In a note to subscribers this morning, Hedgeye CEO Keith McCullough warned investors about the underappreciated risks embedded in emerging market debt.

“Emerging Markets didn’t like the Euro Devaluation last week, the EM MSCI Index closed -0.8% on the week. Reminder: there’s a $9T USD denominated debt #bubble that deflates on these tightening events (see our Q4 Macro Themes deck). Yes, ECB President Mario Draghi ramping USD is deflationary – ask Oil down -6.3% last week, or Energy Stocks (XLE -1.4%).”

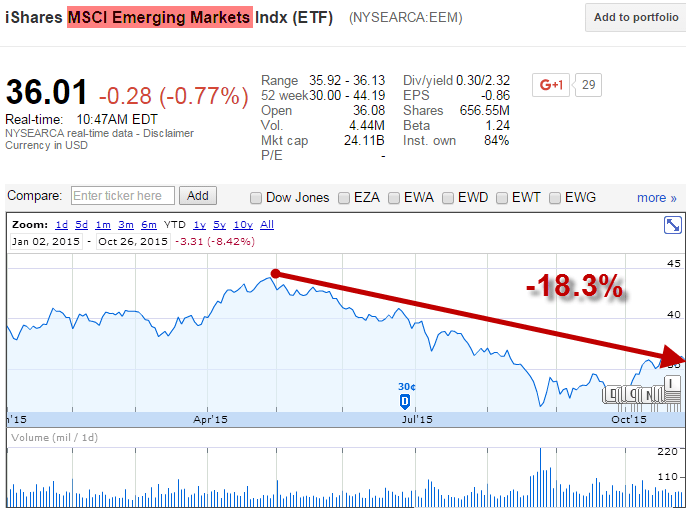

Take a look at this slide from our Q4 Macro deck on emerging market debt .

Click to enlarge the image below:

We see #deflation and the popping of over-inflated asset bubbles everywhere. That's why #Crashing is one of our Q4 Macro themes.

But we'll let you be the judge of the evolving trend playing out in emerging markets...

*If you’d like to learn more about our institutional research offerings or obtain a copy of our Macro Themes deck please ping sales@hedgeye.com.