Japanese shares have remained one of the best performing DM global equity markets as of late. That being said, we don't believe it makes a ton of sense to bet that this outperformance continues from here (at least not in the immediate-term). A confluence of domestic and international factors suggest it is now appropriate for investors to book gains – be they absolute or relative – on the long side of Japanese equities (DXJ).

I) No Easy Money Anytime Soon: Despite that fact that Headline CPI, Core CPI and PPI all continue to slow on a sequential and trending basis, recent commentary out of the BoJ – led by Governor Haruhiko Kuroda – continues to be [inappropriately] sanguine on the outlook for reported inflation in Japan. In addition to that, Prime Minister Shinzo Abe was out over the weekend effectively granting the BoJ leeway in its pursuit of the +2% inflation target amid the recent plunge in crude oil prices while also confessing his complete faith in the BoJ’s handling of monetary policy. The key takeaway here is that the Cabinet Office is unlikely to lean on the BoJ to ease in the near term, which, on the margin, reduces the likelihood of QQE expansion in 2H15. Specifically, increased wiggle room in obtaining key policy objectives delays the advent of presumably desired policy support measures from the perspective of Japanese equity market participants.

II) China Headwinds: Clearly the recent devaluation of the Chinese yuan put dour outlook for regional and global growth at the center of investors’ concerns. Last Friday, Chinese growth – in Manufacturing PMI terms – hit a 77-month low with the advent of the flash Caixin-Markit report for the month August. As such, we can reasonably conclude that investors are commensurately worried about the outlook for corporate earnings growth in Japan given the headwinds to exports stemming from Chinese #GrowthSlowing (Japan’s 2nd largest export market at 18.1%), as well as the recent bout of defensive strength in the yen amid global contagion.

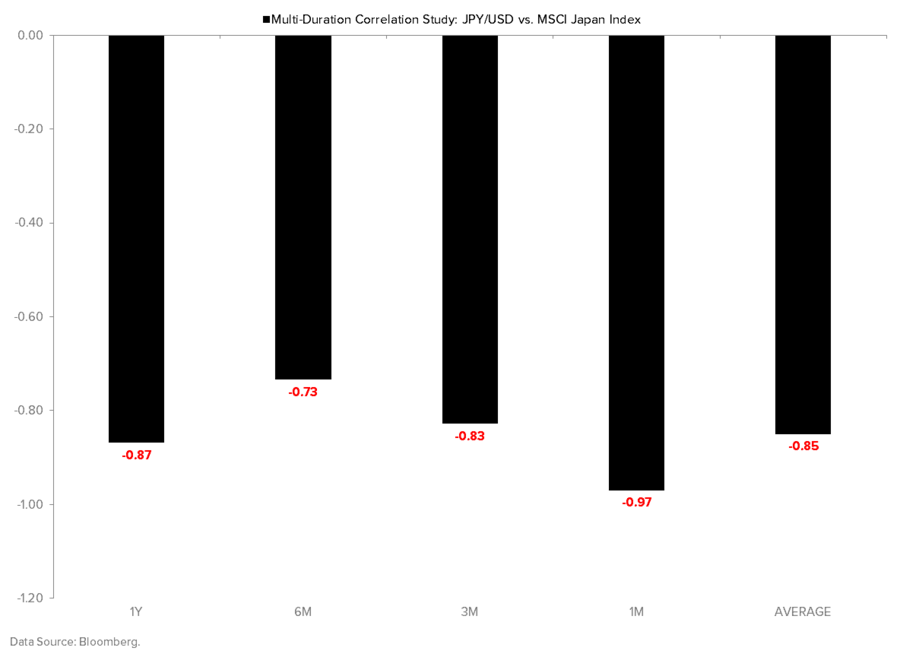

III) Correlation Risk: Speaking of global contagion, the recent melt-up in the Japanese yen (up +3.1% since Thursday’s close) and melt-down in the Nikkei 225 (down -11.1% since Thursday’s close) should remind investors that the Japanese equities remain tightly correlated to monetary policy expectations – despite growing calls for a sustainable decoupling. Specifically, cyclical bouts of global risk aversion have historically proved positive for the Japanese yen. This is largely due to the yen’s status as both a global funding currency and Japan’s status as an international capital allocator. Its net international investment surplus of ~$3.1T is equivalent to 75% of the country’s GDP and compares to a -$6.8T deficit for the U.S.

All told, while we still continue to see long-term upside for Japanese equities amid sustainable higher-highs in the USD/JPY exchange rate as the LDP and BoJ’s +3% GDP and +2% Core CPI targets clash with heinous demographic dynamics that should lead to perpetually easier monetary policy at the margins. Given the immediate-to-intermediate-term headwinds outlined above, however, we consider it prudent for investors to step to the sidelines for now.