Weekly Activity Wrap Up

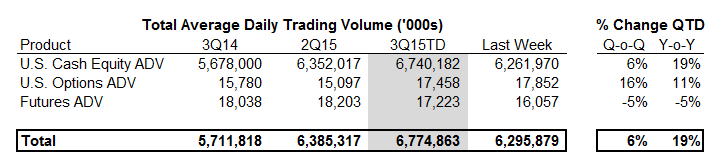

U.S. cash equity volume growth for the third quarter remains strong but decelerated slightly last week to +19% year-over-year from +20% in the prior week. Equities are maintaining their lead among the major product categories with U.S. equity options activity putting +11% Y/Y growth currently. U.S. futures trading has been in a summer lull for the third quarter with this week's average volume coming in at 16.1 million, lower than the third-quarter average of 17.2 million. That represents a -5% year-over-year contraction. The important open interest tally continues to favor our Best Idea's long view on CME Group (CME), with the big Chicago exchange's trading backlog now up +25% since the beginning of 2014. (It was up +24% last week.)

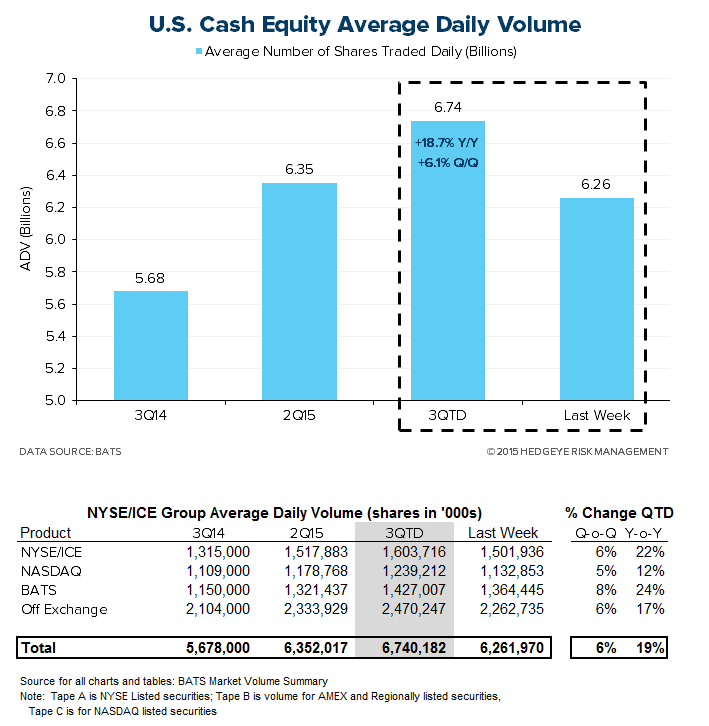

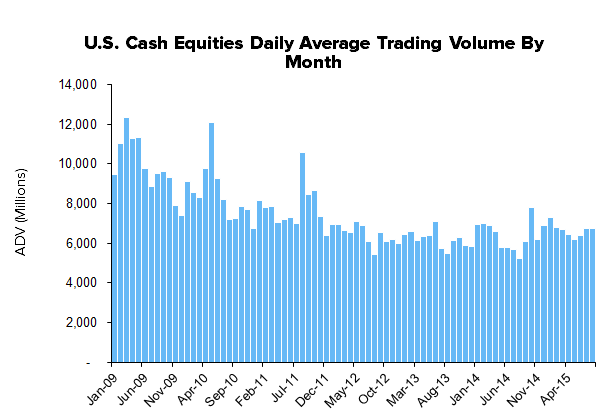

U.S. Cash Equity Detail

U.S. cash equity trading finished the week at 6.3 billion shares traded which is blending to a 6.7 billion daily average thus far for the 3rd quarter of 2015. This is +19% year-over-year growth for U.S. stock activity. The market share battle for volume is mixed, with the New York Stock Exchange/ICE standing pat at 24% market share but with NASDAQ's still sporting market share 200 bps lower than last year, a -6% decline.

U.S. Options Detail

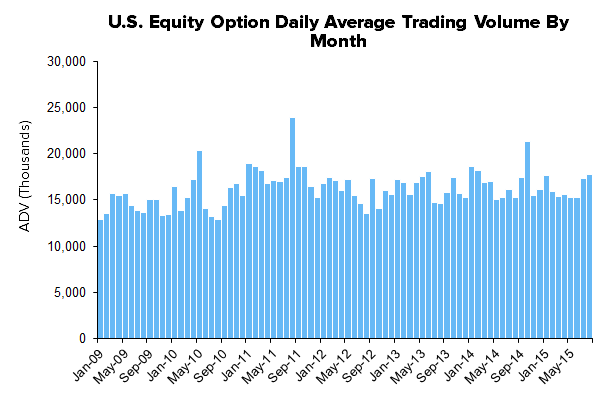

U.S. options activity remains significantly higher, both quarter-over-quarter and year-over-year. 17.9 million contracts traded this week which is blending 3Q15 activity to 17.5 million contracts per day, up +16% quarter-over-quarter and +11% year-over-year. The market share battle amongst venues continues to be one of losses at both the NYSE/ICE and NASDAQ. NYSE has lost 400 basis points of share year-over-year settling at just 18% of options trading currently. NASDAQ has shed 300 basis points of share, good for a -14% loss from last year as ISE/Deutsche Boerse and BATS mop up volume and share.

U.S. Futures Detail

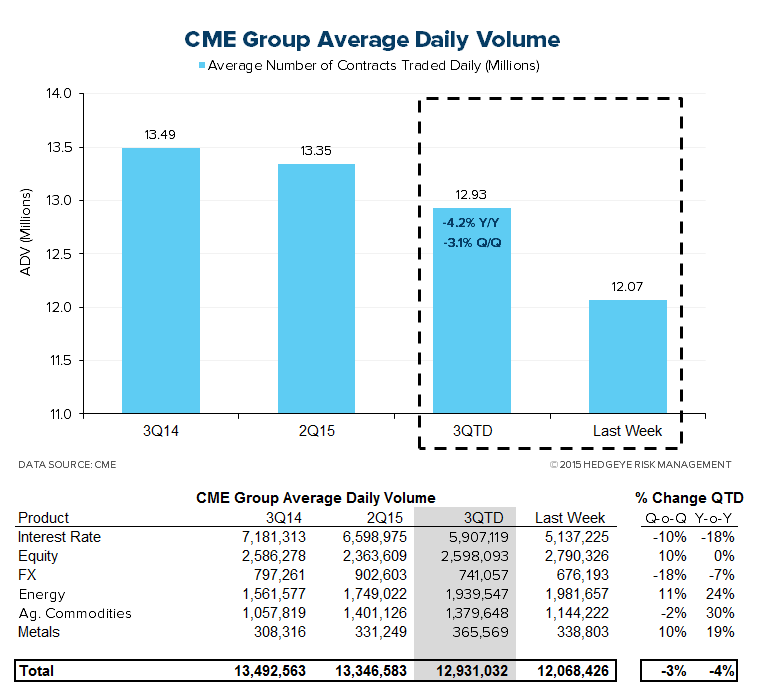

CME Group volume came in this week at 12.1 million contracts. That blends 3Q15 volume to a 12.9 million average level, a -4% year-over-year decline. CME open interest, the most important beacon of forward activity, continues in strong fashion with 105.1 million contracts pending, good for +25% growth over the 84.1 million pending at the beginning of 2014. That marks further improvement from the prior week's +24%.

