Editor's Note: The following chart and excerpt are from this morning's Early Look which was written by Hedgeye Director of Research Daryl Jones. Click here if you would like to learn more about how you can subscribe.

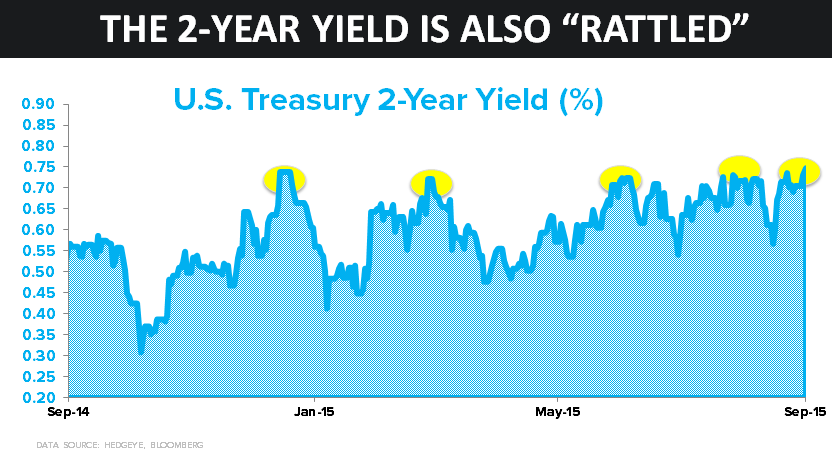

...Speaking of "rattled," the short-duration Treasury market is completely rattled as it relates to digesting the Fed's intentions. In the Chart of the Day below, we show a chart of the 2-year Treasury yield, which emphasizes the inability of the 2-year to break through the 0.74% yield level. Certainly, it has made attempts to breakout, but alas, it continues to fail as the likelihood of the Fed increasing rates gets pushed out further and further.