C&I Seeing a Bump to More Easing and Mortgages Continue Significant Easing

The Fed released its 3Q15 Senior Loan Officer Survey yesterday afternoon. The survey was conducted between June 30 and July 14 and covers lending standards and loan demand across business and consumer loan categories.

The survey results were largely positive. In most categories, lenders continue to report net easing of underwriting standards, falling spreads and rising borrower demand.

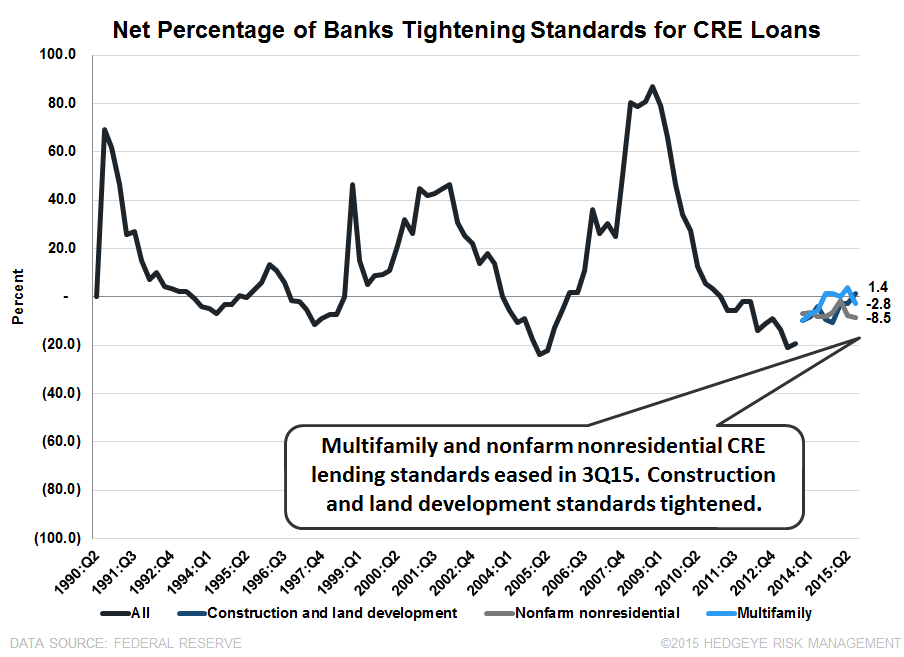

The one slight negative for the quarter was that standards for construction and land development CRE loans crossed the zero line into net tightening in 3Q15, but only by 1.4%.

Here are the two main takeaways this quarter:

1. The net % of banks easing C&I lending standards rose in 3Q15. 7% of banks eased C&I credit standards for large firms in 3Q15 versus 5% in 2Q15. Additionally, 6% of banks eased C&I credit standards for small firms versus 1% in 2Q15.

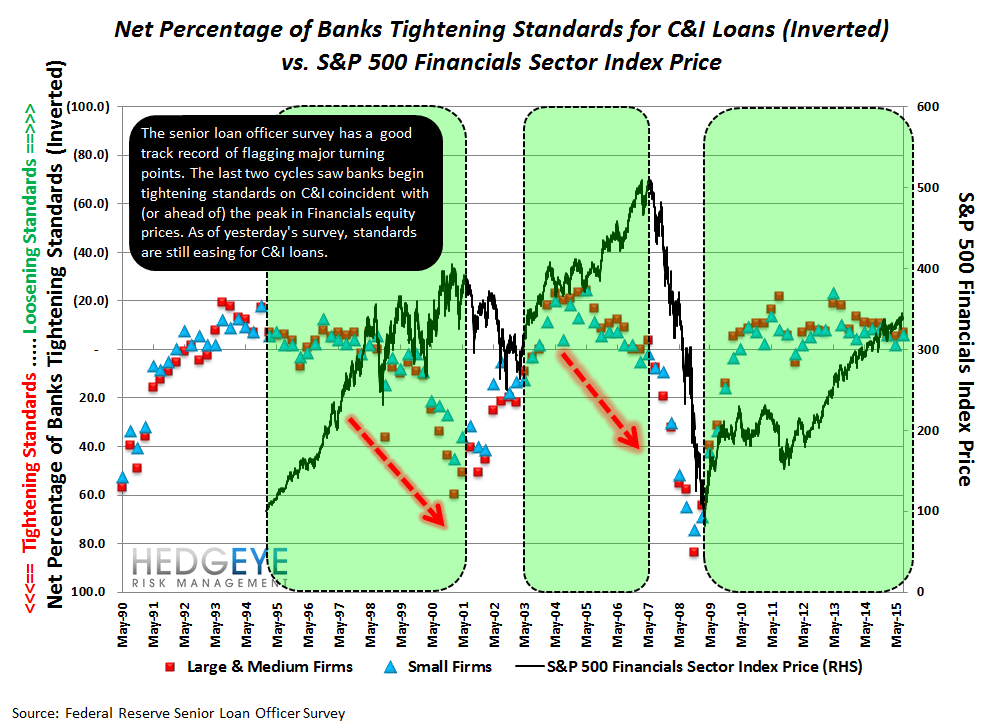

The chart below looks at the historical C&I lending standards (LHS) juxtaposed against the S&P 500 Financials Index (RHS). C&I lending standards have historically begun tightening ahead of peaks in equity prices. We've highlighted in green the periods during which Financials stocks are rising. In the 1990s it was clear that lending standards were tightening by early-1999, suggesting the roll was near. In the 2003-2007 period standards began to tighten steadily in 2007.

There are two important takeaways here. First, inflections in this series lead turning points in Financials equity prices. Second, underwriting standards tend to be autocorrelated, meaning they trend in the same direction for a long time before reversing. This means that once the turn begins you can ride the trend for a long time.

2. Ongoing Resi Easing. Lending standards among underwriters of Fannie and Freddie guaranteed loans continued to ease in 3Q. FHA/VA standards also eased in the quarter. One of the central tenets to our longer-term bull case on Housing is that underwriting standards will continue to ease in the coming years as the credit pendulum works its way back to center.

Now, A Quick Review of the Senior Loan Officer Survey by Category:

C&I: Easing Resumed

Last quarter we called out C&I as a potential canary in the coal mine. That's because the net percentage of lenders tightening standards was almost back to the zero line. This matters because, historically, net tightening of credit conditions has preceded (and arguably, precipitated) all three recessions since the survey's introduction.

As such, we were very interested in whether the 3Q15 survey would show a continuation of that trend. It turns out that it didn't. C&I lending standards eased at a faster clip in 3Q than they did in 2Q.

Moreover, demand from both large and small firms for C&I loans increased in the third quarter.

CRE: C&D Tightens (Slightly)

Back in 4Q13, the Fed split the CRE category into four new survey components: C&D Lending, Nonfarm nonresidential lending, and Multifamily lending. C&D lending actually saw a small net percentage of lenders tightening standards -- a first in the post-4Q13 era. We wouldn't get too excited about it as it was only 1.4%, net of lenders surveyed that were tightening, but the trend signal is what matters to us.

Meanwhile, the lending environment for nonfarm nonresidential and multifamily CRE loans improved in the third quarter as banks eased standards.

Demand for all three categories of CRE loans increased in the third quarter.

Residential Mortgage: Easing

Starting in 1Q15, the Federal Reserve broke the survey's residential Prime and Nontraditional categories into six new categories and kept the Subprime category for a total of seven different categories. The six new categories include: (GSE-Eligible, Government, QM non-jumbo/non-GSE eligible, QM jumbo, Non-QM jumbo, and Non-QM/non-jumbo). The categories we're most interested in are the GSE-Eligible (Fannie/Freddie) and Government categories (FHA/VA) since these two categories account for ~90% of all origination volume. The GSE-Eligible category showed 11.3% of banks, net, eased standards Q/Q in 3Q15. Additionally, Government showed a 5.1% net easing. Four of the other five categories also eased.

We pay little attention to the demand component of the Fed's Survey because it reflects shifting refi demand and isn't a good barometer for purchase activity. Nevertheless, we include both charts below.

Consumer: Easing

Standards for credit cards, auto loans, and consumer loans ex-cards and autos all eased in the third quarter.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT