This was a textbook print from RH – or for any company, for that matter. RH put up the best comp in all of US retail this quarter with 16% brand comp and 19% store comp. That drove 26% EBIT growth and 27% EPS growth. RH beat by a penny, but took up the lower end of the year by $0.03 more than the 2Q beat. That upside is coming entirely in the fourth quarter, and as we suspected (see below) this all allowed RH to set the bar low for 3Q as revenue from new businesses will not be booked until 3Q closes in October. We think all of this sets up for a beat in another 90 days, at the same time square footage growth is accelerating to 29% vs 7% in 2Q, new concepts (RH Modern/RH Teen) are in full swing, and EPS is growing 40%+. This is going to be a rough time for the bears – especially with 25% of the float short.

Transformational stories like RH are not linear, and this one certainly has not been. The stock chart over three years certainly proves that. But it also proves that the people who bought on quarterly noise have made money almost without fail. If the market decides to sell off based on lower guidance in 3Q (i.e. if the after-market gains reverse), then consider it a gift. Fundamentally and financially, we’re about to see growth at RH go on a multi-year tear. We think this stock is headed to $300 over the next 2-3 years. We’ve been patient for the catalyst calendar to begin, and the waiting is finally over.

For a full rundown of our thesis see our latest Black Book published in July.

RH: Road to $300 (Link: CLICK HERE)

09/09/15 05:48 AM EDT

RH | What Could Go Wrong?

Takeaway: We’re confident in RH across durations. But when asked about the ‘worst that could [realistically] happen’ on Thurs, here’s our answer.

We think that the core long-term call on RH is as clear as ever, as is the catalyst calendar over the next six months. We outlined all of this in our two recent Black Books 1) Road to $300 (Link: CLICK HERE), 2) Home Furnishings Deep Dive (Link: CLICK HERE).We also think that the numbers RH will report on Thursday will be spot-on with the type of model we expect to see from RH going forward (comp 14%, Revenue 18%, EBIT growth 25%, Cash Flow 30%+).

But yesterday someone asked us…

Q: “What’s the worst we could hear from RH on Thursday”?

Our answer sounded something like this (actually it sounded exactly like this)...

A: “We’re not worried about the print. RH has never missed a quarter and it’s not going to start now. This will be one of the lighter quarters of the year, and earnings should STILL grow 25-30%. If there’s any bad news, it will likely come in the 3Q comp guide – with earnings potentially shifting into 4Q. There are some legitimate factors that could cause a lull in the top line, and whether or not they materialize, our bet is that the company invokes them to keep expectations grounded.“

Let’s put ‘light guidance’ into perspective. We think that a worst case comp guide is in the high-single digits (we think less than 30% probability). That would leverage to revenue growth in the low dd, and EBIT/EPS 30%+ (the consensus is at 37%). If the worst case scenario were to happen, we’d have to give the revenue/earnings to the fourth quarter. In other words, the year really does not change materially. Also keep in mind that there is little upside baked into the guidance in 2H from the new categories which already calls for the underlying growth rate to accelerate by 350bps. It’s also worth noting that the company would have to guide 3Q comps as low as 5% in order for the 2-year trend to turn down. We put less than a 5% chance on that happening.

What would cause 3Q guidance be light? There are three meaningful business drivers in 2H that move the needle.

1) RH Teen -- launch on September 18, with subsequent mailing of 200-page sourcebook and dedicated space inside future design galleries.

2) RH Modern – launches within a week of RH Teen. This will have a 370-page sourcebook with a simultaneous opening of a stand-alone store on Beverly Blvd

3) Starting Late Sept/Early Oct, Successive Design Gallery Openings In…

- Chicago (62,000 feet in the most elite part of Chicago’s Gold Coast -- but at a non-elite cost).

- Denver (another anchor property -- using 53,000 feet of the 90,000 left vacant by Saks at Cherry Creek).

- Tampa (47,000 feet, which is spot on with what our real estate analysis suggests is appropriate for 10% market share and $1,200/ft).

- Austin (47,000 feet at The Domain – likely to replace one of the two small-format stores in the area, one is just 4-miles away. That makes sense given that our math suggests that Austin could support 50-60k feet for RH).

Here’s why timing matters.

1) Delivery, Not Order = $. It will take a six months to build mass awareness for the new concepts, but RH should begin to take customer orders at a level that actually matters within 3-4 weeks of launch. Let’s say $50mm combined for both concepts right off the bat. We’re talking about roughly 8 to 9 points of comp in the quarter, which would be an extremely solid start. But the problem is that even if the orders are placed for both concepts by October 1, then we need to count forward by at least six weeks for revenue recognition, as customers only pay for product upon final receipt. That puts the sales into mid-November, which is the first month of the fourth quarter.

2) Ditto for store openings. Chicago and Denver are likely the only stores to impact square footage count for 3Q, but only around 5% of revenue is ‘cash and carry’, meaning that the consumer walks out with the purchase on the same day. The rest of the revenue builds into the fourth quarter P&L.

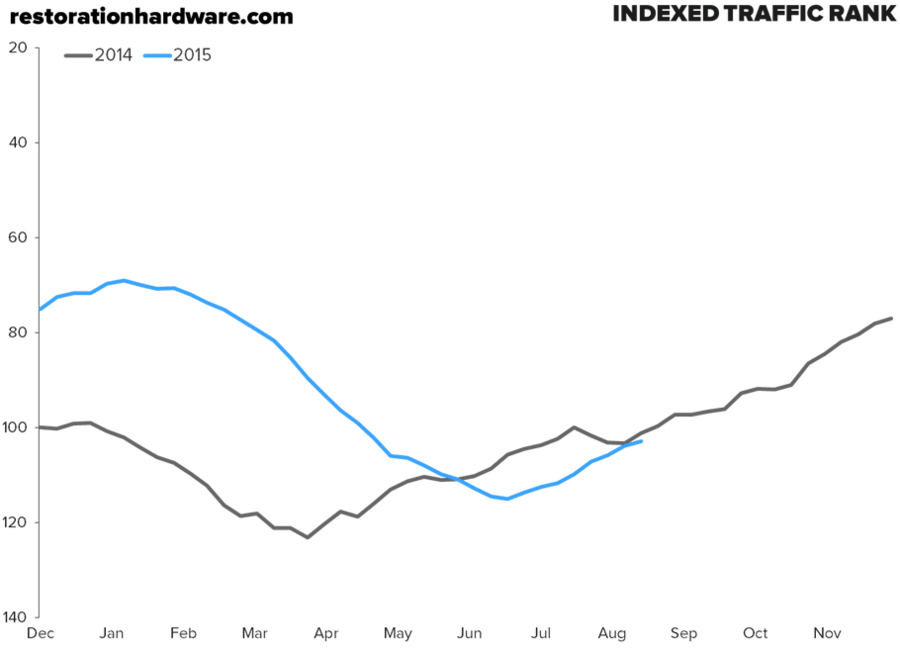

3) RH Cleared The Deck. In anticipation of its new concepts and stores, RH explicitly noted on the last call and on the recent convert Roadshow that there would be a lull in the summer as it relates to new product. That has, in fact, shown up in the online data that we track for RH, as visits to the site seem to have fallen behind last year for the better part of eight weeks. This week’s reading shows that RH is back on par with last year, and we expect that to head meaningfully higher throughout the third quarter. But again, there’s a good 6-8 week lag between the pick-up in business that we see vs. when RH actually sees it on the P&L.

One other reason why RH might guide lightly. Simply put, because it can. It has never had such a position of strength, yet the shorts are already betting against RH with 25% of the float held short. It has two major initiatives that are stand-alone multi-year growth platforms, and we wouldn’t be surprised to see another announced by the time the year is done. Add up the four stores being added this year and we’re looking at about 210k square feet. That alone represents about 25% growth in square footage (and that’s not counting Atlanta). Keep in mind that this company went from over 100 stores pre-recession (and before having a defendable merchandise, real estate strategy, and actual management team) to 67 in the latest quarter as it culled bad locations. Square footage grew on occasion over that period in a given quarter, but has settled in around 850k. Starting in 3Q, we should see square footage growth ramp from a mid-single digit rate in 2Q to a number ~20%, then steadily march towards 35%+ in FY16. Then we’ve got 20%+ square footage growth every year thereafter for at least five years based on our real estate analysis.