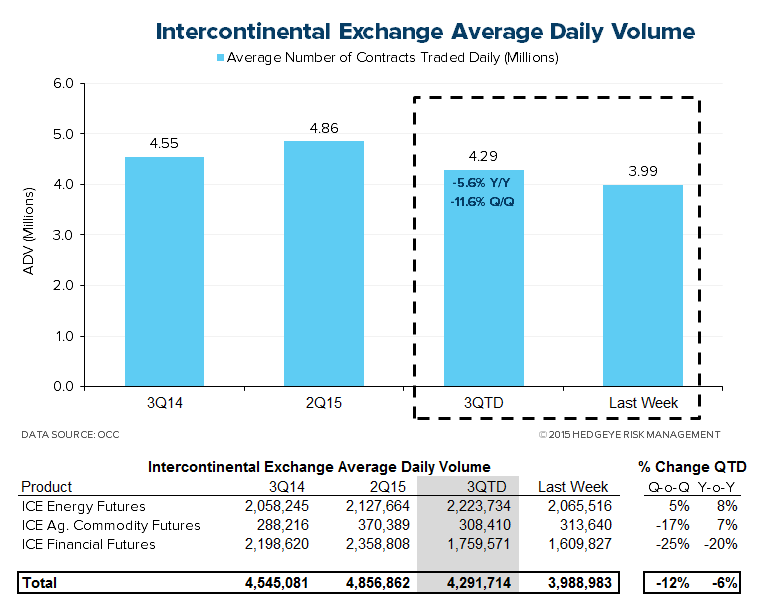

Activity levels on the futures side at ICE hit 4.0 million contracts this week, with 3Q15 blending to a 4.3 million daily average. That is a -6% year-over-year decline. ICE open interest this week tallied 73.9 million contracts, a -2% contraction versus the 75.2 million contracts open at the beginning of 2014. That marks an improvement versus the prior week's -3% level.

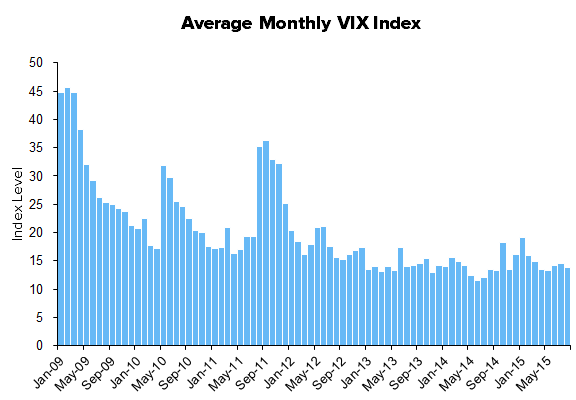

Monthly Historical View

Monthly activity levels give a broader perspective of exchange based trends. As volatility levels, measured by the VIX, MOVE, and FX Vol should rise to normal levels after the drastic compression this cycle, we expect all marketplaces to experience higher activity levels.

Sector Revenue Exposure

The exchange sector has broadly diversified its revenue exposure over 10 years as public entities with varying top line sensitivity to the enclosed trading volume data. The table below highlights how trading volumes will flow through the various operating models at NASDAQ, CME Group, ICE, and Virtu:

We recently presented our investment thesis on the Exchanges. To summarize,

- Long CME: Financially oriented CME Group (CME) is enjoying a long awaited boom in activity, as trader counts and open interest in Treasuries, Eurodollars, and FX products are swelling. The decade long concentration on trading energy and commodities is over and with steeply shaped forward curves and more profitable opportunities, financial products are seeing rapid adoption.

- Short ICE: We see collateral damage from the ongoing rapid price decline in energy and commodity markets. As a result, these important products at ICE will be less active than the Street expects, as commercial hedging and speculative energy trading dries up.

We think CME has $5 per share in earnings power in the out year and the stock will revisit near $140. As outlined in our presentation deck and replay below, a CME long position can also be paired with a short ICE position, with favorable fundamental exposures on each side of the trade.

Separately, recent IPO Virtu (VIRT) is being valued incorrectly by the market. Our main qualm is that the company takes intraday prop risk, but has no tangible equity capital to cover any potential trading losses. Shares of VIRT are currently on our Best Ideas list as a short with a fair value in the mid-teens (30-40% downside).

Hedgeye Exchange Black Book Replay HERE

Hedgeye Exchanges Black Book Materials HERE

Please let us know of any questions,

Jonathan Casteleyn, CFA, CMT

Joshua Steiner, CFA