Editor's Note: Click here to learn more about our suite of investing products and how you can subscribe.

Oil was slammed by Draghi’s Devaluation, closing down another -1.8% yesterday (WTI), taking it to -5.2% in the last week alone. It's still very much in crash/deflation mode -47% year-over-year. Witness the carnage in Oil & Gas stocks (XOP) -2.9% yesterday too.

Yeah, #NoWorries. Everything you had to be long for the 1st two weeks of October, like Oil & Gas stocks (XOP), U.S. Transportation (IYT), and Biotech (IBB) has gone straight down in the last 3 trading days post the Draghi Devaluation => USD Up Deflation.

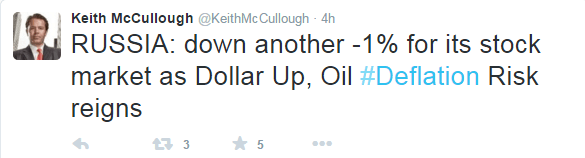

And with oil down, we're watching Russia take a hit too...