Below are our analysts’ updates on our thirteen current high conviction long and short investing ideas. Please note that we added Wayfair (W) to the short side yesterday and removed Foot Locker (FL), also from the short side. As usual, if nothing material has changed in the past week which would afffect a particular idea, our analyst has made a note of this. Hedgeye CEO Keith McCullough’s updated levels for each ticker are below.

***In case you missed it, Keith sent a brand new Macro Overlay Friday afternoon. Click here to watch.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or les

IDEAS UPDATES

TLT | EDV | GLD

It was an important couple of weeks for those who were still wrestling with our lower-for-longer views. 50% of the questions we were fielding into lower highs in the 10-year treasury yield pre-September Fed meeting centered around our timeframe for capitulating on our U.S. treasury position. We didn’t field any such inquisitions after Friday’s jobs report.

The brevity of the macro moves post-report Friday proves just how non-consensus that call remains in a year where the S&P 500 is down -8%. None of our trusting clients would refute the fact that we told them to get out of the way of the central planning train-wreck in equities. The scary thing with regard to Janet’s credibility is that bad news is now being priced in as bad news.

Moreover, we believe this late-cycle weakness is likely to remain ongoing.

Keith commercializes the top three things in his macro notebook early every morning by distributing an email to a list of institutional subscribers. On Friday morning, that note hit the inbox at 6:32 a.m. and read as follows with the accompanying chart:

“The Atlanta Fed cut their GDP forecast for Q3 closer to ours yesterday – most of the sell side should too:

- UST 10YR – 2.05% yield into this rate of change slowing US jobs report (see chart attached), so the bond market continues to front-run both Yellen and Wall Street’s overly bullish (pro-cyclical) forecasts; on a bad headline NFP print, no support to 1.98%; on a “good” one, upside to 2.19% - that’s my risk range

- GOLD – is the 3rd time a charm? this is the 3rd time (in 3 months) to buy Gold on a down move (before making a higher-low and ramping for a weekly gain) ahead of the jobs print, and I would – immediate-term upside to $1155

- JOBS – rate of change data/charts don’t lie; political economic pundits do – when rate of change in the jobs market bottomed at the end of 2012, Hedgeye went bullish on US #GrowthAccelerating (particularly consumption) and, as it slows here from the FEB 2015 top, we’re bearish – cycles take time to play out.”

You know the story. The non-Farm payrolls print was a bomb, printing +142K additions vs. +201K additions expected. Immediately following the release:

- Treasuries rallied (TLT +1.7%)

- Gold ripped (GLD +2.3%)

- Equities got crushed (S&P 500 -1.1%)

We’re not going to pat ourselves on the back just because we were one of the only ones with a consistent, coincise view of the domestic economic cycle. Nor do we have a crystal ball that spits out the job number. Rather, we dig into the weeds and study developing trends that give credance to our position in the business cycle.

As we’ve mentioned, the month-to-month non-farm payroll number is unpredictable. The “guess the number segment” on CNBC is a carnival at best. However, studying the cyclical trend provides a longer-term-picture on the general direction of this data series.

While we don’t know what the print is going to be in any given month, we know the direction of the trend. Here’s why:

From a rate of change perspective NFP peaked in February at +2.343% YoY and Re-tracing that growth rate to the upside would require a M/M chg in NFP of +602K. That’s not going to happen.

The last time that happened was September of 1983 as we were coming out of an early 80s recession (hint: employment picks up early cycle).

You can slice the NFP or ADP employment numbers any way you want, but the trend has been one of deterioration: 3M avg. < 6M avg. < 2015 avg. < 2014 avg.

As you can see in the chart, peak rate-of-change in NFP occurs approximately 2-years ahead of the peak in the cycle. Cycles take time to play out, but one thing is for sure: The cycle always cycles.

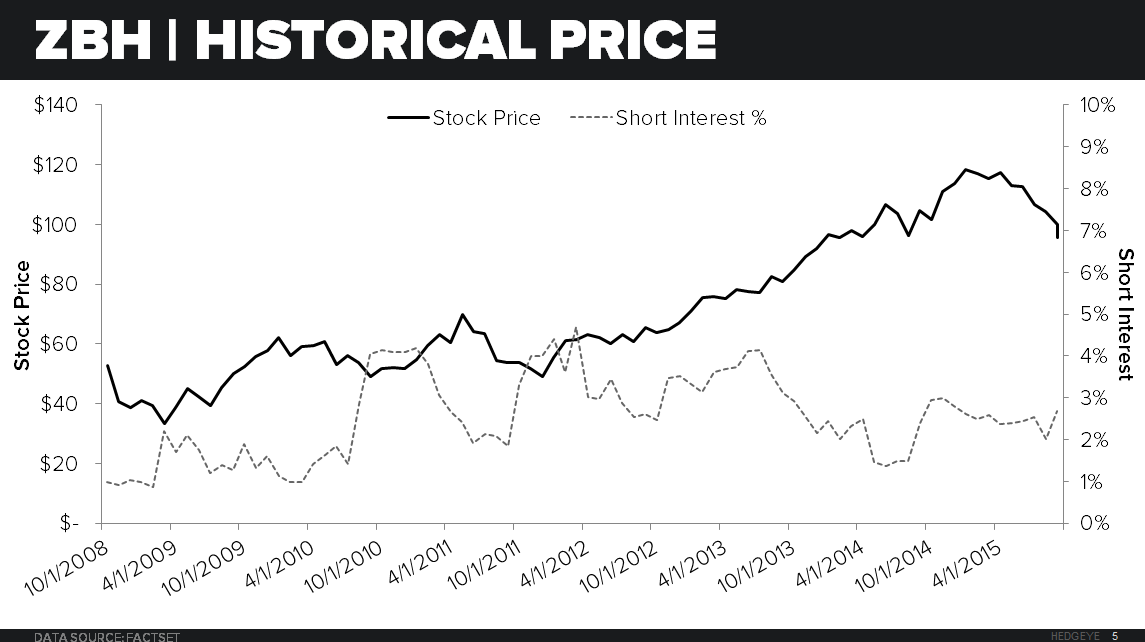

ZBH

To view our analyst Tom Tobin's original report on Zimmer Biomet CLICK HERE

We have been across the country and back again meeting with institutional investors this week and last. We fielded a lot of questions and some skepticism on our Zimmer Biomet short thesis. Generally, our sense is most investors are negative on ZBH and getting more negative as we head into 3Q15 earnings.

It seems likely to us that growth is slowing across the US Medical Economy as the US digests the massive stimulus 24 million new healthcare consumers produced by the ACA in 2015. We’re very sure there has been accelerated consumption across ER visits, physician offices, and pretty certain there was a tailwind for ZBH knee revenues as well.

Sentiment is a key risk factor heading into earnings. Are investors too bearish? Where are expectations? What is the sellside saying? What we know today is that Healthcare employment and Hospital employment remained strong in September, suggesting the #ACATaper has yet to make landfall.

The next update critical to our ZBH short thesis will be the updated job openings for healthcare (JOLTS) employees which will be reported October 16th. If demand is weakening, openings will slow again as they did last month, and we’ll make the assumption that growth in knee replacement surgery, ER visits, imaging studies, and host of other medical procedures is grinding toward negative growth for 4Q15 and beyond.

GIS

Our Consumer Staples team remains positive on General Mills coming out of the 2Q15 earnings call. We have been LONG GIS for the last six months and continue to have a favorable view of the company due to the following reasons:

- Sequential improvement in cereal

- Growth in Natural & Organic categories

- Snacking

- Cost cutting initiatives

- M&A activity

RH

To view our analyst's original report on Restoration Hardware: CLICK HERE

RH Modern launched on the company’s website on Wednesday, October 1st and now has its first retail presence as of Friday when the company opened its new 40k+ sq. ft. store in Chicago. That will be quickly followed by a 540 page Source Book launch, a stand-alone Modern store in Los Angeles, and additional square footage in the new galleries in Denver, Tampa, and Austin, TX.

This is a lot more than a new category or concept for Restoration Hardware. We think it’s more like a classification.

Think about it … everything that RH currently sells – whether it be Sofas, Chairs, Tables, Lighting, Flooring, Kitchen – that all falls under the traditional RH aesthetic. RH Modern, however, allows the company the opportunity to take every single category it sells, layer them over a new classification, and sell to a completely different customer.

There will likely be additional classification expansions for RH in the future. Modern, along with other yet to be named category/product line launches, will play an important role in the company getting to its target of $4bn-$5bn in sales.

ZOES

Zoës Kitchen has named Sunil Doshi their new CFO. He was previously the CFO for Fossil Americas. This is not a positive or a negative but it is good to see they filled the position with a person that has a strong background.

Our restaurants team remains very positive on the company long-term.

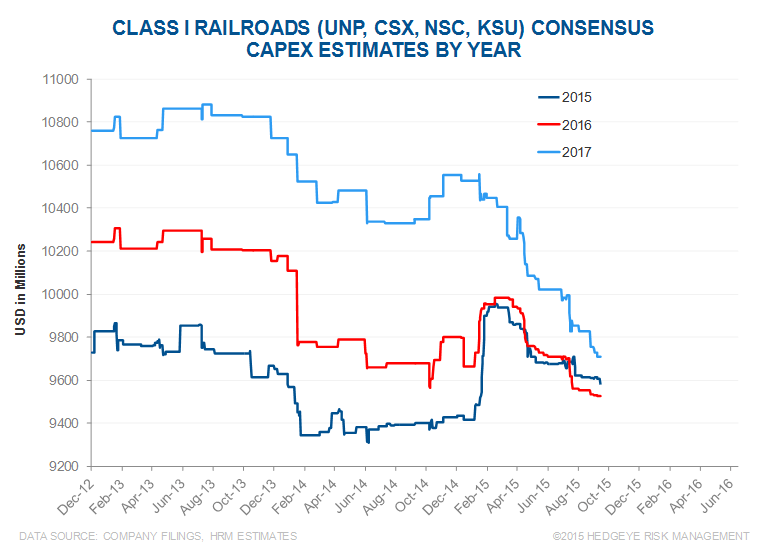

WAB

To view our analyst's original note on Wabtec: CLICK HERE

Since we added Wabtec on the short side in September, shares have fallen -6.3% versus the S&P 500 which has fallen -1%.

Signs continue to mount that the rails themselves will have lower than expected capital spending in 2016 and 2017. Consensus estimates for the large public Class 1 rails have tumbled – starting right around when we did our Rail Capex/WAB black book.

We expect capital spending guidance accompanying Class 1 4Q 15 earnings reports to be an important catalyst for Wabtec shares.

LNKD

Hedgeye Internet & Media analyst Hesham Shaaban has no material update this week. To view his original report on LinkedIn: CLICK HERE

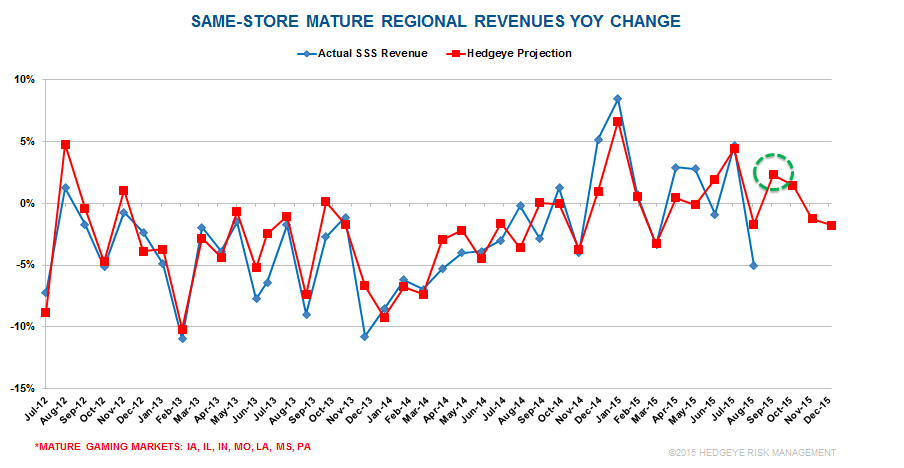

PENN

Many of the regional gaming states will release September revenues next week and as we’ve written about, they should look a lot better than August. Overall same store revenue declined 5% in August (we had predicted –2%) but most of the decline was due to the calendar and a difficult comparison. For September we are projecting an increase of 2% YoY

Our Missouri tracker is forecasting September gaming revenues to be up 3.6% YoY. This is a 6% sequential improvement from August's YoY change of -2.5%. Meanwhile, Pennsylvania slot revenues were up 4% in September

Our thesis for a sequential rebound in September remains intact. We like PENN on the long side from these levels.

MCD

To view our original note on McDonald's: CLICK HERE

McDonald’s continues to be well liked by our research team, and is a perfect fit into our macro team’s style factor preferences. This stock is high cap with a low-beta, coupled with a turnaround story that is well underway. We believe this stock will do well through this tumultuous time in the market.

MCD has all day breakfast starting next week on October 6th, we anticipate this not only driving increased visits from existing customers but also new customers that maybe don’t wake up early enough to get breakfast by 10:30am or just people that enjoy eating breakfast items outside of the morning day-part.

New CEO, Steve Easterbrook has taken an internal activist approach to reorganizing this company and we believe we will see the strong signs of it all working during the 3Q15 call on October 22nd.

FNGN

Shares of Financial Engines continue to get pushed down in a negative broader equity tape despite improving fundamentals. While over the longer term, the rationale for self-directed 401K investors to subscribe to the company’s services improves as DIY investors lose more money than professionally managed, optimized portfolios, investors continue to push the broader asset management sector stocks down.

FNGN hit records levels of assets-under-management and also assets-under-contract in its most recently reported quarter, a vast divergence from the active management industry which has been bleeding assets all year.

With this fundamental improvement in the firm’s fundamentals year-to-date, the stock does not deserve to trade at a new low market cap-to-AUM percentage of 1.3%. The average level since the firm’s IPO in 2010 has been 2.3% providing lots of upside when the company’s valuation improves.

W

Retail Sector Head Brian McGough added Wayfair to the short side on Friday. We will send out a full stock report detailing his bearish thesis in the upcoming week.