RECENT NOTES

10/30/15 SBUX | WHAT WILL SLOW THEM DOWN? | CONFERENCE CALL NOTES

10/30/15 RUTH | #BEEFDEFLATION

10/29/15 EAT | TIME FOR A RESET

10/29/15 BURRITO TRACKER | CMG, QDOBA (JACK)

10/29/15 BWLD | BWLD TRACKERS | CONFERENCE CALL NOTES

10/28/15 PNRA | NO “CHOPPY” OCTOBER HERE

10/26/15 BLMN | HOW BAD IS BAD? | ASK THE STEAK TRACKER

10/23/15 DNKN | THE DONUT TRACKER

10/22/15 MCD | THE ROAD TO $150

SECTOR PERFORMANCE

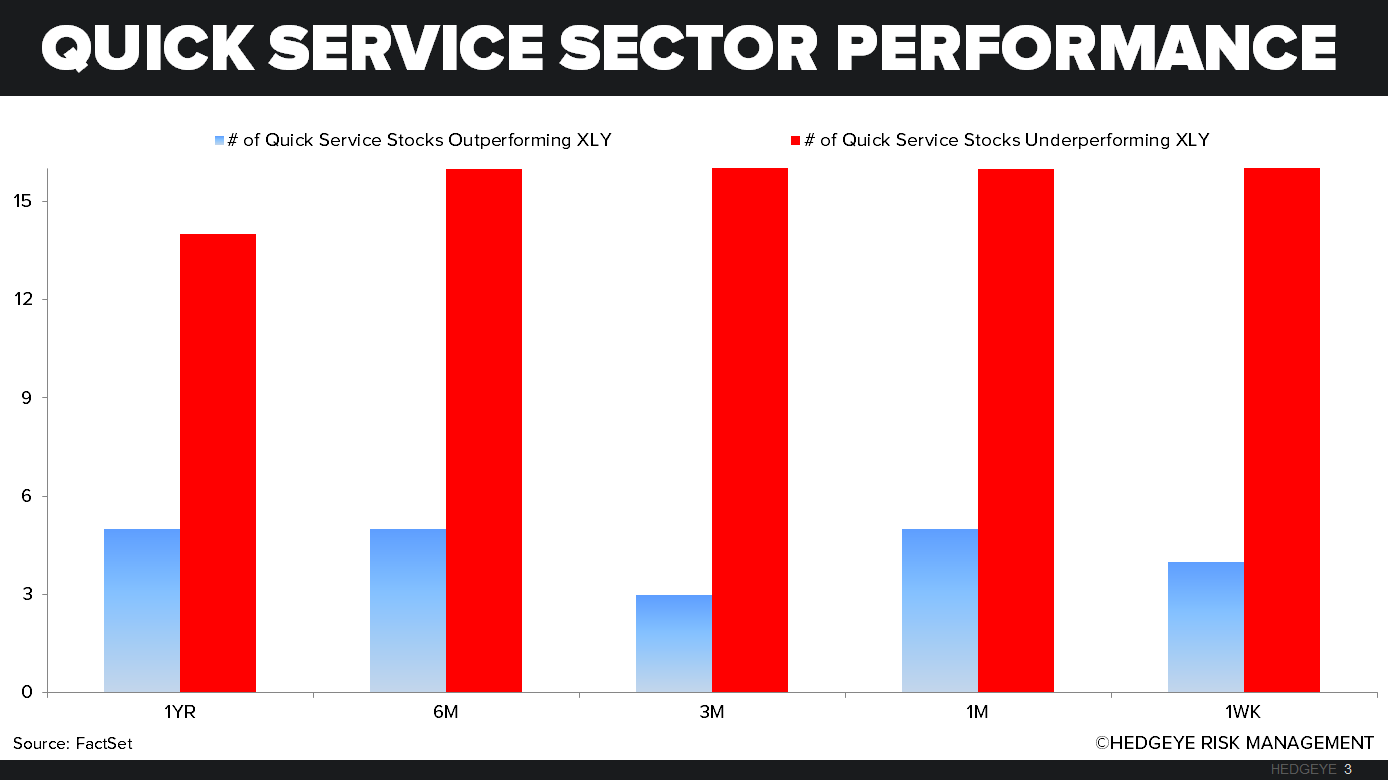

Casual Dining and Quick Service stocks that we follow widely underperformed the XLY last week. The XLY was up +1.7%, top performers on a relative basis from casual dining were BOBE and BBRG posting a decrease of -1.4% and -1.6%, respectively, while NDLS and WEN led the quick service group this week up +5.8% and +1.8%, respectively.

XLY VERSUS THE MARKET

QUANTITATIVE SETUP

From a quantitative perspective, the XLY looks BULLISH from a TRADE and TREND perspective, TREND support is 76.98.

CASUAL DINING RESTAURANTS

QUICK SERVICE RESTAURANTS

Keith’s Three Morning Bullets

341 of 500 S&P companies have reported – sales are -5.5% and earnings -3.9% and USD #Deflation Risk hasn’t gone away:

- ASIA – post their month-end markups for OCT, Japan and China dropped -2.1% and -1.7%, respectively, overnight – on any metric (never mind a cluster of metrics) we follow, that side of the world hasn’t stopped slowing in GDP terms

- RUSSELL – but “stocks are up” if you back out the 2000 stocks in the Russell which dropped another -0.4% last week to -3.6% YTD (in the Russell 3000, 62% of stocks are still -20-25% from their #bubble peaks) – reminds me of OCT 2007

- JOBS – I keep hearing that the jobs report this week could “surprise to the upside” but haven’t had 1 email that suggests it could be another slowing one… weird. Since FEB all the rate of change in the US jobs market has done is slow from its peak

SPX immediate-term risk range = 2015-2096; UST 10yr Yield 1.99-2.19%

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst