ADJUSTMENTS TO THE BEST IDEAS LIST

HABT: HABT is down 25% over that last three months and down 40% from its POST IPO high of $41.89 back on 12/12/14. The declines in the stock price and the strong fundamentals now have the stock more reasonably valued at 12x NTM EV/EBITDA. HABT is one of the recent IPO’s we have been tracking on the SHORT side but never really pulled the trigger to get more aggressive on the SHORT. That being said, the stock might not be a great SHORT at this point. We believe that the overall fundamentals of the company are sound and believe the stock could be setting up to be a LONG. The concept and management have always been great and valuations have come down to more modest levels. We are going to monitor and dig in a little further, and hopefully will be moving it above the line in the coming weeks.

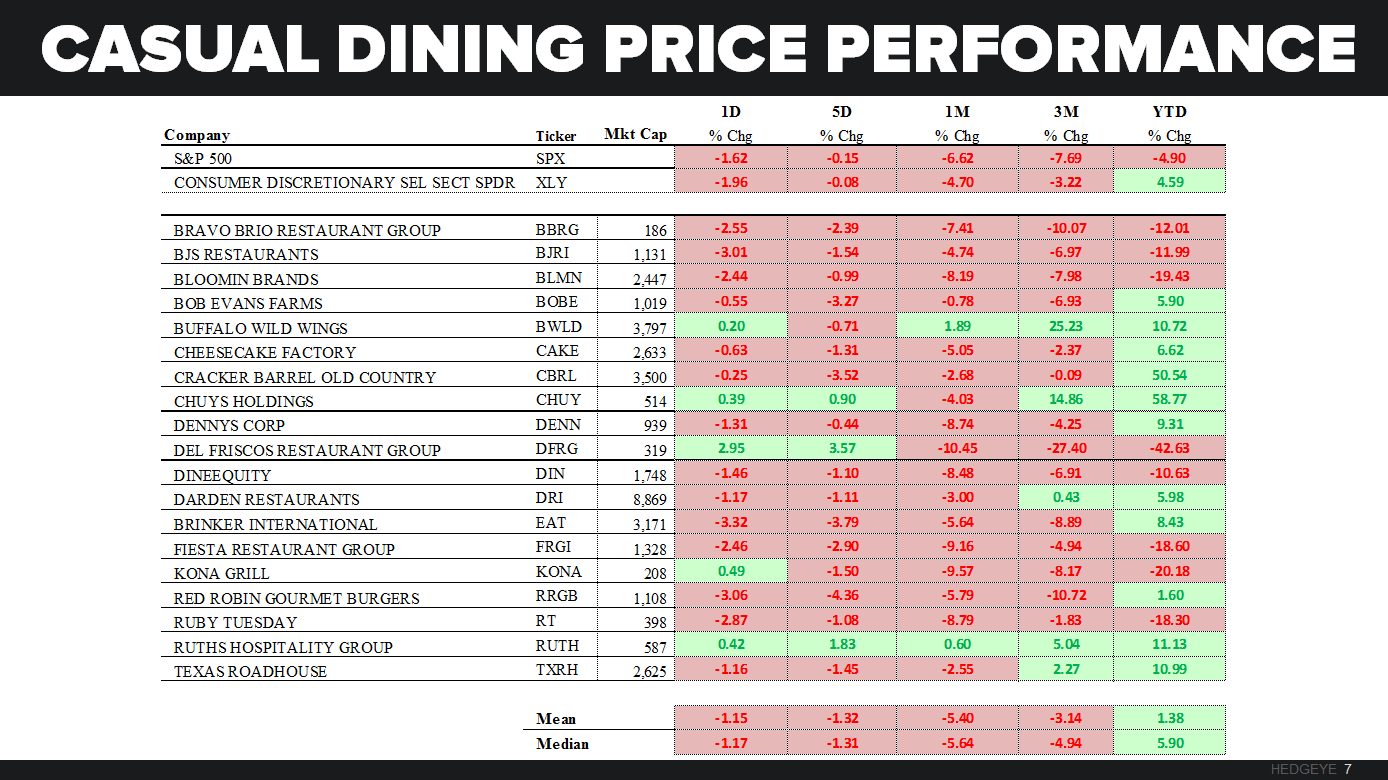

DFRG: This stock has been beaten to a pulp, down ~30% over the last three months. We are starting to feel that at 6x EV / NTM EBITDA all the bad news has been priced into the name. Management recently spoke about changes to the operating model that should improve profitability in 2016. Specifically, slowing growth of “The Grille” and closing two unprofitable locations are good news. These two events will help put a floor on the stock, and will ultimately help sentiment and improve profitability. Unfortunately, the company's strongest brand, The Double Eagle, is seeing slowing sales trends due to market volatility and the associated decline in banquet business. As for the changes within their control, this is exactly what we want them to be doing, and we believe that they will get the Grille concept running smoothly.

RECENT NOTES

9/16/15 SHORT SMALL-CAP BURGER CHAINS | QUICK SERVICE CAN’T AFFORD $15 MINIMUM WAGE

9/15/15 August Restaurant Sales and Employment Trends

9/15/15 SONC | FIRST MISS – EXPECT MORE TO COME

9/01/15 MCD | ALL DAY BREAKFAST IS OFFICIALLY LAUNCHING ON 10/6

RECENT NEWS FLOW

Thursday, September 17

JMBA | Announced the signing of a 13 store refranchising deal in southern California, 88% of their stores are now franchised (ARTICLE HERE)

BWLD | Will stop airing commercials with spokesman Steve Rannazzisi after he made up a story of being at the World Trade Center during the terrorist attacks (ARTICLE HERE)

Wednesday, September 16

CBRL | Reported 4Q15 that disappointed on the top-line, reporting revenue of $719mm versus consensus of $726, as well as FY2016 guidance that came in below consensus estimates (ARTICLE HERE)

DFRG | Opened a new Grille location in Little Rock, AR, this marks the 20th Del Frisco’s Grille (ARTICLE HERE)

Tuesday, September 15

YUM | Taco Bell is opening first ‘Cantina” units with alcohol in Chicago and San Francisco that are meant to appeal more to the millennial generation (ARTICLE HERE)

Monday, September 14

QSR | Tim Hortons has improved its lunch offering, adding four new sandwiches to the menu in an effort to entice afternoon customers to buy food and not just drinks (ARTICLE HERE)

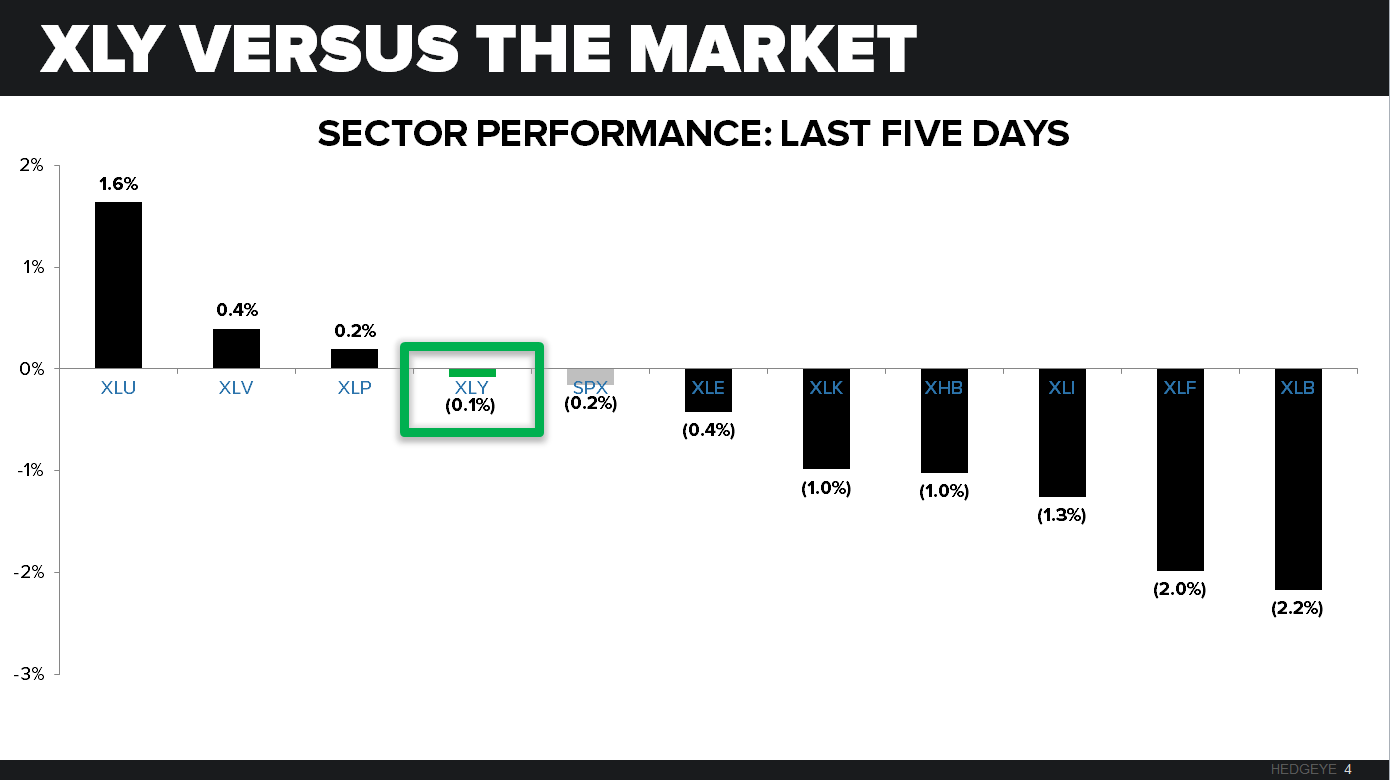

SECTOR PERFORMANCE

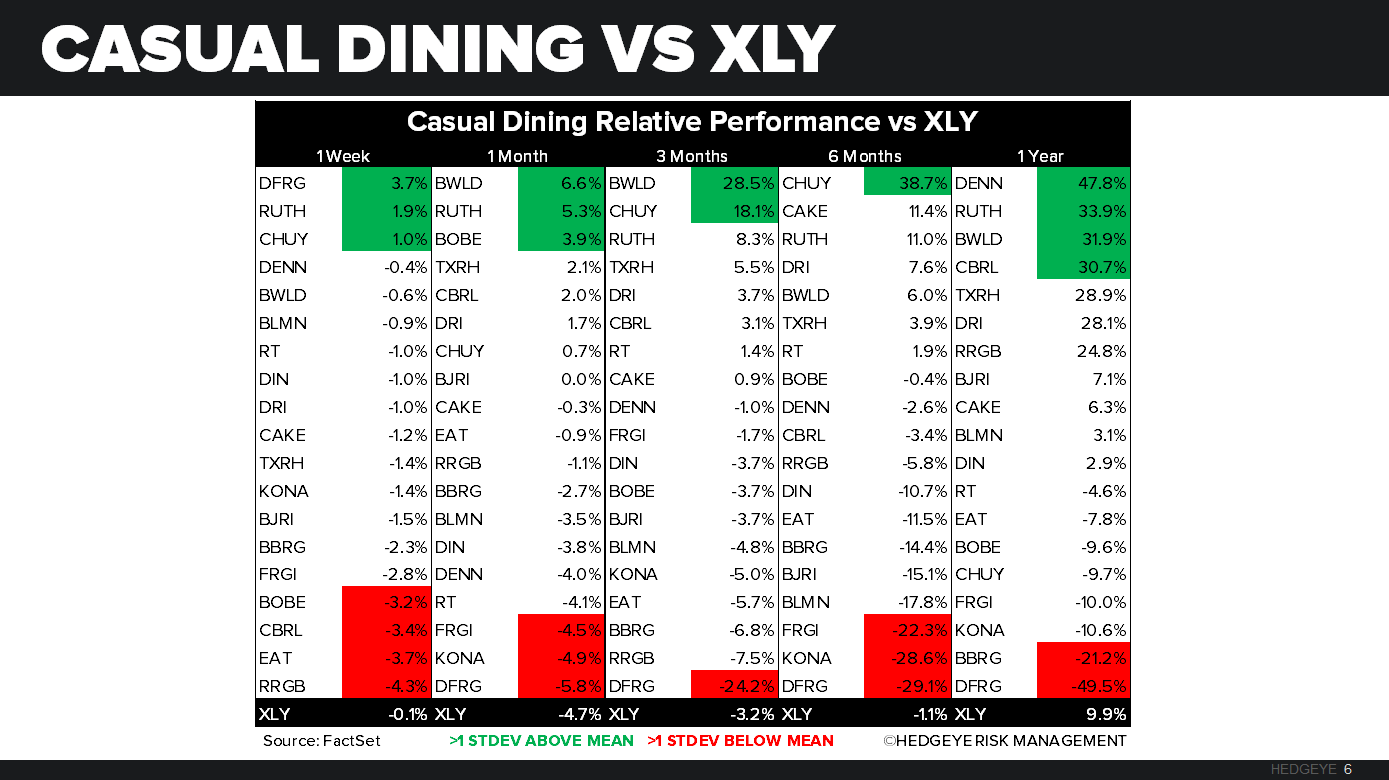

Casual Dining and Quick Service stocks that we follow widely underperformed the XLY last week. The XLY was down -0.1%, top performers on a relative basis from casual dining were DFRG and RUTH posting an increase of +3.7% and +1.9%, respectively, while NDLS and JMBA led the quick service group this week up +6.6% and +6.1%, respectively.

XLY VERSUS THE MARKET

The XLY has fared better than most other sectors in the YTD time period and as of late especially. In the last five trading days while the SPX was down -0.2% the XLY was down only -0.1%, outperformed only by XLP (Consumer Staples), XLV (Healthcare), and lastly XLU (Utilities).

QUANTITATIVE SETUP

From a quantitative perspective, the XLY looks bearish from a TRADE and TREND perspective, TRADE support is 73.64.

CASUAL DINING RESTAURANTS

QUICK SERVICE RESTAURANTS

Keith’s Three Morning Bullets

Dovish Fed = Oil, Gold, EM all up last wk; Rate Sensitive Stocks (Utes, REITS) outperformed big time too:

- DAX – the Fed’s Dollar Devaluation (EUR/USD +2.5% m/m) thing isn’t appreciated by either the DAX or Draghi (he testifies to European Parliament Wed); DAX down another -0.6% w/ keeping the crash (-20.4% since APR) in play, but signals immediate-term oversold here, for a trade

- OIL – Gold and Oil were +3.2% and +0.7%, respectively last week (vs. SPX -0.2%) and WTI is up another +1.5% to $45.34 this morning taking it to +5.7% in the last month (vs. SPX -6.6%) – is the new perma bull US stock market catalyst “higher gas prices”?

- YEN – signaled immediate-term TRADE overbought on Friday as the USD was signaling oversold (and Gold immediate-term overbought); the risk ranges in all of these big FICC trades (USD, Rates, Oil) are narrowing now (leading indicator for lower highs in volatility)

SPX immediate-term risk range = 1; UST 10yr Yield 2.11-2.21%

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst