In a recent note to subscribers, Hedgeye CEO Keith McCullough reiterated our #SlowerForLonger (growth) theme and explained how investors should play slowing economic growth:

"If we’re still right on #LateCycle GDP Slowing, easiest move is to short the Financials (XLF, KRE, JPM) and buy Utilities and Treasuries (XLU, TLT, etc.) – this is the 8th or 9th time in 2015 they’ve “rallied” the 2yr to 0.75% and failed."

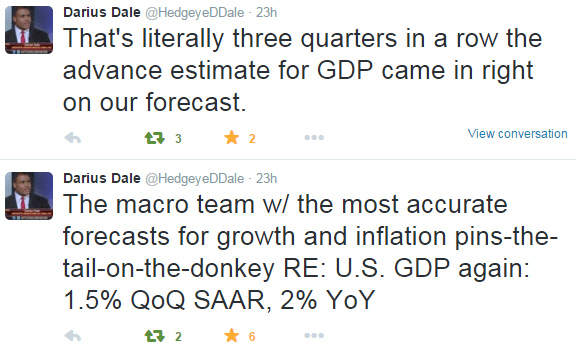

Incidentally, our macro analysts Christian Drake and Darius Dale sent a detailed note to institutional subscribers Thursday afternoon providing additional context on why we believe things are going to get worse on the economic front and providing an update on how to be positioned.

Here's the headline and takeaway:

Here's how that setup worked out in 3Q:

LONGS: Utilities (up +4.4%) and Treasury Bonds (10Y Yield down -32bps):

SHORTS: S&P 500 (down -6.9%), Financials (down -7.2%) and High Yield Credit (Yields up +148bps and OAS up +154bps, on average)

(If you'd like access to our macro team's non-consensus research please email sales@hedgeye.com)