We’re punting this one from our Retail Best Ideas list. The name has been ‘Under Review’ from a research perspective as we were waiting for this quarter as a last shot to gain confidence in the underlying growth story. International expansion of PLG brands, which has been the crux of our thesis, has been tracking at the lower end of what we think is acceptable. But unfortunately the bigger problem is that the other 70% of the portfolio is in the US, and that business wants to do nothing but decline. The last thing we want to own here is a portfolio of average footwear brands when we’re late in the economic cycle (actually, the only thing worse would be a portfolio of average apparel brands). We’d rather own something at twice the multiple with an asymmetric growth setup.

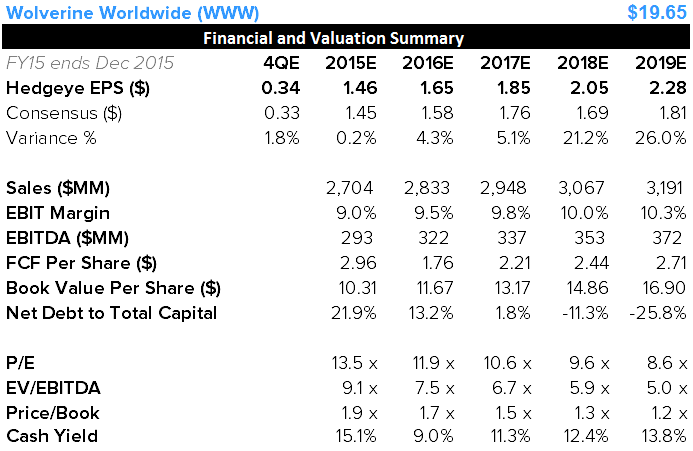

While this is completely hindsight, we’d point out that in 3Q the company put up a decline of 4.5% in revenue, 17.7% in EBIT, 24.4% in EPS, and -70% in cash flow. Inventory was up 6%, representing a negative 11 point delta in the Sales/Inventory spread. It really has never been worse for WWW in this cycle. Its current SIGMA reading (Quad3) is horrible, and is extremely bearish for Gross Margins in the upcoming quarter. Its two largest brands, Merrell and Sperry, which account for 40% of sales, have slowed sequentially (on a constant C$ basis – i.e. we’re not dinging it for FX) in each of the past 4-quarters.

One reason why the value-destructing algorithm is notable is that this company should be throwing off a boatload of cash. And by ‘boatload’ we mean $300mm+. The reality is that this is the first quarter where the TTM cash flow turned down, and we expect that to continue well into 2016.

Why does this matter? Glad you asked. We have yet to meet anyone who owns WWW who does not think that this story ends in WWW doing another deal. After all, they do a deal at the friction points of almost every economic cycle. But the last thing we’re going to do is stay on board with WWW because of a theoretical backdrop of an accretive acquisition. Aside from being Thesis Drift – which we won’t succumb to – we’d note that the muted (and now declining) growth in cash flow implies that the company will have to renegotiate its lending agreements to do a deal, and still will only have $600mm-$800mm to spend. That’s nice, but a far cry from when it bought PLG for $1.2bn – effectively growing the size of the company by 66%.