“Hurting was nothing new to him.”

-Daniel James Brown

That was a formative character quote about 1936 Olympic Gold medal winner, Joe Rantz, in an epic story I’ve been reading called The Boys In The Boat. His parents packed up and left him with the family farm when he was only 15 years old. He had no choice but to fend for himself.

“Each evening (eating by himself at the head of a table in an empty house) Rantz noted with mounting satisfaction that there were fewer boys making the climb. And he noted something else. The first to drop out had been the boys with impeccably creased trousers…” (pg 51)

While I didn’t live during the depression, I did leave home when I was 16 years old. My teammates and I have a DNA that will not fade when we have conviction in something we see that others don’t. Both #Deflation and #GrowthSlowing risks remain. Tell the Establishment we said so.

Back to the Global Macro Grind…

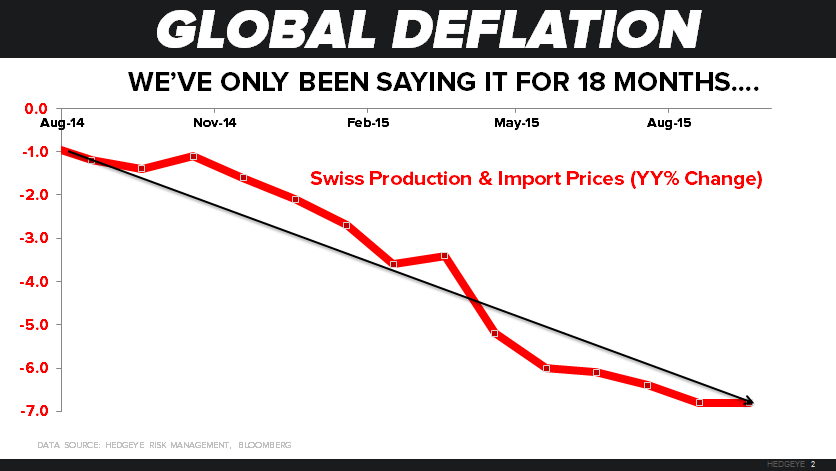

Got, hashtag, #Deflation?

Yep, ask the authors of that call when we think the risk doesn’t remain. We’ve been making this call for over 15 months now. Whether it’s signaling an immediate-term TRADE overbought signal within a long-term bearish TAIL risk or updating the data itself, we’ve had your back.

Away from China’s Imports (one of the few #s they can’t make up) crashing -20.4% y/y in SEP:

- Swiss Producer Price (PPI) #Deflation was -6.8% y/y in SEP (yes, that’s why they have negative bond yields)

- German Econ Sentiment (ZEW index) slowed to 1.9 in OCT vs 12.1 last (= fresh #SuperLateCycle lows)

- UK Producer Prices dropped -1.8% y/y and CPI showed only its 2nd NEGATIVE reading (y/y) since 1960

I know. I know. My Canadian buddy, Francois – who has been saying “don’t pay so much attention to the data” (after telling clients to chase “reflation” and global demand “bottoming” in July) reiterates not to be so data driven. Great.

How about being market driven? After yet another “reflation” rally to lower-highs last week:

- Oil (WTI) got smoked for a -5% loss yesterday and, despite last week’s +9% gain, is -15% in the last 3 months

- Energy Stocks (XOP) were down -4% at one point in the day and remain the worst sector to have been long in 2015

- Emerging Markets (still in crash mode) are leading on the downside (again) this morning with Indonesia -3.2% overnight

But, if we don’t pay attention to the data or market prices, we can pretty much tell ourselves whatever we want, eh? Not @Hedgeye. We aren’t the boys with the creased trousers trying to sell the perma bull.

What’s really interesting about the perma bull on growth and inflation “bottoming” isn’t so much that the growth bulls didn’t call for a slowdown to begin with, it’s that they’re way more bullish than the slow-moving-economists at the Fed, ECB, BOJ, etc.

Check out these comments from linear economists in the last 24 hours (even they get it at this point!):

- "I view the risks to the economic outlook as tilted to the downside.” –Lael Brainard, Federal Reserve

- “We see the possibility of inflation turning negative.” –BOJ Bureucrat

- “It will take longer than expected to reach stable inflation.” –Yves Mersch, ECB

In other words, forget the perma bulls who are still calling for 3.5-4.0% GDP growth (Nancy Lazar). They aren’t even in the debate at this point. The market’s debate (marked-to-market, every day) is purely about the risks of long-term #Deflation vs. immediate-term #Reflation trades.

On US growth, the much more appropriate debate right now is between the Hedgeye low-end scenario of 0.1% Q3 GDP and high-end scenario of 1.5% (SAAR) GDP vs. the Atlanta Fed Tracking model of 1.0%. We’ll get that river card report at the end of the month.

In the meantime, we’ll spend our time this week observing the data we’ve already predicted as slowing (10 months ago) like US CPI, PPI, Retail Sales, and Industrial Production (all due to be reported this week).

Darius Dale and I will also spend plenty of time debating Institutional Investors on the real-time call they need to make (from here) into the end of 2015 – perversely, will the #SuperLateCycle call itself be the catalyst for Down Dollar asset price reflation?

Or will consensus eventually just come to terms with the simple reality that central planners and their cheer-leading economists/strategists cannot CTRL+Print demand?

Deflation risks remain because Global #GrowthSlowing does. The hurt remains on those expecting both higher-growth and higher bond yields.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.97-2.12%

SPX 1 (bearish)

EUR/USD 1.11-1.14

Oil (WTI) 46.07-50.60

Gold 1135-1171

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer