Below are our analysts’ updates on our fifteen current high conviction long and short investing ideas. Please note that we added Tiffany (TIF) and Junk Bonds (JNK) to the short side this past week. As a reminder, if nothing material has changed in the past week which would afffect a particular idea, our analyst has noted this. Hedgeye CEO Keith McCullough’s updated levels for each ticker are below.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or les

IDEAS UPDATES

W

Our veteran Retail Sector Head Brian McGough sent out a full stock report detailing his bearish thesis on Wayfair on Friday. Click here to read it.

tif

In addition to his note on Wayfair, McGough also sent out a stock report outlining in granular detail his bearish case on Tiffany. Click here to read it.

JNK

Our macro team has just released its short thesis on Junk Bonds. Click here to read it.

TLT | EDV | GLD

Bottom Line: We remain 50% below Bloomberg Consensus on GDP growth. Wall Street, the IMF, World Bank and OECD are all still forecasting global growth of around 3% for 2015. We reiterate our call for growth to come in at or below half that rate.

The most recent US jobs report confirmed the top in the #LateCycle US Employment. We highlighted this in last weekend’s report, but gold likes a bad jobs report and any other data point that takes the Fed further away from hiking rates:

- Dollar Down + Rates Down ripped both #YieldChasing and everything linked to Down Dollar Reflation (Gold, Energy Stocks, Russia, etc.) higher.

From labor and manufacturing markets to consumer and business confidence, leading indicators are beginning to roll as the late-cycle moves past peak.

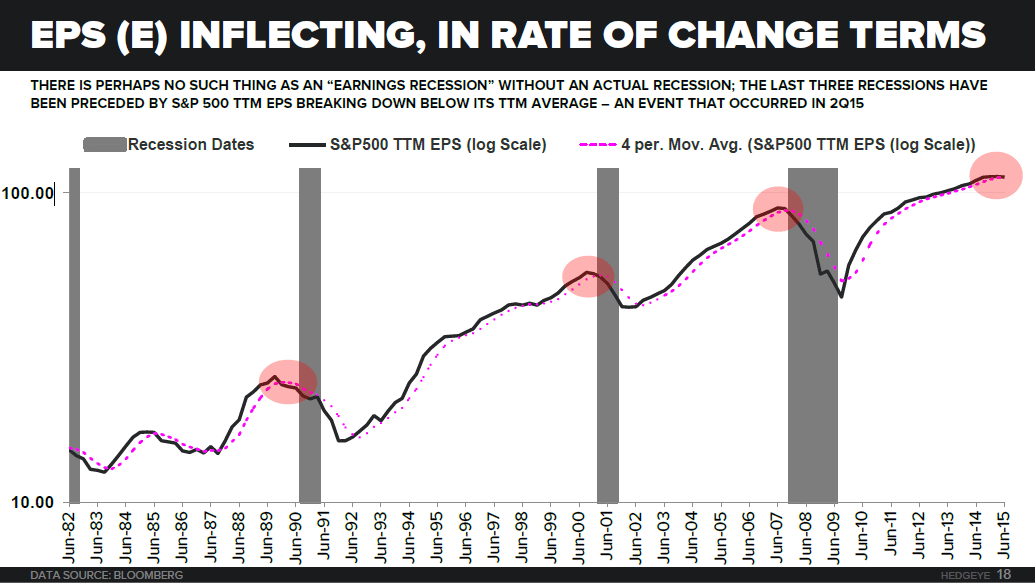

Concentrating on the corporate profit cycle which peaks late cycle, here is a summary of some content from our Q4 2015 macro themes call with respect to S&P 500 company performance:

- EPS is inflecting in rate of change terms. The last 3 recessions have been preceded by S&P 500 TTM EPS breaking down below its TTM average

- Just 37% and 43% of S&P 500 companies recorded sequential acceleration and sales earnings growth in Q3

- Profitability is past peak

- Build-up in customer inventories: A build-up signals a decline in future orders and factory output

While most #LateCycle growth expectations in macro markets peaked in April, the US stock market peaked in July as bond yields hit the market with their last head-fake of a “breakout.” That makes this bear market in growth expectations relatively young. With that considered, sit back and relax with your TLT and EDV.

RH

To view our analyst's original report on Restoration Hardware: CLICK HERE

We think that the catalyst calendar is just starting to pick up, and should be the best that Restoration Hardware has seen – perhaps ever. Here’s the roadmap:

- RH Teen -- launched on September 18th, with subsequent mailing of 200-page sourcebook and dedicated space inside future design galleries.

- RH Modern – launched October 1st. This will have a 500+ page sourcebook with a simultaneous opening of a stand-alone store on Beverly Blvd.

- Analyst Day mid-October.

- Starting Late Sept/Early Oct, Successive Design Gallery Openings In…

- Chicago (62,000 feet in the most elite part of Chicago’s Gold Coast -- but at a non-elite cost).

- Denver (another anchor property -- using 53,000 feet of the 90,000 left vacant by Saks at Cherry Creek).

- Tampa (47,000 feet, which is spot on with what our real estate analysis suggests is appropriate for 10% market share and $1,200/ft).

- Austin (47,000 feet at The Domain – likely to replace one of the two small-format stores in the area, one is just 4-miles away. That makes sense given that our math suggests that Austin could support 50-60k feet for RH).

- Square Footage Growth Returns. Add up the four stores in the point above and we’re looking at about 210k square feet. That alone represents about 25% growth in square footage (and that’s not counting Atlanta). Keep in mind that this company went from over 100 stores pre-recession (and before having a defendable merchandise, real estate strategy, and actual management team) to 67 in the latest quarter as it culled bad locations. Square footage grew on occasion over that period in a given quarter, but has settled in around 850k. Starting in 3Q, we should see square footage growth ramp from a mid-single digit rate in 2Q to a number ~20%, then steadily march towards 35%+ in FY16. Then we’ve got 20%+ square footage growth every year thereafter for at least five years based on our real estate analysis.

So all in, there are two new and significant merchandising initiatives, which are solid on their own. But to pair them with the square footage growth acceleration seems almost like a fantastic coincidence. But it’s not. This has been in the plan all along. There’ll be many more new concepts and classifications – though we’d argue that the company can go deep and add $2bn in revenue with what it has.

To be clear, there’s much more to this story than just square footage growth – like the ability to consistently merchandise product people want in quantities they need. Without the ability to deliver on that requirement, a retailer could have the greatest store in the hottest location with the best demographics, and it will still be nothing but a liability (regardless of how low the rent might be). That’s why square footage growth is grinding to a halt for other US retailers.

That’s also why the growth profile at RH is so powerful, and unmatchable by anyone we see in Retail today.

LNKD

To view Hedgeye Internet & Media analyst Hesham Shaaban's original report on LinkedIn: CLICK HERE

The disappointing Non-Farm Payrolls release for September may be viewed by some investors as weakness for LinkedIn given that much of its business centers around recruitment. However, it’s not net hiring, but rather gross hiring that is the better read into the recruitment industry.

We’ll be getting a read there when the Bureau of Labor Statistics (BLS) releases its JOLTS data next week. As of the last release, there wasn’t any cause for concern.

As mentioned here before, we remain long LNKD into its next earnings release. We’re expecting a clean beat and raise. We expect this will be a positive catalyst for the stock, especially given the current dearth of good Internet longs.

ZBH

To view our analyst Tom Tobin's original report on Zimmer Biomet CLICK HERE

We had two interesting, incremental updates to our Zimmer Biomet short thesis this week. In our process, we attempt to marry the data with anecdotes. This week we managed to accomplish both.

On the anecdotal front, we interviewed an orthopedic surgeon from a major academic hospital in the Midwest. He does 800 cases per year, which is high volume by any measure, and likely means he’s a very fit guy. But more importantly, his comments match our data analysis.

Case volume has been generally very consistent yearly with a modest increase late in 2014. In the most recent months, case volume slowed dramatically. This is consistent with a penetrated market that caught a slight boost from the Affordable Care Act.

This morning we updated our population model that describes what we are expecting for total knee replacement volume. The government released data for total cases by age and payor for 2013 and the results of our mini-experiment were spot on. Growth in younger patients is slow and growth among Medicare patients is fast. That would be positive if not for the fact that Medicare is putting pressure on reimbursement which is subsequently putting intensifying pressure on device costs, and ZBH revenue.

As we heard from our surgeon, they have a “patient matching algorithm” which just means they use cheaper implants in older Medicare patients. And with Medicare rolling out a global payment system for knee replacement surgery reimbursement, the pressure and device deflation will only get worse from here.

GIS

Our Consumer Staples team has no new material update on General Mills this week. They remain positive on the company coming out of the 2Q15 earnings call. We have been long GIS for the last six months and continue to have a favorable view of the company due to the following reasons:

- Sequential improvement in cereal

- Growth in Natural & Organic categories

- Snacking

- Cost cutting initiatives

- M&A activity

ZOES

Our restaurants team has no new material update on Zoës Kitchen this week. They remain very positive on the company long-term.

WAB

To view our analyst's original note on Wabtec: CLICK HERE

Wabtec’s core US freight equipment business is a good franchise, but also a cyclical one. The investment cycle is turning down for global freight rail equipment as decreased mining capital spending and a young US freight equipment fleet constrains spending, as we see it.

WAB is trading at a high multiple on what we expect to be peak results, with estimates reflecting faith in management more than prospective customer activity. Is Wabtec a ‘growth’ industrial even though it serves a mature, static, sub-GDP product category? Is expansion outside of its traditional, structurally robust US freight franchise a solution to slowing freight rail capital investment?

We think the answer to both questions is ‘probably not’, and that investors are mistaking a long investment upcycle for secular growth…much as they did for Joy Global and Caterpillar a few years ago.

MCD

To view our original note on McDonald's: CLICK HERE

Our Restaurants team has no new material update on McDonald’s this week.

The stock continues to be well liked by our research team, and is a perfect fit into our macro team’s style factor preferences. This stock is high cap with a low-beta, coupled with a turnaround story that is well underway. We believe this stock will do well through this tumultuous time in the market.

As you may have read or seen, MCD's all day breakfast began this week. We anticipate this not only driving increased visits from existing customers but also new customers that maybe don’t wake up early enough to get breakfast by 10:30am or just people that enjoy eating breakfast items outside of the morning day-part.

New CEO, Steve Easterbrook has taken an internal activist approach to reorganizing this company and we believe we will see the strong signs of it all working during the 3Q15 call on October 22nd.

FNGN

Our Financials analyst Jonathan Casteleyn has no material update on Financial Engines this week. He reiterates his long term bullish thesis on the company.

PENN

As we predicted, a rise in September regional revenues would serve as a catalyst for regional gaming stocks, and in particular, Penn National Gaming. For the record, PENN is up +12% since we added it to Investing Ideas back in May, outperforming the S&P 500 which has fallen -5% since then.

We believe shares of PENN have a lot more room to run, given its strong performance in key markets like Ohio and its successful opening in Massachusetts. A handful of states still need to report their September revenue figures, but numbers have been in line with our expectations thus far.

PENN will be reporting Q3 earnings on October 22nd.