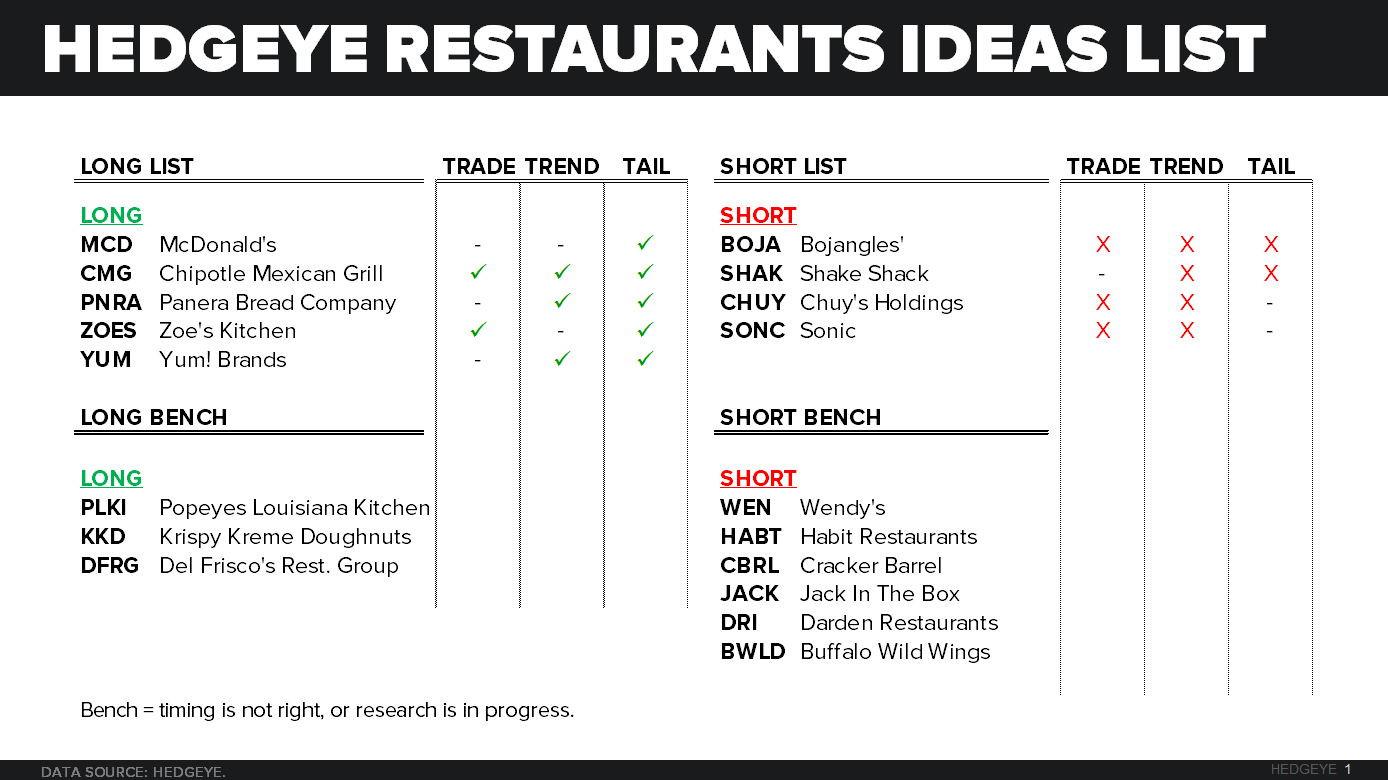

RECENT NOTES

8/17/15 MCD | Create Your Taste Experience

8/11/15 SHAK | PLANTING FLAGS

8/10/15 July Restaurant Sales and Employment Trends

8/7/15 BOJA | BO’S DILEMMA

RECENT NEWS FLOW

Friday, August 21

MCD | Signed agreement to franchise 20 restaurants in remote Russian locations (click here for article)

Burgers | Casual dining restaurants boosting lunch sales with burgers (click here for article)

Thursday, August 20

MCD | Another survey supports the expansion of All Day Breakfast (click here for article)

Wednesday, August 19

QSR | Burger King is expanding delivery service in India, marking the fifth country that BK offers the service (click here for article)

Tuesday, August 18

YUM | Micky Pant named new Yum China CEO (click here for article)

NYC Restaurant Wage Hikes | Quick service restaurant owners in New York have filed objections to the proposal to raise minimum wage to $15 per hour (click here for article)

Monday, August 17

DFRG | Opened new Double Eagle steak house in Orlando, FL (click here for article)

SBUX | Expanded evening program with beer and wine (click here for article)

DRI | Named Bill Lenehan as CEO of proposed REIT, currently a member of the Darden board (click here for article)

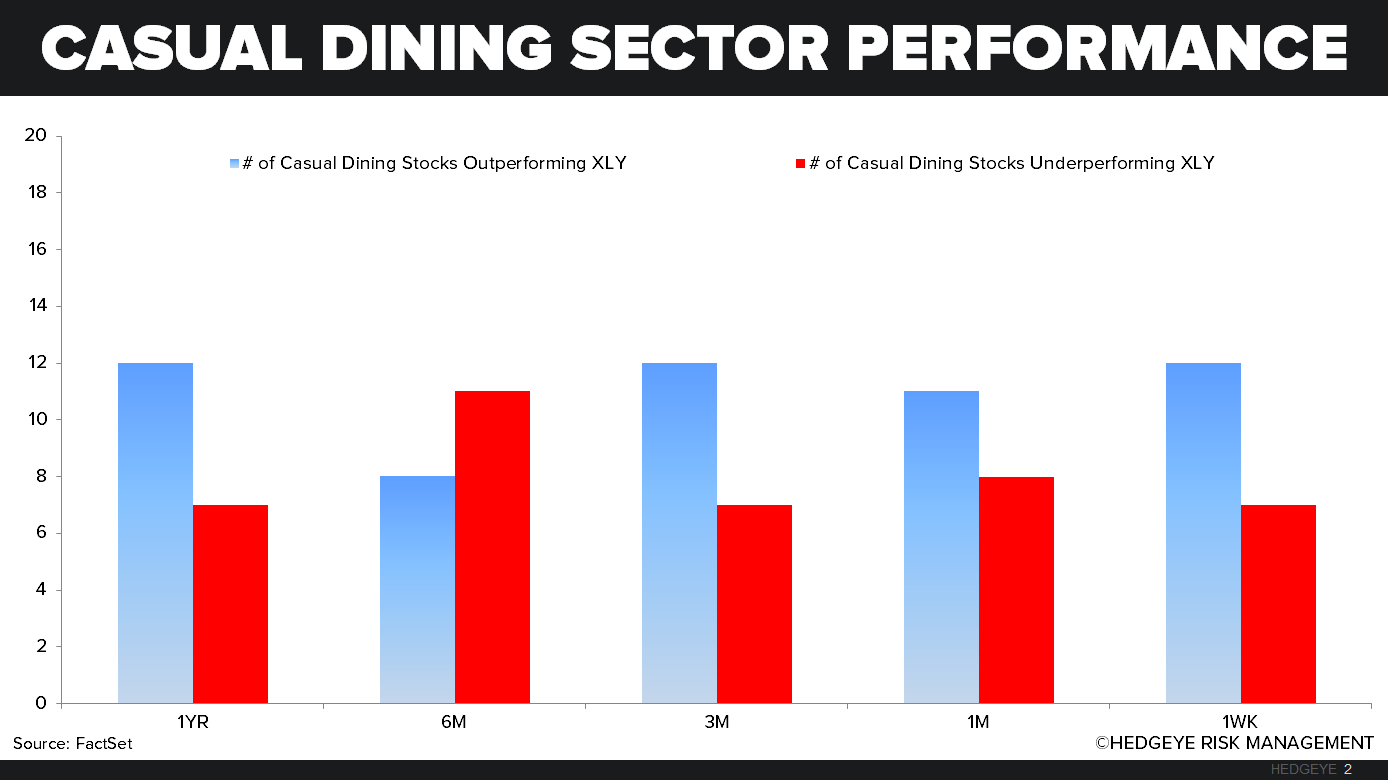

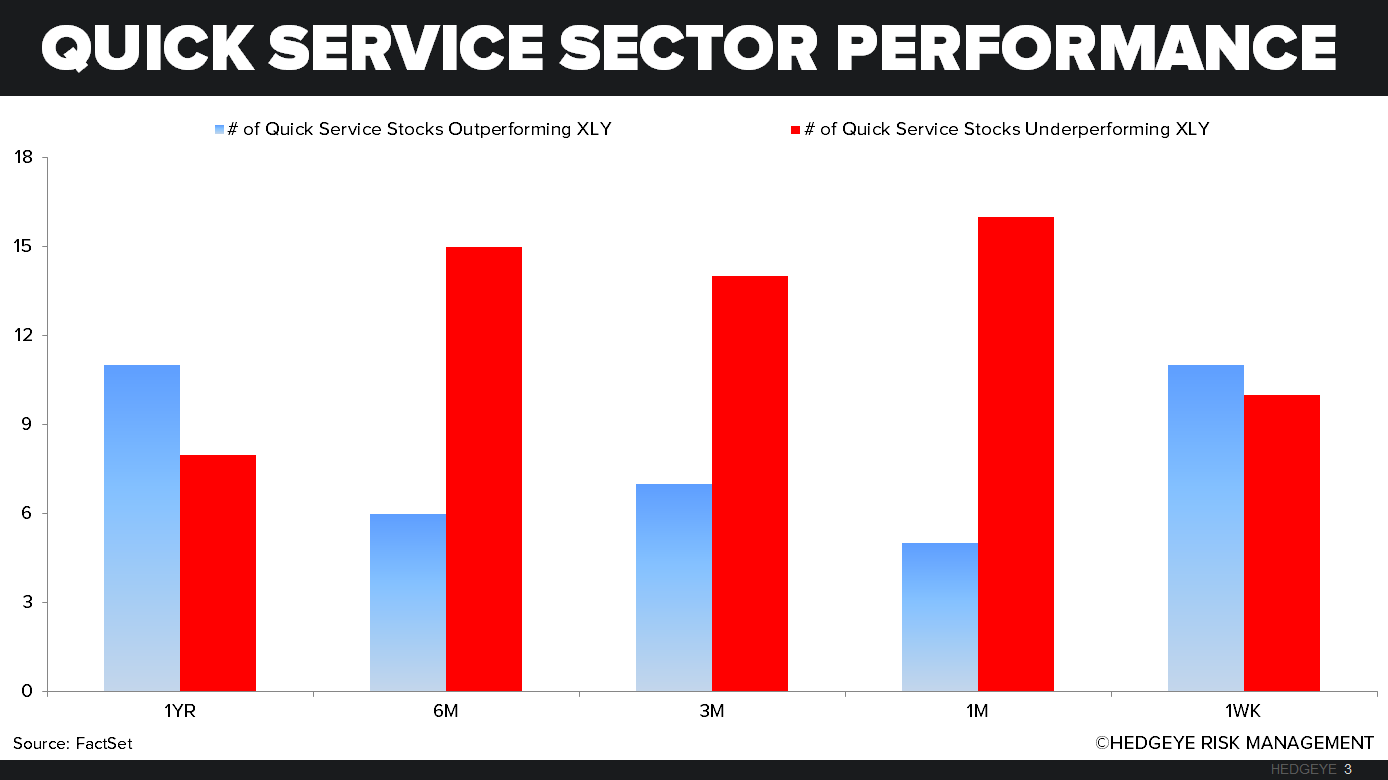

SECTOR PERFORMANCE

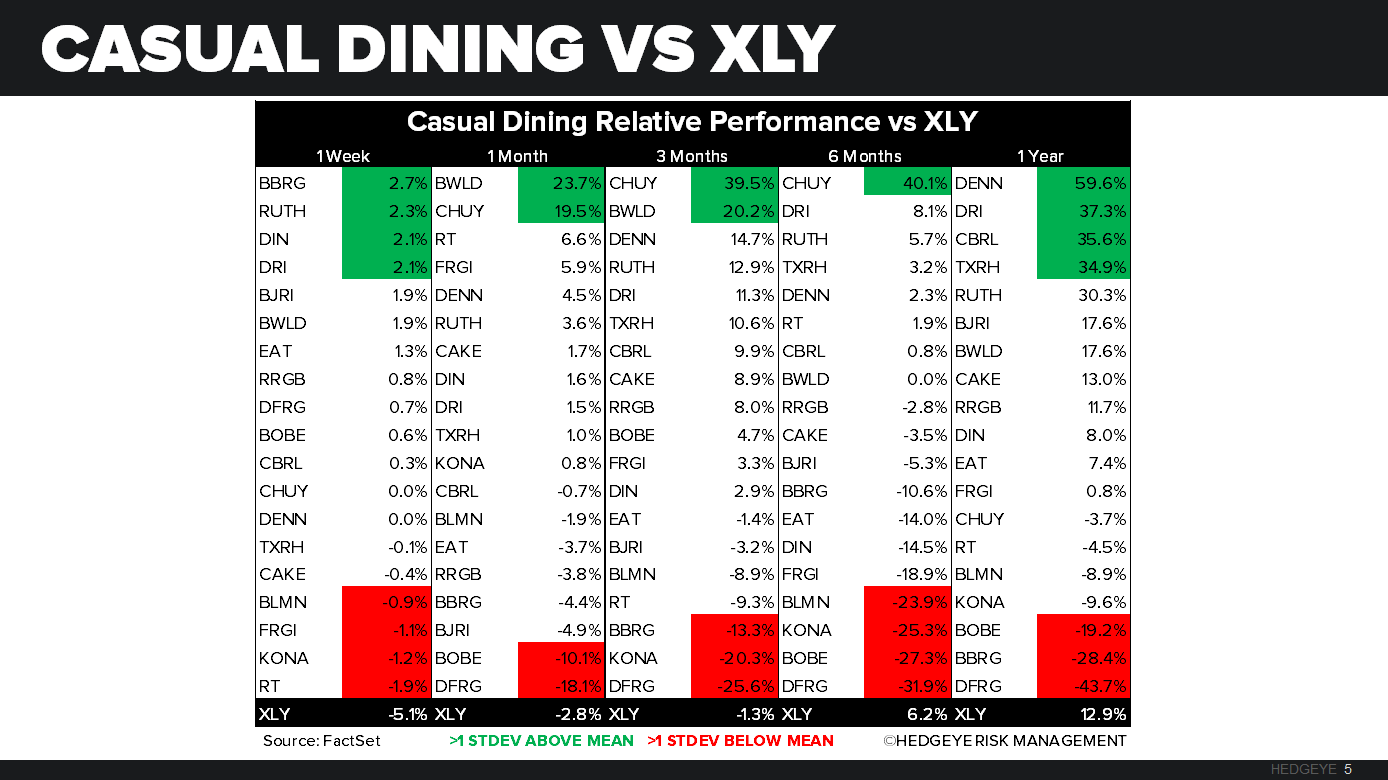

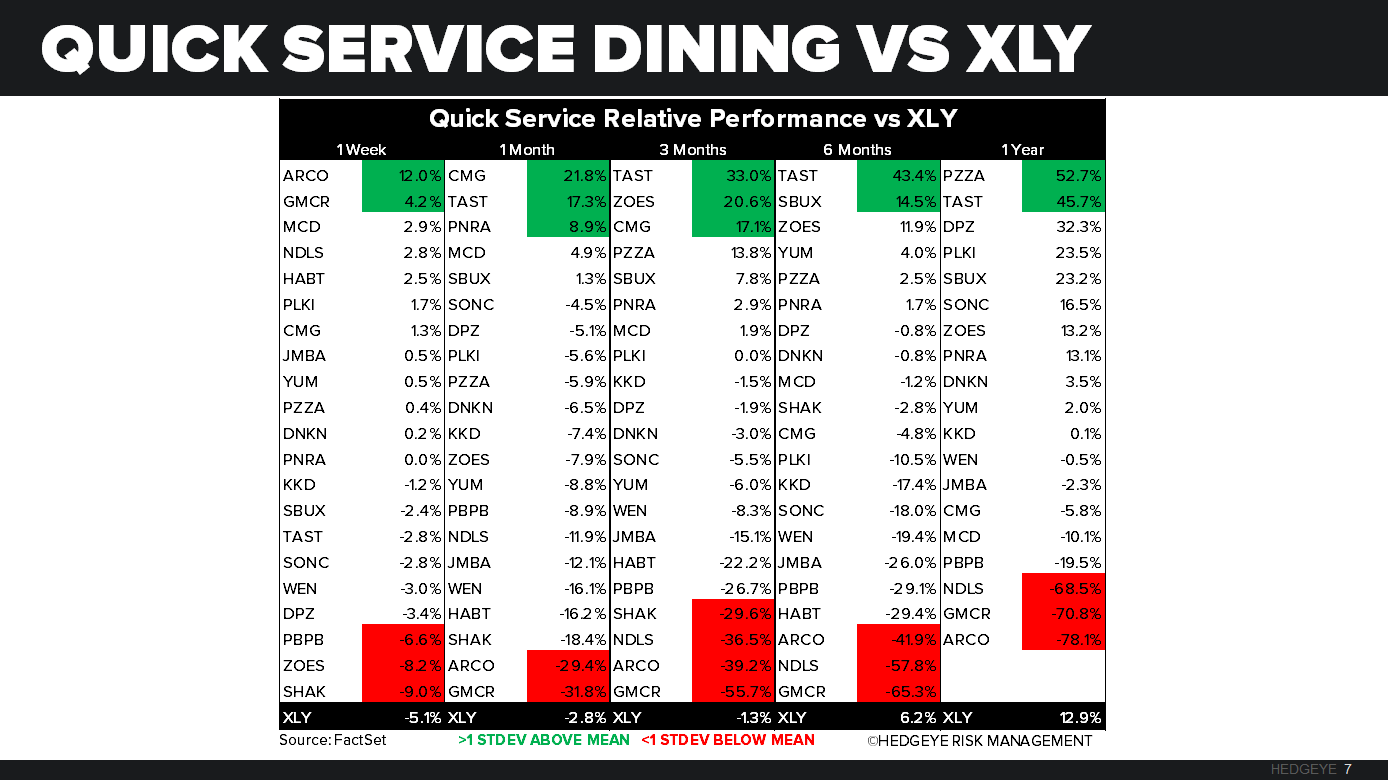

Casual dining and quick service stocks, in aggregate, outperformed the XLY last week. The XLY was down -5.1%, top performers from casual dining were BBRG and RUTH posting an increase of 2.7% and 2.3%, respectively, while ARCO and GMCR led the quick service pack up 12.0% and 4.2%, respectively.

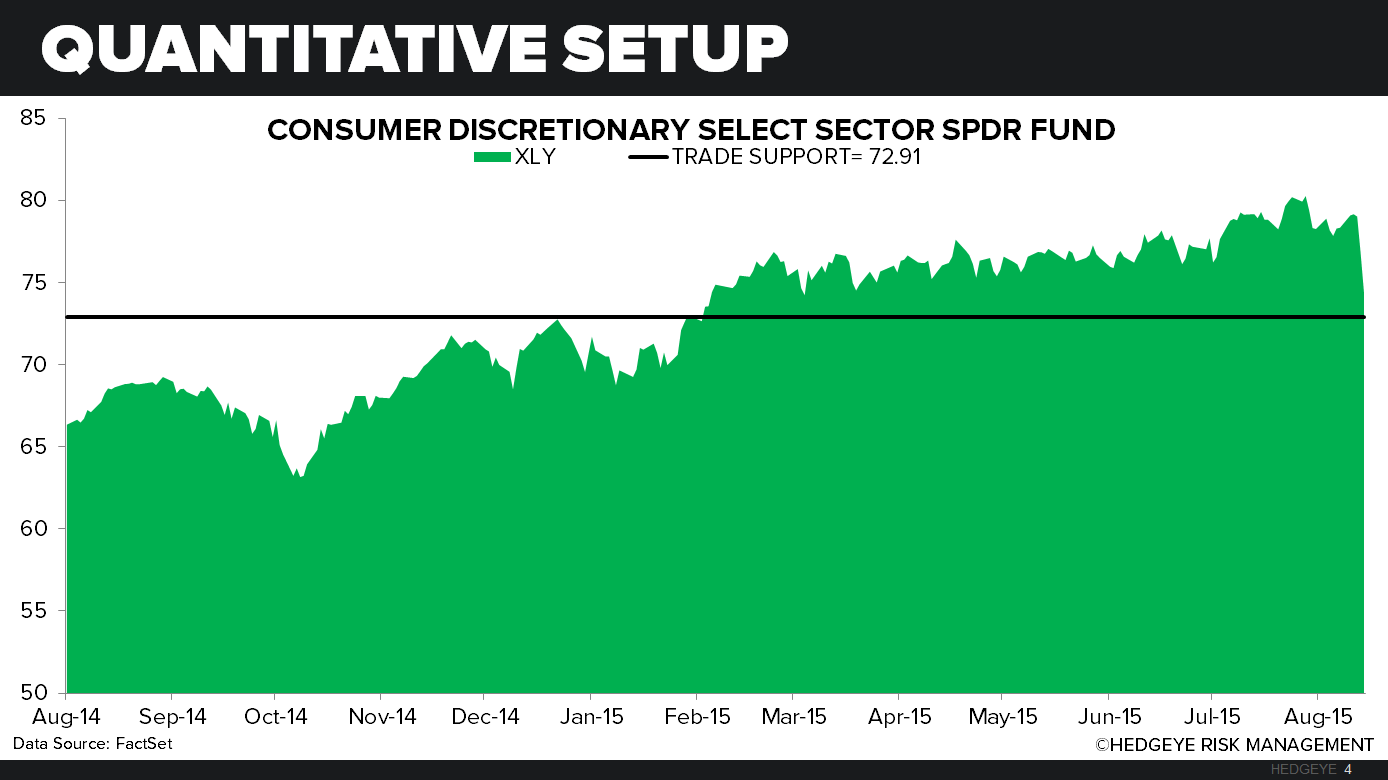

QUANTITATIVE SETUP

From a quantitative perspective, the XLY looks bearish from a TRADE and TREND perspective, TRADE support is 72.91.

CASUAL DINING RESTAURANTS

QUICK SERVICE RESTAURANTS

Keith’s Three Morning Bullets

- CRASH – not an inappropriate word to use given that on the 3-month duration alone, Oil (-37%), China (-31%) Emerging Markets (-26%), and Long-term Sov Bond Yields have crashed. This is a literal crashing of both US and Global growth expectations – we’re still at ½ of consensus forecasts

- HIKE? – oh definitely – they should hike. “It’s just 25 basis points, Keith” – yep. Have at it. Let’s see what happens. This risk of being too tight during both the cyclical and secular slowdown was only obvious to those who had the bearish growth and inflation views. Jackson Hole = Thursday

- VIX – the main challenge with modeling accurate risk management levels right now is that volatility is undergoing a major Phase Transition across durations – hard to explain in 140 characters or less but very easy to see the series of higher-highs going back 2yrs