HAIN remains on the Consumer Staples Best Idea list as a SHORT.

We continue to believe that HAIN is a collection of brands and businesses that are not deserving of the premium valuation. The company is only one of a few that participate in the “better-for-you” space, but not all companies are created equal. HAIN’s business model is a risky roll-up story whose better days are in the past.

The most recently reported 4Q15 only confirms this belief and the issues the company faces today are very relevant to the future of the company.

- Business trends and a sum of the part analysis suggest that the UK business is overvalued

- The drive to cut costs increases business risk

- The quality of earnings is the lowest in the Consumer Staples sector

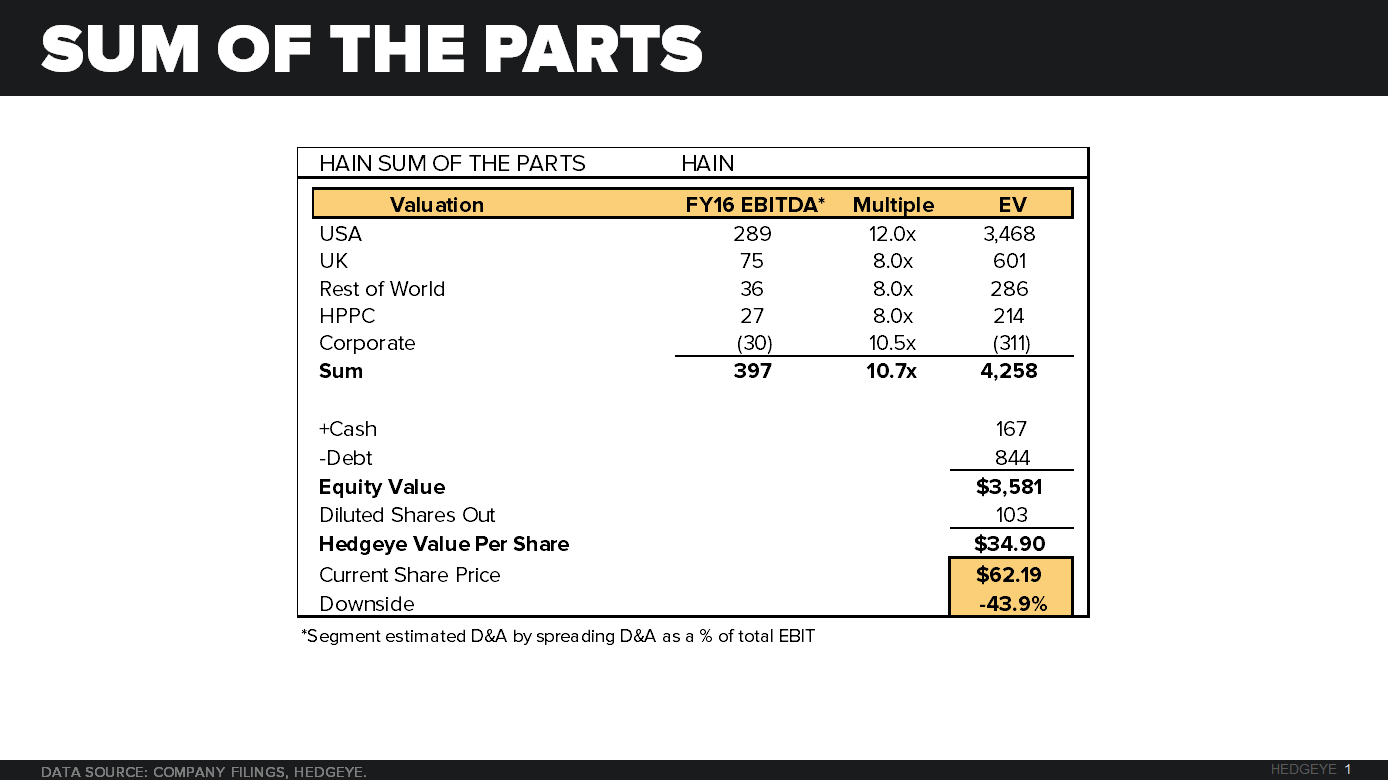

SUM OF THE PARTS

The performance of the UK business last quarter was anything but organic. The company reported a -7.8% decline in revenues and a 210bps decline in operating margins, before currency adjustments. Management alluded to the UK segment net sales being up in “constant currency,” but the retailer environment remains very competitive. Consistent with past quarters management did not comment on real organic growth, but went on to say “we saw good growth from our soup, grocery, desserts, rice and plant-based beverages.” With private label at 40% of sales in the UK segment and seeing declining volumes, the organic growth on the business is limited. Taken together; the 4Q15 performance, limited visibility to organic growth in FY16, and significant exposure to private label should lead the UK business to be valued at a substantially lower multiple than the U.S. business.

As we have demonstrated in our past Black Books, HAIN is less than forthcoming with detailed information on how the core business is preforming and clearly overstates the positive business trends. This past quarter is just another example of the company hiding what the true organic growth is of the UK business.

CUTTING INTO THE MUSCLE

One of our biggest issues with the company is the secular decline in gross margins. As the environment for “better-for-you” products in the U.S. gets more competitive, HAIN will not be able to defend brands or market position. The only weapon the company has to defend itself on declining gross margins is to take massive cuts in G&A. Cutting G&A is never a long term winning proposition, and cutting too deep can put the business model at risk. This quarter looks as if they are cutting into the muscle of the company. With the current G&A cuts the company is now taking a big risk with their most important distribution channel.

In 4Q15, HAIN announced that they were moving their natural channel merchandising team to Advantage Sales & Marketing to “drive SG&A productivity.” Advantage is a third party national sales and marketing company that works with many companies within the consumer packaged goods space.

This is just the latest move by HAIN to reduce costs, saving them roughly 20-25% per year. Advantage is used by some of the big players to supplement their sales and marketing in the natural & organic channel, specifically on slower moving sku’s. The problem with HAIN’s use of this company is its sole dependence on it, as they said they moved their entire natural channel merchandising team to Advantage.

Transferring the entire operation out of HIAN is strategically a very risky idea and could lead to a loss of brand expertise at the company. HAIN will effectively go from managing their brands first hand to having a third party manage them, depending on how their contract is structured (dedicated resources or not) will be a pivotal factor. The biggest advantage of an internal sales force is, share of mind, you want your employees pitching your products. How do you know the third party will be representing your brands in the best light?

Advantage is a middle market provider from a cost perspective, definitely cheaper than others, such as Crossmark.

LINE ITEM ADJUSTMENTS LOWER THE QUALITY OF EARNINGS

The company’s ability to make the numbers is growing increasingly challenged and management is being forced to adjust more lines to meet expectations.