“Sometimes things strike a chord with people. Simple stuff.”

-Robert DeNiro

I was flying from San Francisco to LA last night and, taking a break from yesterday’s US Retail Sales and economic data slowing, I enjoyed reading Cigar Aficionado’s cover article conversation between Marvin Shanken and one of my favorite actors, Robert DeNiro.

Fully loaded with his 95 movie appearances and 2 Oscars winning performances, De Niro has too much epic content to count. But the aforementioned scene from Taxi Driver (1976) has to be one of the all-time greats.

“You talkin’ to me?” You think we’re gonna get a rate hike? You think growth isn’t slowing? You talkin’ to me? Or are you long the Financials (JPM) and just talkin’ your book? I’m talkin’ mine this morning. That is the game. So let’s keep talkin.’

Back to the Global Macro Grind…

BREAKING NEWS: “Soft patch of data eroding the probability of Fed raising rates in 2015” –Hilsenrath, Wall Street Journal

#Cool

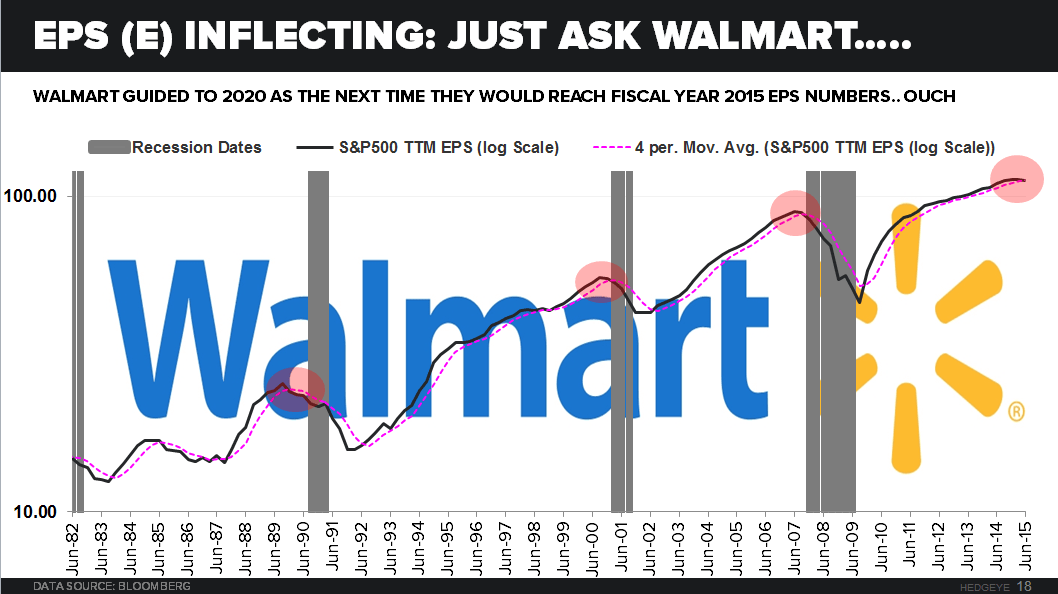

JP Morgan (JPM) reporting a slow-down (and re-testing YTD lows) and Wal-Mart (WMT) losing the most market cap it has in one day in 25 years corroborates with a little more than a “soft patch”, though.

Make no mistake. We’re talkin’ to you. This is a #SuperLateCycle slowdown.

Macro markets obviously agree with what we’ve been talkin’ about:

- US 10YR Bond Yield back below 2.0% this morning to 1.99%

- Russell 2000 -12.4% from her YTD top

- Gold leading gainers +1.7% alongside Treasuries yesterday

Oh, and the US Dollar re-testing her AUG 2015 lows where all of a sudden Down Dollar, Down Rates was seen for what it is – an obvious #GrowthSlowing signal.

But, but, Energy Stocks (XLE) we’re +0.9% on Down Dollar (oversold) yesterday – and Russian Stocks are +2.1% this morning (+9% in the last month) – isn’t that a “demand” signal, or something like that?

Uh, no. If it was, Consumer Discretionary (XLY) stocks wouldn’t have led on the downside (-1.0% yesterday) alongside the Financials (XLF) -0.8% and the Sector ETF (XLP) that has Wal-Mart, -1.2%. If growth was accelerating, rates would be rising too.

And this is what we’ve been talkin’ about on the road in California this week:

- Our #Deflation call is well over a year-old now and not as market-moving as our #GrowthSlowing call

- While both inflation and employment/consumption growth are classic #LateCycle indicators, consumption slows last

- As we enter a cyclical recession (globally), the jobs market looks #SuperLateCycle inasmuch as wage gains and spending do

Sometimes simple stuff, like cycles, strike a chord with people.

So we’re very appreciative of our growing audience on these matters as it’s not enough “this time” (it’s not different this time either) to blame everyone but consensus itself for not performing this year.

At 72 years old, Robert DeNiro gets that performance still matters.

To end on a positive note this morning, being right or wrong on Wall Street shouldn’t ultimately shape your life anyway. When Shanken asked DeNiro “what’s the one thing you haven’t done yet that you want to do before you die?”

DeNiro “pounded the table” and said: “I want to live as long as I can for my kids.” Amen, brother. You’re talkin’ to me.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.96-2.07%

SPX 1

RUT 1095--1179

USD 93.81-95.34

EUR/USD 1.12-1.15

YEN 118.25-120.48

Gold 1150-1187

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer