Takeaway: The split is on track for February, but now with better leadership and significant identified restructuring opportunities. We think that MTW is one of the most undervalued and least understood names in the sector.

Overview

We think that the departure of Glenn Tellock is a positive for MTW and that Hubertus Muehlhaeuser seems a very promising segment leader. The restructuring opportunities in the 3Q release suggest a substantial opportunity to improve operations, which is not that surprising given a lack of prior operational attention. The 3Q preannouncement was somewhat misleading, in our view, since it provided little context on weaker Crane results that we now know were driven heavily by delayed VPC shipments. The planned split was defended robustly on the call, including the point that an investment grade credit rating for either segment is not needed. In all, we continue to think the split will unlock substantial value and that MTW is one of the most undervalued and misunderstood companies in the sector.

Highlights

Preannouncement Head Fake: MTW’s preannounced a GAAP number, which we thought inappropriate given the separation costs. Today, we learned that MTW had $10.4 million in costs associated with restructuring and separation, as well as a “ballpark” $15 million hit from delayed shipments of newly introduced VPC cranes (now corrected). Backing out those items, MTW generated an estimated operating income of ~$68 million vs. $83 million in the year ago period. While down, it is hardly as catastrophic as headlines suggested. Those items should also have been disclosed in the preannouncement.

Split Defended Strongly: Apparently, no one on the Board cares if Cranes is investment grade, or if it has a fairly small valuation and profitability. We agree that the split is a great value-unlocking opportunity; as we see it, the Crane segment has a ‘negative’ valuation at present. We also think that the Cranes business is less broken than some believe (see below).

Tellock Out Is A Positive: It seems clear that Glenn Tellock was let go by the Board. Hubertus Muehlhaeuser, the new head of the Foodservice business, sounded very strong on the earnings call this morning. That is a significant upgrade from his introduction on the last call, when Tellock didn’t given him much of an introduction. Hubertus’s presentation was detail oriented and he handled the Q&A effectively. As we see it, Tellock did not appreciate activist meddling and never seemed on board with the split.

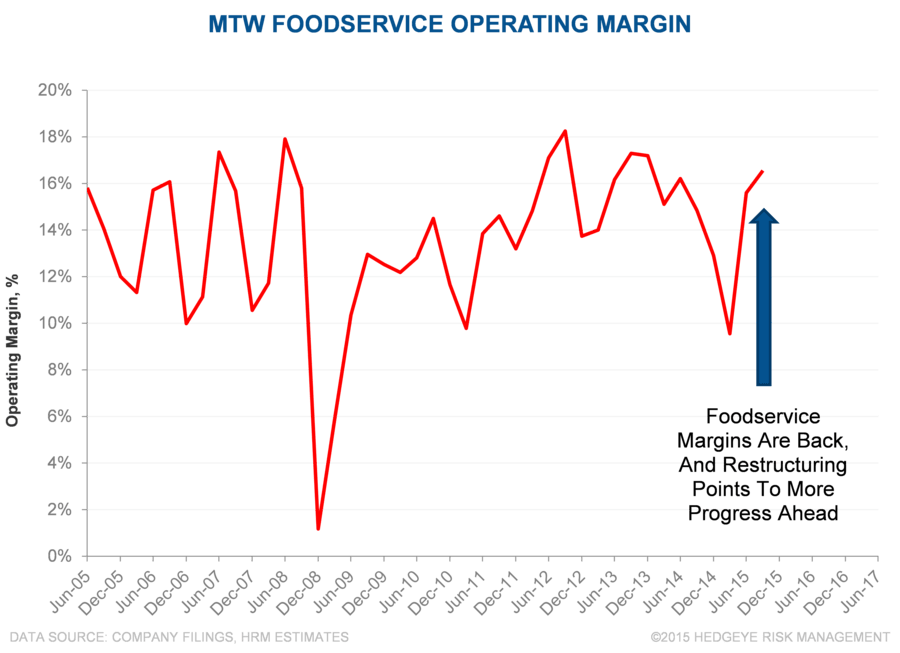

Restructuring Guidance Quite Large: The restructuring announcements suggest a substantial opportunity to improve operations, which is not that surprising given a lackluster prior management team. If you caught all of benefits from the restructuring items, it sounds as though Foodservice should spin with a substantial earnings growth opportunity baked in. Expect new management to market these, and we wouldn’t be surprised if more opportunities pop-up in Cranes as new leadership comes in.

- Foodservice: The nearer-term consolidation of the Cleveland facility is expected to result in $30 million in cost savings next year, and $40 million by 2017. Over the next 3 years, they indicated an extra 150 basis points to the margin in addition to that Cleveland restructuring.

- Cranes: There should also be a benefit from the right-sizing and capacity reductions in the Crane segment of $35 - $45 million over the next three years, with a portion of that expected next year. We should get more detail here as new leadership takes over.

Sentiment Very Negative, Inconsistent: For a company with a solid value-unlock catalyst in just four months, the analyst community certainly hates MTW. The questions from sell side analysts with higher ratings were even nasty in tone. It isn’t clear to us how the price target from the Street could have been literally cut in half over the last year. After all, it is the exact same group of businesses and the sales and margins in the Foodservice segment (the vast majority of the firm’s value) are higher today.

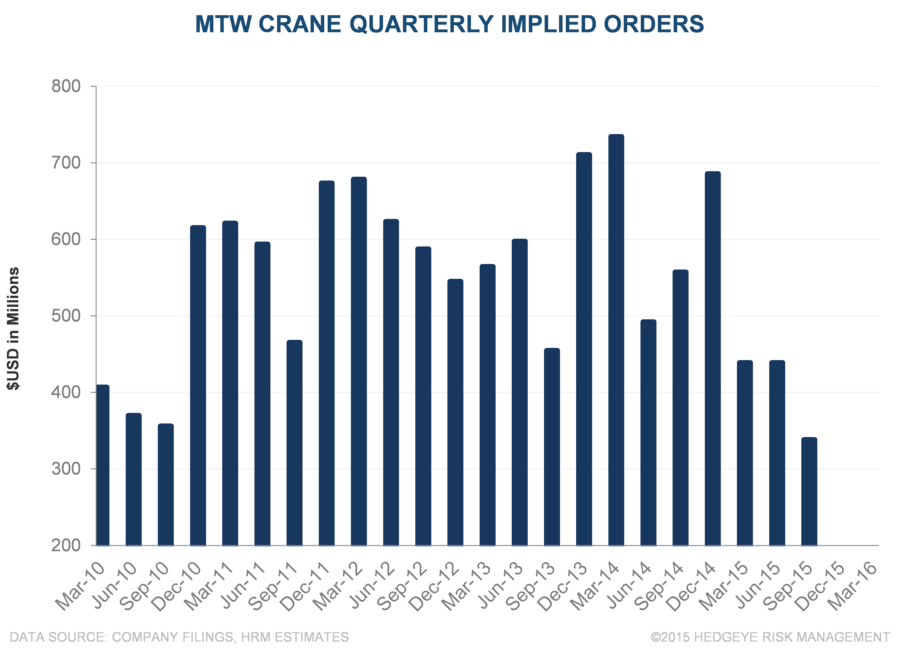

Cranes Not Below Prior Trough If Appropriately Adjusted: If the delay in VPC shipments is backed out, which is appropriate since it is associated with a hitch in a new product introduction, crane margins look much better – certainly above the prior cycle low. Sales in the quarter would have been about $55 - $60 million higher at a “ballpark” 25% incremental margin. Should this have been emphasized in the earnings release? Obviously. As for crane orders, the quarter was pretty weak. That is a negative, but it is hard to say if the VPC issue also delayed orders or how much is related to weaker commodity prices – an impact that should roll off as construction is the key crane end market.

Crane Orders Are Incredibly Noisy Quarter To Quarter: The September quarter is typically the seasonally weakest.

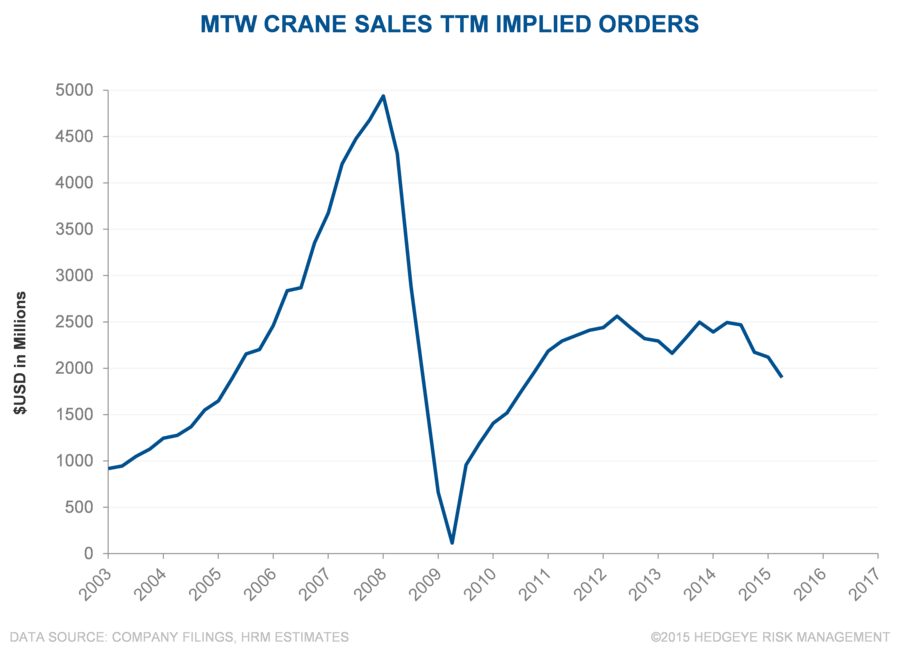

TTM Less Remarkable: The trailing 12 month orders for the MTW crane segment shows a trend unlike the prior downcycle.

Upshot: The split is on track for February, but now with better leadership and significant identified restructuring opportunities. We think that MTW is one of the most undervalued and least understood names in the sector.