Key Takeaway:

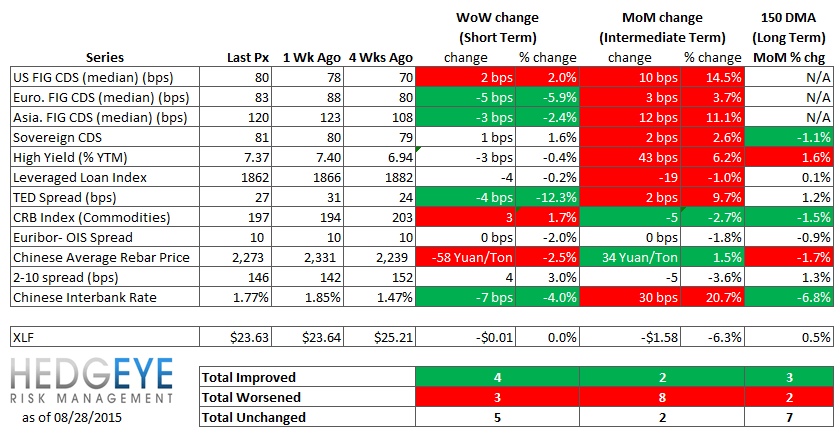

The VIX has "cooled off" to ~26 following an intraday surge above 50 last week - the highest reading since early 2009. Global markets bounced on Wednesday following comments from Federal Reserve President William Dudley that a September rate hike now seems less compelling and a favorable revision to US GDP (+3.7% vs +2.3%) restored a degree of confidence. Risk warnings in our heatmap below eased off for the week with slightly more green than red in the short term. However, looking at the intermediate term, risk perception remains one-sided in favor of the negative; eight out of twelve measures are red. From our standpoint, nothing has changed fundamentally. The key risk metrics we watch in China remain on the same negative trend.

Current Ideas:

Financial Risk Monitor Summary

• Short-term(WoW): Positive / 4 of 12 improved / 3 out of 12 worsened / 5 of 12 unchanged

• Intermediate-term(WoW): Negative / 2 of 12 improved / 8 out of 12 worsened / 2 of 12 unchanged

• Long-term(WoW): Positive / 3 of 12 improved / 2 out of 12 worsened / 7 of 12 unchanged

1. U.S. Financial CDS – Swaps tightened for 14 out of 27 domestic financial institutions on positive GDP data and dovish comments from Fed President William Dudley. U.S. GDP came in at 3.7% in the second quarter, and Mr. Dudley commented that the case for a September rate increase is now less compelling.

Tightened the most WoW: ALL, CB, ACE

Widened the most WoW: BAC, C, MS

Tightened the most WoW: CB, ACE, AXP

Widened the most MoM: GNW, MET, GS

2. European Financial CDS – Swaps mostly tightened in Europe last week as a global market recovery began on Wednesday.

3. Asian Financial CDS – Swaps were a mixed bag across Asian Financials last week. Chinese banks were mostly tighter, while Japanese banks widened.

4. Sovereign CDS – Sovereign Swaps were little changed over last week. Spanish swaps widened the most, by +3 bps to 101.

5. Emerging Market Sovereign CDS – Emerging market swaps mostly tightened last week. Russian swaps saw the largest move, tightening by -45 bps to 375.

6. High Yield (YTM) Monitor – High Yield rates fell 3 bps last week, ending the week at 7.37% versus 7.40% the prior week.

7. Leveraged Loan Index Monitor – The Leveraged Loan Index fell 4.0 points last week, ending at 1862.

8. TED Spread Monitor – The TED spread fell 4 basis points last week, ending the week at 27 bps this week versus last week’s print of 31 bps.

9. CRB Commodity Price Index – The CRB index rose 1.7%, ending the week at 197 versus 194 the prior week. As compared with the prior month, commodity prices have decreased -2.7%. We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

10. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread was unchanged at 10 bps.

11. Chinese Interbank Rate (Shifon Index) – The Shifon Index fell 7 basis points last week, ending the week at 1.77% versus last week’s print of 1.85%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

12. Chinese Steel – Steel prices in China fell 2.5% last week, or 58 yuan/ton, to 2273 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread widened to 146 bps, 4 bps wider than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

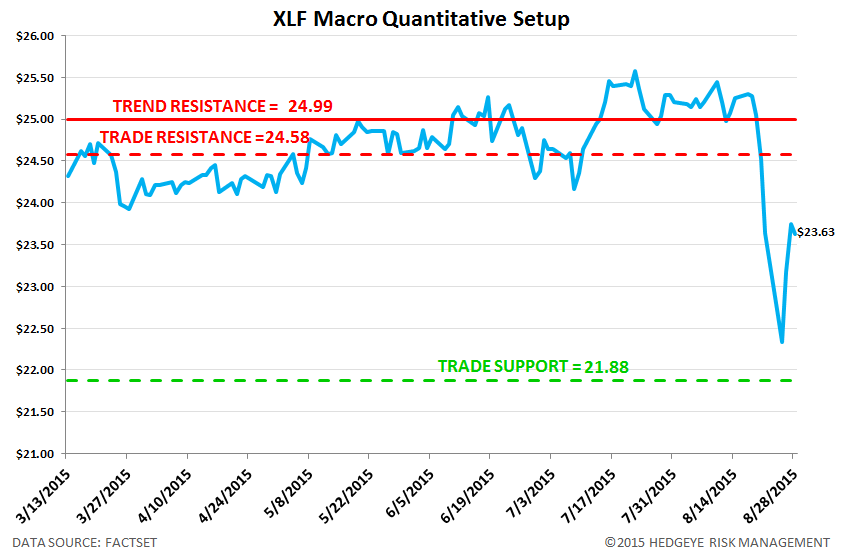

14. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 4.0% upside to TRADE resistance and 7.4% downside to TRADE support.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT