Panera Bread (PNRA) is on our Hedgeye Restaurants Best Ideas list as a LONG.

Yesterday after the market close PNRA reported 3Q15 numbers followed up by a conference call this morning at 8:30am ET.

HEDGEYE OPINION

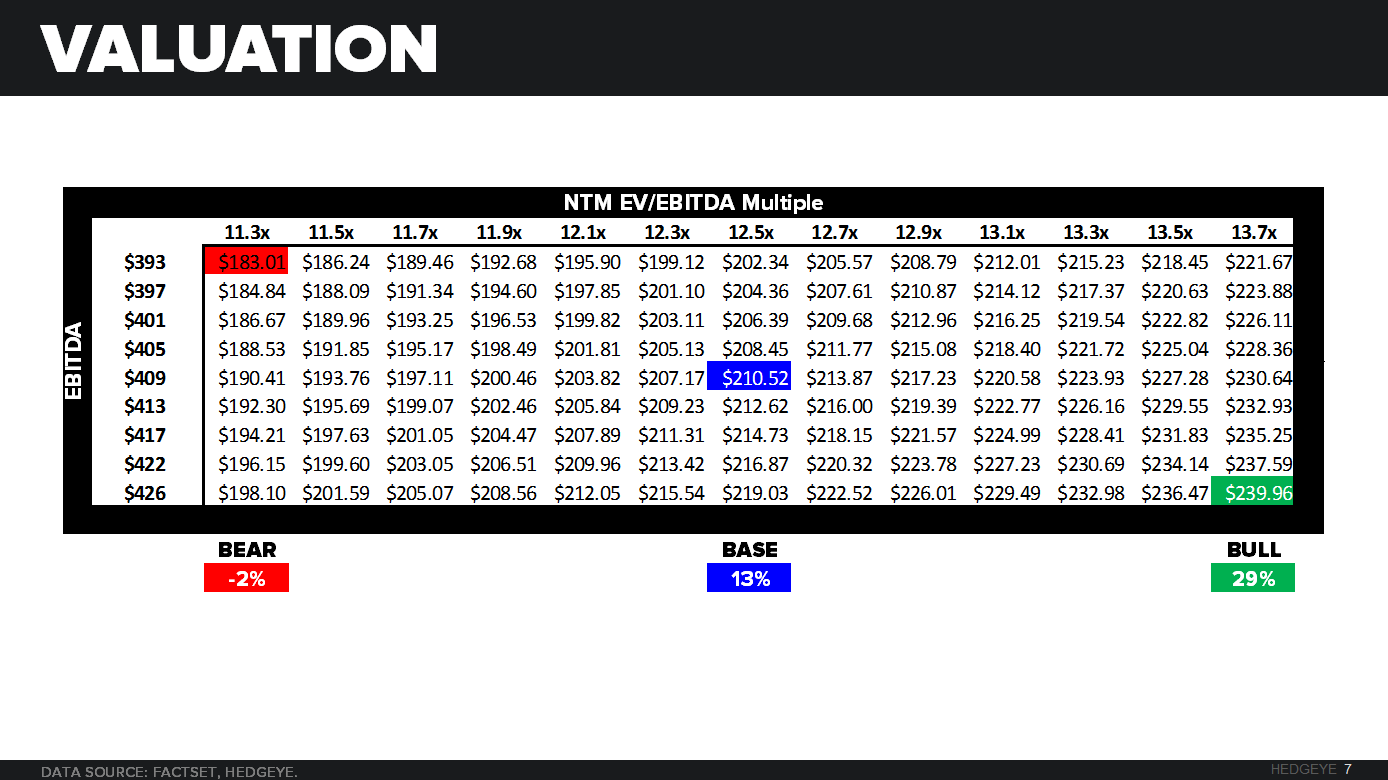

Although PNRA missed on the top-line, in our eyes it was a solid performance overall, especially relative to some other companies that have already reported. PNRA represents one of our top ideas in the restaurant space and as you will see in the valuation section below, we see roughly 30% upside in the name, up to $240 per share.

3Q15 EARNINGS RESULTS

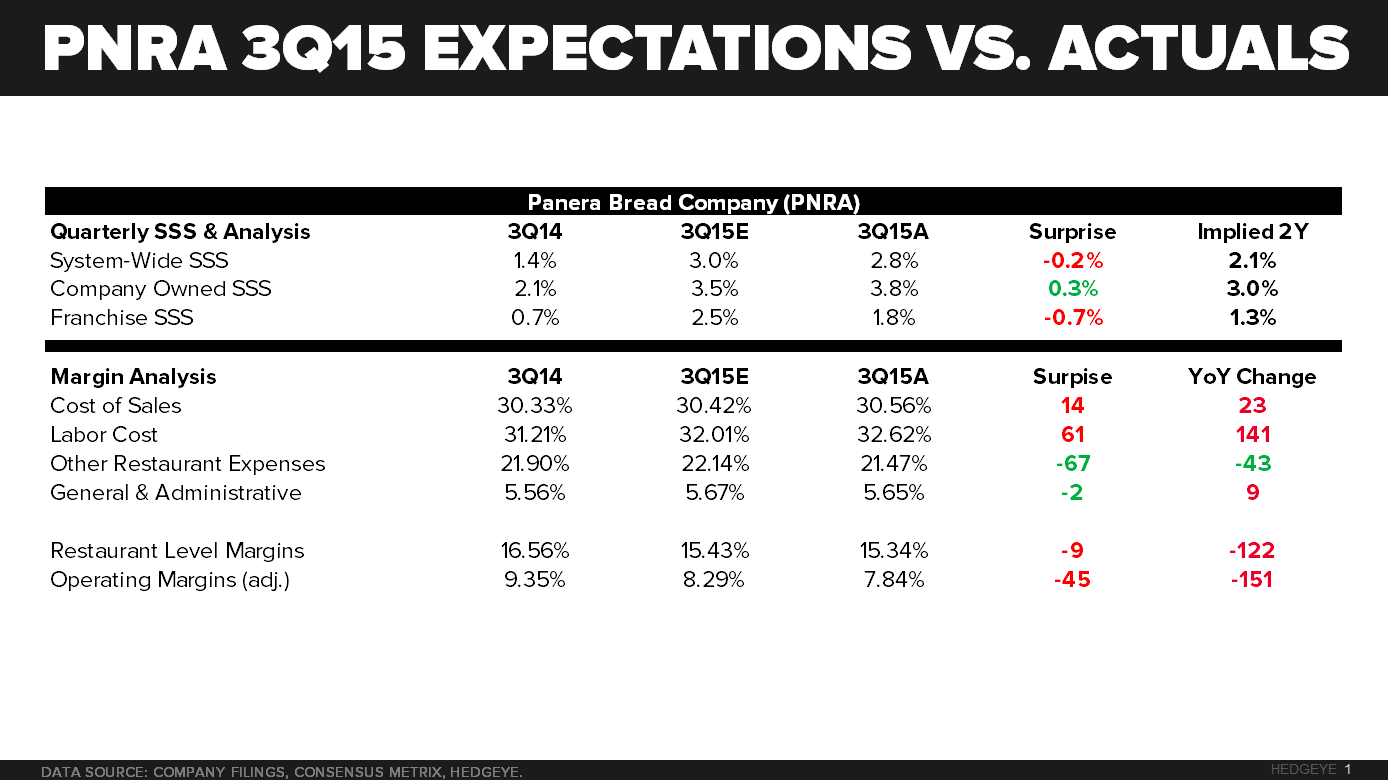

PNRA reported revenue of $664.7mm versus consensus estimates of $667.6mm. Broken out by segment; sales for Bakery-cafés were $584.1mm versus consensus estimates of $585.6mm, Fresh Dough to Franchisees $46.3mm versus consensus estimates of $47.0mm, Royalties and Fees $33.7mm versus consensus estimates of $33.7mm.

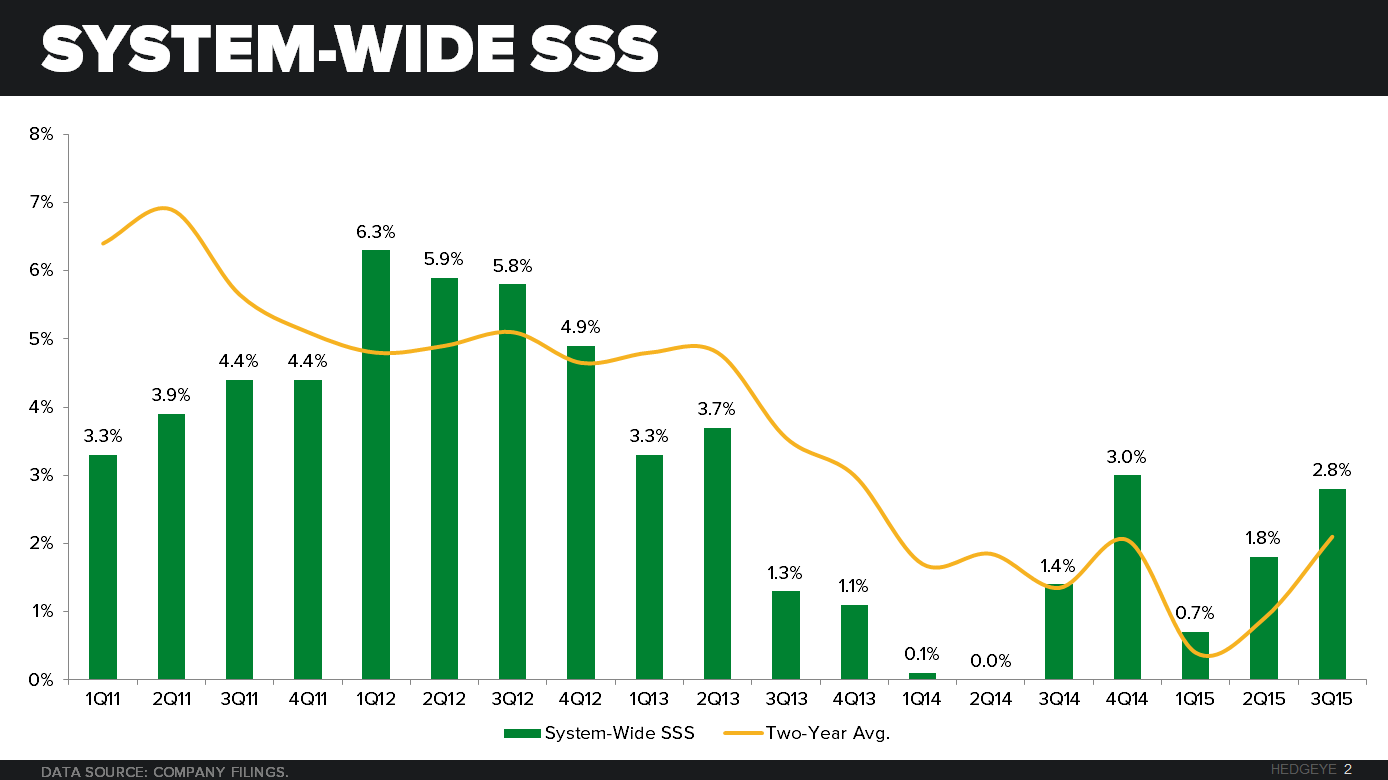

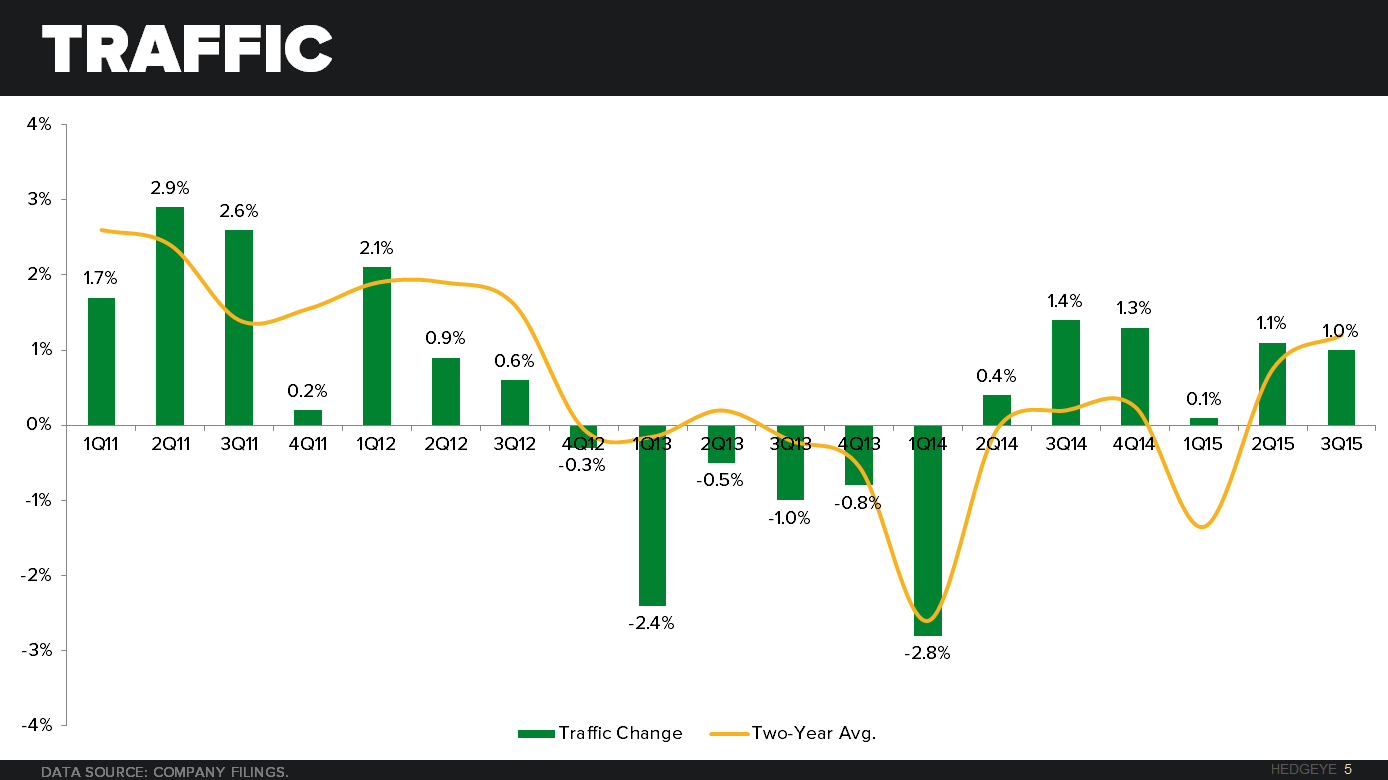

System-wide same-store sales (SSS) were 2.8% versus consensus estimates of 3.0%, Company-owned SSS were 3.8% versus consensus estimates of 3.5% and lastly Franchise SSS came in well short of expectations, at 1.8% versus consensus of 2.5%. Breaking down the company-owned comp, PNRA saw 1.0% traffic growth and 2.8% check growth in the quarter. Transaction growth was up in every day part, pre-11am day part was up 1.7%, while the post-11am day part was up 0.7%. Traffic, although positive and well ahead of the industry average, was still short of consensus expectations, which were calling for a 1.6% traffic number. Notably, the company commented that in the first 27 days of Q4 comps at company owned restaurants were 3.4%

Moving to the bottom-line, PNRA reported EPS of $1.32 ex-items beating street expectations of $1.31 by $0.01.

NOTEWORTHY COMMENTARY

- As of 3Q15, the company had completed the conversion of 291 bakery-cafes to Panera 2.0, with 108 conversions completed during Q3, which is more than one per day

- Catering grew by 12% in the quarter, evidence that the Hub investments are paying huge dividends for the company, management believes this will be a $1bn business over time

- Consumer products is expected to grow to a $175mm business by the end of 2015, has grown at a 60% rate for the last four years

- The widening divergence in the company-owned versus franchisee comp is evidence of the positive impact of initiatives such as Panera 2.0

- Delivery is still in tests, big decisions to be made about whether it should be handled internally or through an outside party

- Structural wage inflation and the affordable care act continue to be pressures, accounting for 110bps of deleverage in this quarter

- Breakfast continues to grow faster than lunch and dinner, salad sales also increasing

- Core G&A declined 4% in the quarter

- 100% of artificial ingredients to be removed by the end of 2016, currently at 90%

MANAGEMENT GUIDANCE

Management reaffirmed full year 2015 guidance, of company-owned comparable SSS growth for FY2015 to be in the range 2.0 to 3.5%. Management is still targeting the conversion of approximately 300 company-owned bakery-cafes to Panera 2.0. Operating margins are still expected to be down 100 to 175 basis points. The company is still targeting 105 to 115 system-wide new bakery-café openings in fiscal 2015. In addition, the company reiterated EPS growth of flat to down mid- to high-single digits for the full year.

VALUATION

We believe that management has the company headed in the right direction and are executing well on key initiatives. With that, and our belief that they will continue to outperform their competition we reiterate our positive outlook for the company and its stock performance. We expect PNRA’s multiple to expand over time as investors and analysts see the viability of Panera 2.0, as it will greatly improve sales potential and profitability over time.

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst