Kellogg Company (K) is on our Hedgeye Consumer Staples SHORT bench.

We are tempted to press the short, but few names in the space make good shorts in this market. On the LONG side, your best bet for a large cap, low-single digit top-line growth, dividend company within the consumer staples space continues to be General Mills (GIS), which has much broader growth potential.

We have been vocal about our LONG thesis on the cereal market and its return to positive growth. We do not picture the category as a major growth driver for a particular company, more as a complement, providing consistent low-single digit sales growth. That is what we have with Kellogg, who just reported 2Q15 results yesterday. The street was overly bearish on the company going into the quarter resulting in an estimate beat, but still considerable declines in operating profit year-over-year.

HEDGEYE OPINION

Management isn’t setting the bar too high, even with the sluggish 1H of the year it won’t be difficult to achieve flat sales for the full year. If we continue to see the same softness in volumes and sales, these longer-term targets will start to seem unachievable. We continue to be bearish on K, but can’t find the conviction to call it a true SHORT yet. We do however continue to get excited about the cereal categories resurgence after every earnings call we listen to from one of the category leaders; POST is up next, on Friday, August 7th.

PERFORMANCE IN THE QUARTER

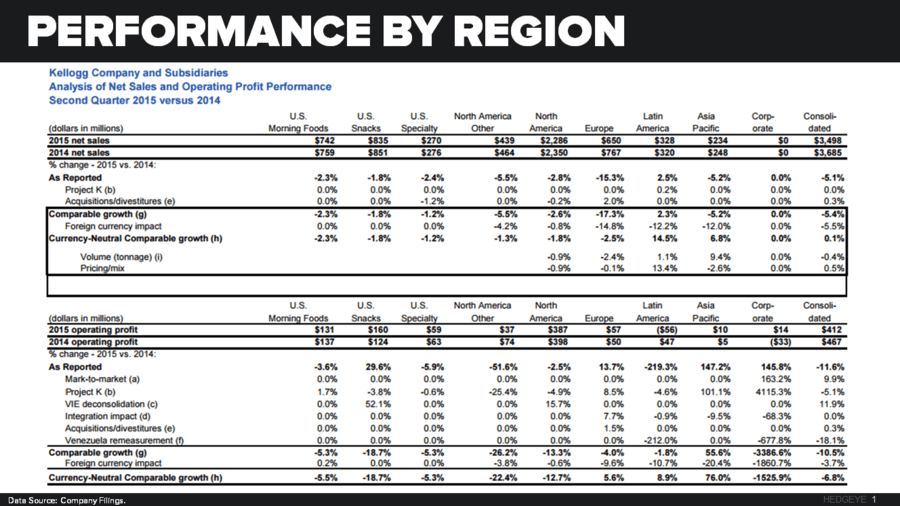

K’s reported 2Q15 currency-neutral comparable diluted EPS of $0.97 versus consensus estimates of $0.92, representing a -4.9% decrease YoY. Currency-neutral comparable net sales came in above estimates, reporting $3,685mm versus consensus estimates of $3,466mm, representing a +0.1% increase YoY. Although net sales saw a slight uptick, notably volume for the company was down -0.4%. Currency-neutral comparable operating income of $529mm beat consensus estimates of $507mm, representing a -6.8% decrease YoY.

PERFORMANCE BY REGION

NORTH AMERICA

(Represents ~65% of total consolidated net sales)

The region struggled across the board, led by U.S. Morning Foods and U.S. Snacks, reporting net sales declines of -2.3% and -1.8%, respectively. The total segment net sales declined -1.8%, leading to a -12.7% decline in operating profit. Operating profit declines were led by North America Other (includes the U.S. Frozen Foods, Kashi and Canadian businesses) down -22.4%, followed by U.S. Snacks, down -18.7%, U.S. Morning Foods down -5.5% and lastly U.S. Specialty down -5.3%. North America is clearly still struggling to grow sales, other things affecting the quarter were increased distribution costs, timing of production and incentive compensation. Although all segments in North America showed net sales declines, management stated that “sales increased…in the Frozen Foods and Canadian businesses.” Management was upbeat about the progress made in cereal, but there is still more to do, as they put it. Currently management is confident in the improvements they have made to the product offering, and continue to improve. Cereal consumption seems to have stabilized and was flat in Q2, Kellogg branded sales were essentially flat, with the top six brands growing share and sales. Currently 75% of cereals are made without artificial colors and more than half without artificial flavors, they plan to transition to 100% on both by 2018. U.S. is down -1.8% as a result of continued weakness in wholesome snacks, and continued distribution losses on this businesses. U.S. specialty sales were down -1.2% in the quarter, as business is experiencing share losses in foodservice. Kashi has continued its descent in 2Q15, and they continue to invest in the brand, is it a dead better-for-you brand? Possibly, it will have to turn soon, or all the investment made in the brand will be for nothing.

EUROPE

(Represents ~19% of total consolidated net sales)

The Europe team is working through a rather difficult operating environment, but surviving. Net sales for the region were -2.5% in the quarter, while operating profits increased 5.6%. These positive results were driven by improved COGS and the timing of investments made in brand building. Pringles is a winner in all regions, growing net sales at a double-digit rate in the UK and Germany. Cereal is struggling international, a little more than the U.S.

LATIN AMERICA

(Represents ~9% of total consolidated net sales)

Latin America has experienced robust sales growth, with net sales up 14.5% and operating profit up 8.9%, driven in large part by the Pringles brand, as well as investments in renovating other brands. This region provided another glimmer of hope for the cereal business, seeing moderate volume and price growth. Consumption of Pringles was also strong for the quarter, leveraging Copa America partnership to drive sales. Latin America, more than any other region was assisted by pricing/mix, which represented 13.4% of the 14.5% increase in net sales.

ASIA PACIFIC

(Represents ~7% of total consolidated net sales)

Asia Pacific is crossing over some easy comparisons, but they are experiencing strong growth as well. Net sales are up 6.8% in the region with operating profit up 76%, still only representing $10mm in operating profit as shown in the chart above.

MANAGEMENT GUIDANCE

Management reaffirmed guidance for the full year 2015, which consists of the following:

- Net Sales = Approximately flat

- Operating Profit = -2% to -4%

- EPS = Flat to -2%

- Operating Cash Flow = Approximately $1bn

- Total capital spending = 4% to 5% of sales

- Share repurchases in 2015 = $700mm to $750mm

Additionally, management provided early guidance for the 2016 fiscal year, which was unusually early; they usually wait until at least Q3. Seemed that they were trying to shift focus away from current poor performance and urge investors to look out 2-3 quarters. In 2016 management hopes that current initiatives both cost savings and investments will start to make a stronger impact leading to flat to slightly up sales, getting them back on their long-term growth model.