Below is the breakdown of this morning's labor data from Joshua Steiner and the Hedgeye Financials team. If you would like to setup a call with Josh or Jonathan or trial their research, please contact

3, 2, 1 ... Countdown

Claims remain on a countdown ... We're now 19 months into the sub-330k environment. For reference, the last three cycles saw claims stay below 330k for 24, 45 and 31 months, respectively before the cycle gave way to recession. The average of those three cycles is 33 months. This implies ~14mos of track to the average of the last three cycles. Obviously, this is simply a reference point and the duration could more closely resemble that of the late 1980s (24mos), which would imply ~5mos of track remaining, or that of the late 1990s (45mos) implying ~26mos of track.

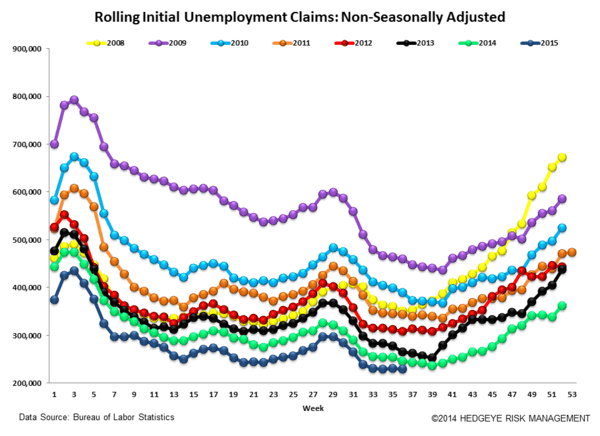

One thing that's more certain and more imminent is the re-convergence toward zero in the rate of change Y/Y. This week that rate of change compressed to -6.6%, down from -9.1% in the prior week. We're finally lapping the floor in claims and within a month the Y/Y rate of change will be ~0%. From that point on, flagging early stage deterioration in the labor market will be a function of noticing any persistent and/or trending rise in Y/Y claims activity.

The Data

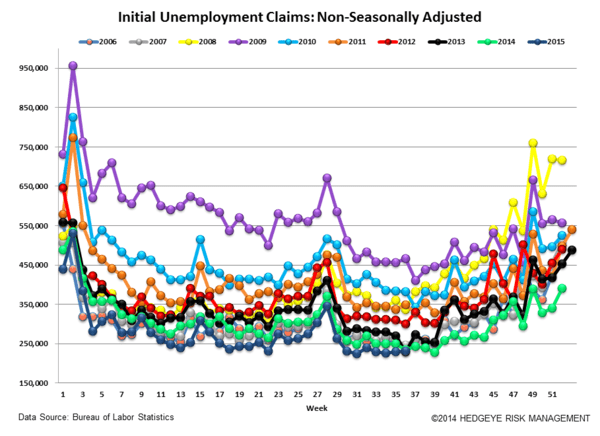

Prior to revision, initial jobless claims fell 7k to 275k from 282k WoW, as the prior week's number was revised down by -1k to 281k. The headline (unrevised) number shows claims were lower by 6k WoW.

Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 0.5k WoW to 275.75k. The 4-week rolling average of NSA claims, another way of evaluating the data, was -6.6% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -9.1%.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT