditional categories into six new categories and kept the Subprime category for a total of seven different categories. The six new categories include: (GSE-Eligible, Government, QM non-jumbo/non-GSE eligible, QM jumbo, Non-QM jumbo, and Non-QM/non-jumbo). The categories we're most interested in are the GSE-Eligible (Fannie/Freddie) and Government categories (FHA/VA) since these two categories account for ~90% of all origination volume. The GSE-Eligible category showed 13.8% of banks, net, eased standards Q/Q in 4Q15. However, Government showed a 5.5% net tightening. 20% of banks also tightened standards for Subprime loans. Three of the other four categories eased while one was unchanged.

We pay little attention to the demand component of the Fed's Survey because it reflects shifting refi demand and isn't a good barometer for purchase activity. Nevertheless, we include both charts below.

Consumer Loans: Easing

Standards for credit cards, auto loans, and consumer loans ex-cards and autos all eased in the third quarter.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT