Starbucks has been a tricky one for us, we tried shorting it back in January of 2015, betting on the food being the demise of the brand, but admittedly the timing was off. Looking ahead, although the food is not driving traffic, we don’t believe that it is tarnishing the brand at this point. The overriding theme driving the SBUX bull case is Mobile Order & Pay. So with the next big initiative being Mobile Order & Pay, we wanted to test out its impact on traffic, customer throughput and general customer/partner experience.

view our experience with Mobile Order & Pay at Starbucks below

The company has specifically set expectation high for the impact of Mobile Order & Pay. On the 3Q15 earnings call SBUX CEO, Howard Schultz, said “By enabling our customers to order ahead and avoid waiting in line, Mobile Order & Pay is enabling us to capture more on-the-go customer occasions, and the data is clear. In those stores where Mobile Order & Pay has been deployed, lines are shorter, service is faster, and in-store operations are more efficient. The net result is increased traffic, incrementally, that is exceeding expectations, improved throughput, and an elevated Starbucks experience for our customers.”

With that statement Mobile Order & Pay appears to be the Holy Grail for SBUX!

Our initial indications are that in its early days Mobile Order & Pay is going well for the company. The following is a survey we conducted, asking 200 Starbucks customers; “How would you rate your experience using the Starbucks Mobile Order & Pay App?” The results were largely positive, with an average rating of 3.5 stars. In addition to the survey we also tested the system with Hedgeye employees, and it probably balanced out to the same rating. Once the app was downloaded and credit card information inserted everyone had a positive experience. When asked whether they would use it again, some people prefer the in-store ordering experience, but the majority said they would use it again.

We asked the store employees (partners) about the app and how it works for them. They had overwhelmingly great reviews on the app giving them more time to produce orders at an even pace. With the more even pace of incoming orders the partners are able to more efficiently produce the drinks and get them out in an orderly fashion.

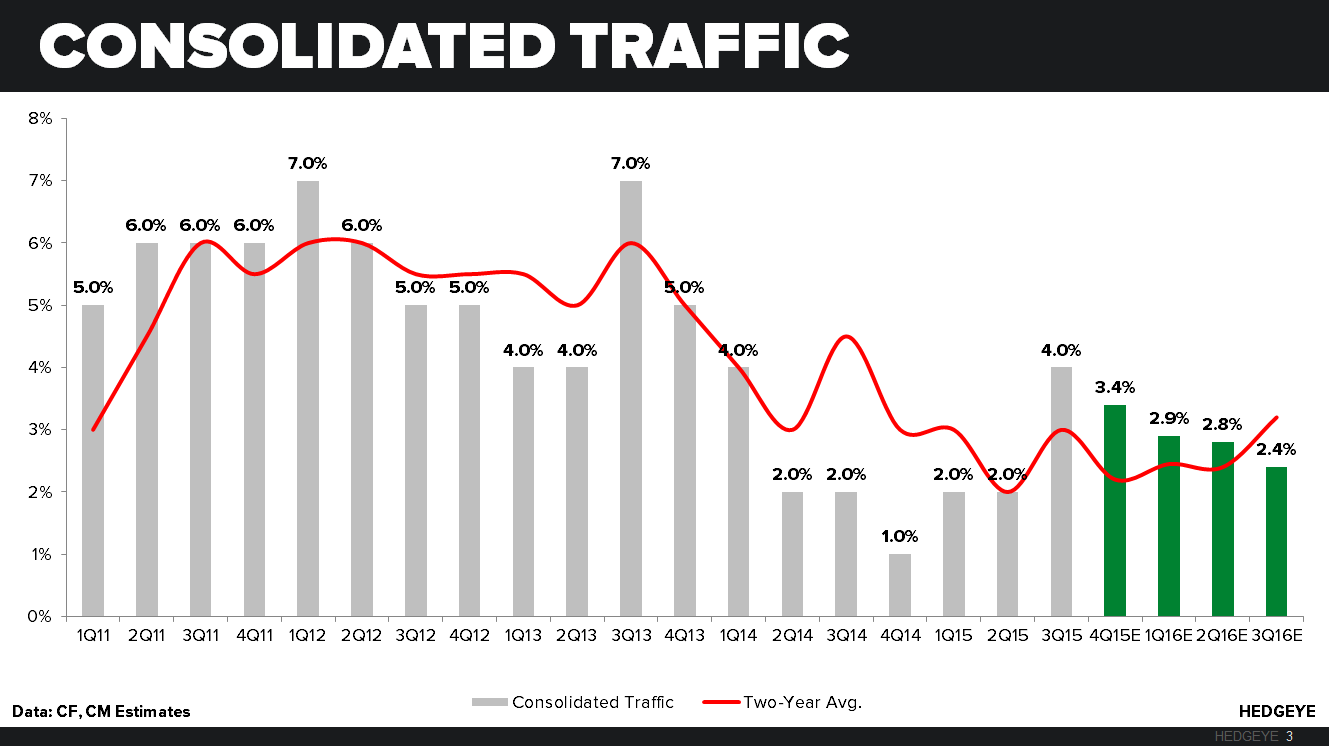

In addition to increasing throughput and efficiency of the store, this app is meant to help drive incremental traffic. In the chart below assuming flat 2-years trends, estimates for Americas traffic, would accelerate to 5% in 4Q15. This would be a significant positive for the company and likely make the consolidated traffic number look conservative. We believe with the new app launched nationwide, consensus estimates may turn out to be slightly conservative.

This new app sets up a TREND duration bullish thesis on Starbucks. Long-term (1-3 years) we remain skeptical on the current food being a driver of growth, but at this point it is not tarnishing the Starbucks brand in any way. After our test/survey we are bullish on the company and the stock for the next 2-3 quarter timeframe.

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst