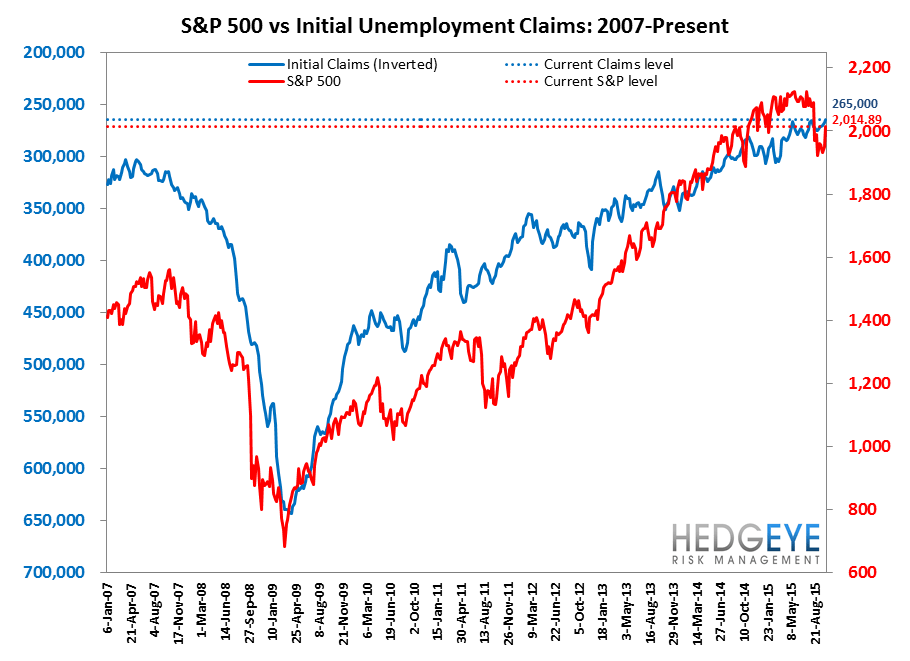

There's growing consternation around the strength of the labor market in the wake of consecutive disappointing NFP reports for August and September. The weekly initial jobless claims series, however, continues to show strength exemplified by this latest weekly reading -- the lowest reading in 42-years. What's an investor to do?

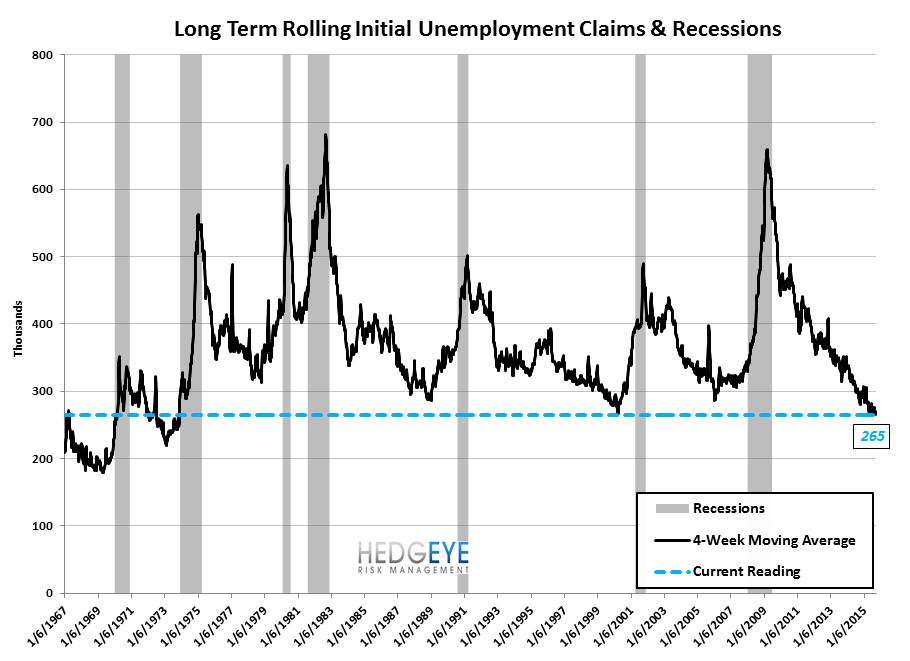

Our framework for thinking about late cycle risk is to start by looking at recent cycles. The last three cycles saw claims stay below 330k for 24, 45 and 31 months before the economy entered recession. The average duration of those three cycles was 33 months (max: 45, min: 24). With claims having just finished their 19th month of strong, sub-330k claims, we are 5 months from the min, 14 months from the average and 26 months from the max. While it's always possible that this cycle could exceed that of the 90s, we think that's a low probability scenario as the 90s cycle represented a near-perfect goldilocks confluence of tailwinds from demographics, technology, peace and government. In other words, we'd put our left tail/right tail boundaries at 5 and 24 months before the start of the next recession and we'll continue to watch the claims data for signals of deterioration. So far, it continues to print lower.

In energy states, indexed claims rose in the week ending October 3 while falling for the country as a whole. The chart below shows that the spread between the two series increased from 18 to 19 week over week.

The Data

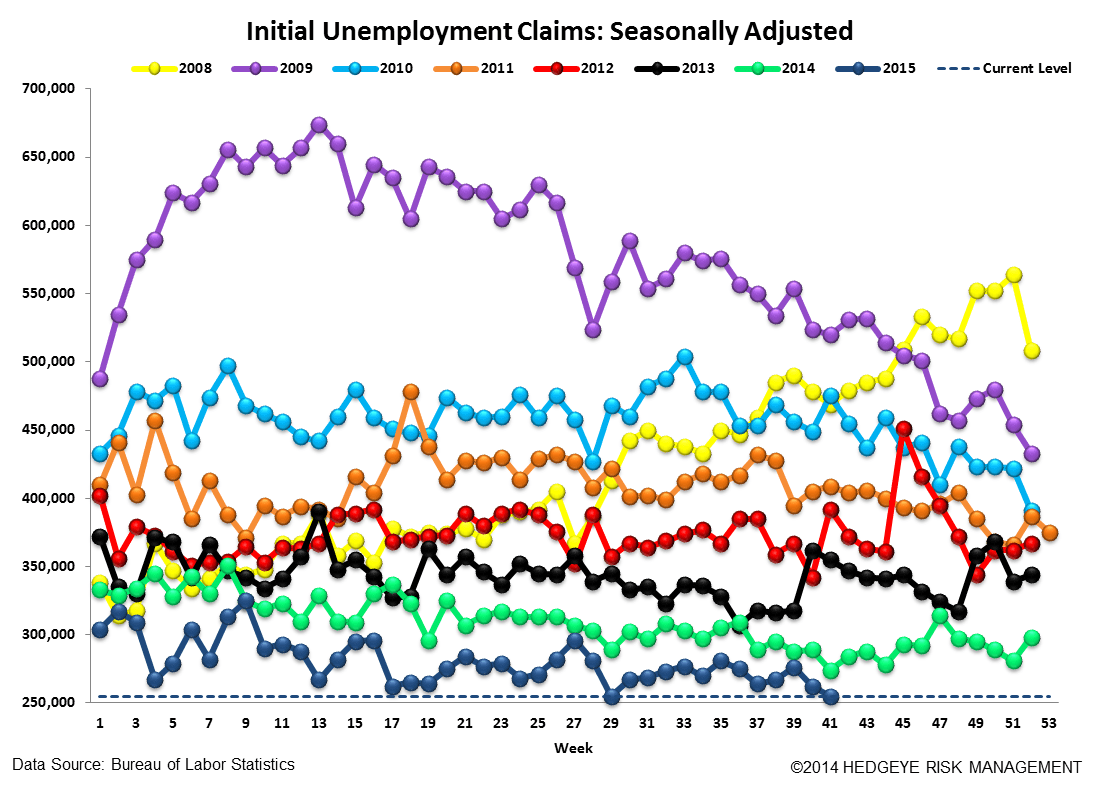

Prior to revision, initial jobless claims fell 8k to 255k from 263k WoW, as the prior week's number was revised down by -1k to 262k.

The headline (unrevised) number shows claims were lower by 7k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -2.25k WoW to 265k.

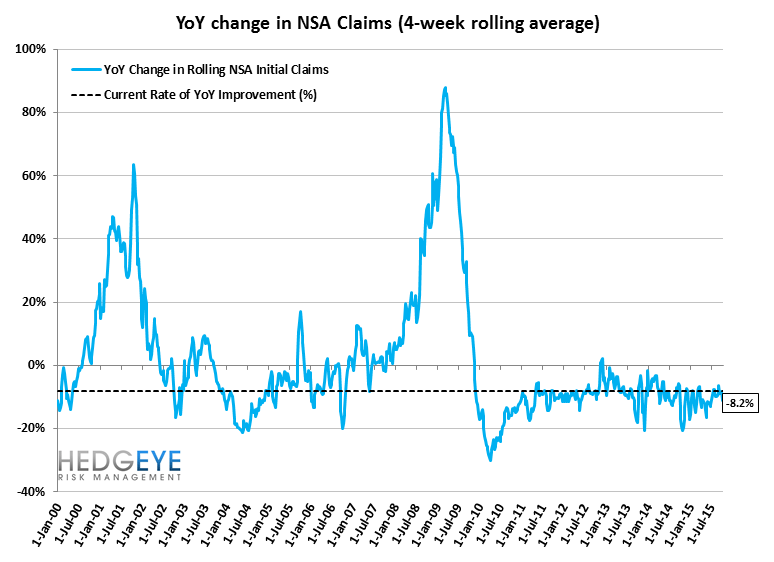

The 4-week rolling average of NSA claims, another way of evaluating the data, was -8.2% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -11.0%

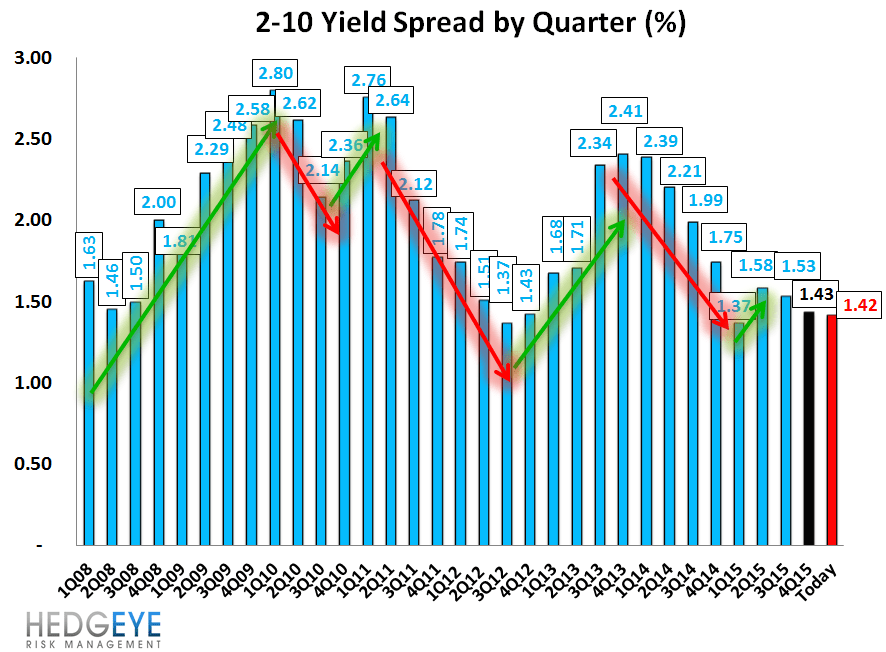

Yield Spreads

The 2-10 spread fell -2 basis points WoW to 142 bps. 4Q15TD, the 2-10 spread is averaging 143 bps, which is lower by -10 bps relative to 3Q15.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT