When a stock trades at 70x an underlying earnings stream that’s only growing 15%-20%, the cold, hard truth is that the ratio of ‘awesomeness-to-mediocrity’ needs to be off the charts in a given quarter to appease the market. For a day, at least. On today’s menu there was a bit too much mediocrity in the mix.

Is there anything we heard that makes us question the long term growth potential of UA? Absolutely not. We think that it ultimately has between $3.50-$4.00 in earnings ($10bn revs at 12% margin). Importantly we think that UA is making the investments required to complete its transition from being a Great US Brand, to a Great Global Company. We actually don’t think it cares nearly as much as other companies in hitting a quarter, and for that we commend Plank & Co. That’s why there are some investors who own this name and will absolutely not sell it. They see a company going from $3.9bn in sales to $10bn, and earnings from just over a buck this year to $4.00 in five years’ time.

But for some investors that don’t have Kevin Plank’s duration, the quarter matters. And unfortunately, when looked at holistically, this was not as stellar a print as one might think in listening to all 5 Analysts who asked questions on the call congratulate management for doing its job.

Revenue was on fire – coming in +29% yy. But Gross Profit was +27%, EBIT +21%, and EPS +17%. On top of that, the cash conversion cycle eroded by 15 days, the most in seven quarters. That’s due in part to higher footwear inventories, as the company scales up a fundamentally more complex business (lower margin and more capital intensive). Most companies in Consumer Discretionary would be thrilled with this growth algorithm – but not those that trade at 70x earnings.

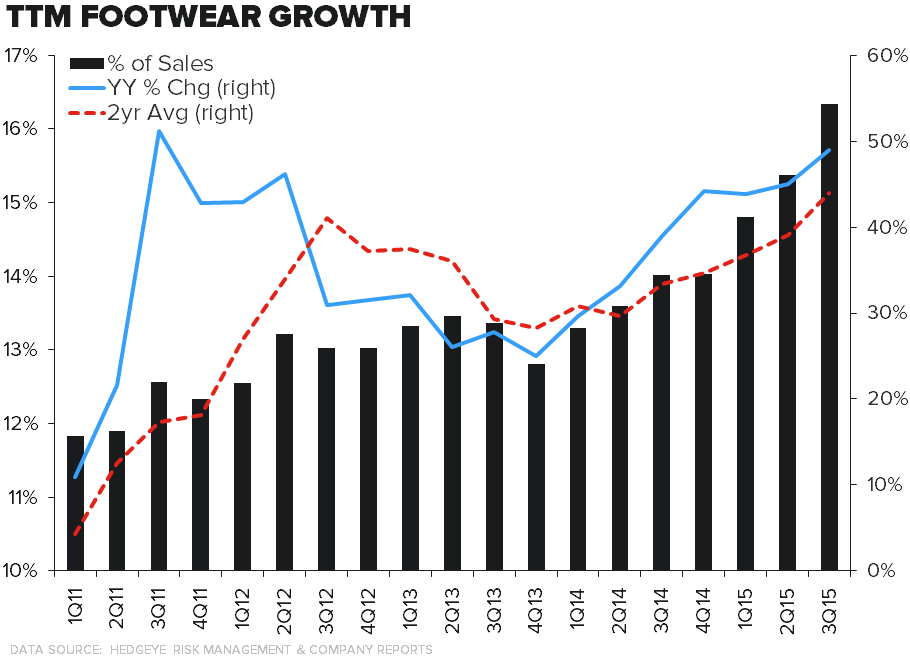

The reality is that this is a generational growth story that is almost always in a state of flux. All great stories are. We’re seeing rapid growth in businesses like footwear, that we would argue are responsible for arguably half of the company’s enterprise value – but just 15% of revenue. This is the most positive trend in the quarter full-stop. We’re looking at 61% growth in footwear, which is the fastest rate of growth since 3Q11, when the business was less than $200mm. In other words, it’s growing faster as it’s getting bigger, which goes against common logic.